Aether Holdings ($ATHR) is the kind of fraud that wears a suit and rings the Nasdaq bell. Behind the buzzwords and newsletters lies a dumpster fire of fake filings, insider enrichment, and outright deception. The CEO sold shares during the lock-up through an undisclosed shell. A barred broker is running point. Their auditor fails 100% of PCAOB reviews. They operate out of a virtual mailbox with less than $3K in equipment. This isn’t a business — it’s a blueprint for a pump-and-dump. We’ve connected the dots. Now it’s the SEC’s turn.

Aether Holdings (NASDAQ: ATHR) is a ticking time bomb dressed in buzzwords and artificial valuation. Behind the $200M market cap façade lies a cheap virtual office, zero infrastructure, deceptive insider enrichment, and brazen violations of SEC regulations. This isn’t just another poorly managed media play — this is a premeditated scheme orchestrated by serial penny stock promoters hiding behind shell entities and misleading disclosure statements.

We believe ATHR is committing securities fraud through:

IPO lock-up violations

Undisclosed insider dealings via 28 Ventures

Material misrepresentations in SEC filings

Sham acquisitions to inflate perceived growth

Auditor red flags and regulatory obfuscation

Nonexistent operations camouflaged with PR gimmicks

We are calling on the SEC, FINRA, DOJ, and retail/institutional investors to take a hard look at this house of cards. It’s time to bring the hammer down.

RED FLAGS MATRIX

Category | Red Flag |

|---|---|

Lock-Up Violation | CEO Nicolas Lin allegedly offloading shares via 28 Ventures during lock-up period |

Shell Game | 28 Ventures Aether (with Lin & barred broker Frank Cid) sold 428,572 shares immediately after IPO |

Undisclosed Affiliations | SEC filing claims no material relationship, despite 28 Ventures site showing Lin & Cid as GPs |

Auditor Issues | Auditor is ZH CPA LLC — flagged by regulators for oversight failures |

Dumped 10-Q | Quarterly results filed late Friday, May 16, with no press release — classic red flag timing |

Virtual Office Scam | ATHR’s only listed office is a $12K/year virtual address in NYC with 235 sq ft |

No Real Assets | ATHR has only $3,000 in PP&E, yet claims to run AI/ML analysis at scale |

Undisclosed SPAC Ties | CEO Lin is CFO of newly launched SPAC (ORIQ) — not disclosed in ATHR filings |

Conflict of Interest | Lin’s employment agreement demands full exclusivity — clear breach by his SPAC role |

Barred Insider | Frank Cid (ATHR BD head) is permanently barred by FINRA — omitted from filings |

Sham Acquisition | AltcoinInvesting.co acquisition announced amid traffic collapse — site had 169 visits in June |

Related Party Deals | ATHR issued 50,896 shares to Monic Wealth Solutions (linked to execs) for vague consulting work |

LOCK-UP VIOLATION — LIN SELLS THROUGH 28 VENTURES

ATHR’s April 11, 2025 IPO Prospectus included a standard lock-up clause:

“Our directors and officers... entered into customary lock-up agreements... for a period of six (6) months.”

On its face, this would prevent CEO Nicolas Lin from selling shares until October 2025.

But here’s the bait-and-switch:

On the exact same day, ATHR filed a separate resale registration statement allowing 428,572 shares to be sold by 28 Ventures Aether, a Series of 28 Ventures Master LLC. The kicker? 28 Ventures is run by Lin himself, along with Frank Cid, ATHR’s Head of Business Development and a FINRA-barred securities offender.

Let’s be perfectly clear:

Lin sold his own stock through a shell company he co-founded while pretending to be locked up.

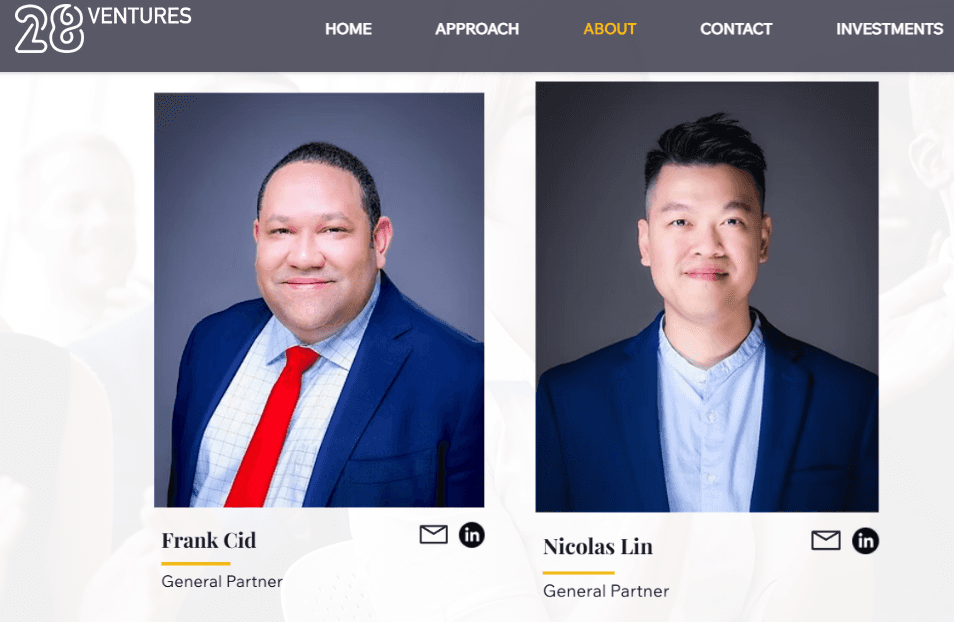

Figure: Screenshot from 28 Ventures Website — Executive Team Page

This figure shows Frank Cid and Nicolas Lin, both listed as General Partners of 28 Ventures, directly from the company’s official website.

That resale filing explicitly lies to the SEC and investors:

“None of the Selling Stockholders... has had any position, office, or material relationship with us.”

That’s not just misleading — it’s materially false.

Lin is CEO and Chairman of ATHR.

Lin is also listed as General Partner of 28 Ventures on the firm’s own website.

Frank Cid is both GP of 28 Ventures and ATHR’s business development lead.

Yet in the registration, the company acted like 28 Ventures was just some random third party — not a front for insiders circumventing lock-up restrictions.

This is textbook securities fraud.

They buried the resale in an entirely separate filing and misrepresented the relationship. This wasn’t a mistake. This was intentional regulatory arbitrage, designed to let insiders dump while retail and institutional investors believed they were protected.

Worse still, Lin’s entire affiliation with 28 Ventures is omitted from his bio in the IPO Prospectus — a carefully scrubbed profile designed to mislead regulators and investors alike.

This is how the scheme worked:

Lin signs a 6-month lock-up.

He creates or activates 28 Ventures Aether as a resale vehicle.

He omits any mention of it from his IPO bio.

He registers shares for immediate resale through this shell.

He lies in the resale filing by claiming no affiliation.

Shares hit the market immediately after the IPO.

Retail bags it. Lin and Cid cash out.

They executed a fraud in broad daylight and used legal paperwork to disguise it as business-as-usual. But make no mistake: this is a violation of the lock-up agreement, Rule 10b-5 anti-fraud provisions, and potentially criminal misrepresentation.

Let’s also not ignore why this matters:

Lock-ups exist to maintain market integrity post-IPO.

They protect investors from insider dumping.

Violating them breaks trust and signals the stock is a vehicle, not a business.

The SEC, DOJ, and FINRA should immediately investigate:

Who at Aether authorized this registration?

Who at the underwriters (Spartan Capital Securities) signed off on this resale?

Why did the SEC allow this dual filing without flagging the conflict?

And why is a barred broker like Frank Cid even involved in this IPO?

Bottom line:

This isn’t a clever legal loophole — it's… in all transparency — fucking fraud.

We’re looking at a clear and deliberate lock-up violation and material false statement to the SEC.

If the SEC doesn’t act, they might as well greenlight insider fraud across the board.

THE FINRA-BARRED ENFORCER — FRANK CID

Every scheme needs a frontman. For ATHR, that’s Frank Cid — the FINRA-barred, multi-firm-hopping, private-placement peddler who somehow landed as “Head of Business Development” for a publicly traded company.

Let’s break this down like prosecutors would:

Frank Cid was permanently barred by FINRA in January 2022.

Why?

He refused to cooperate with an investigation into private securities transactions involving an entity he controlled — exactly the kind of undisclosed deal-making we now see in ATHR.

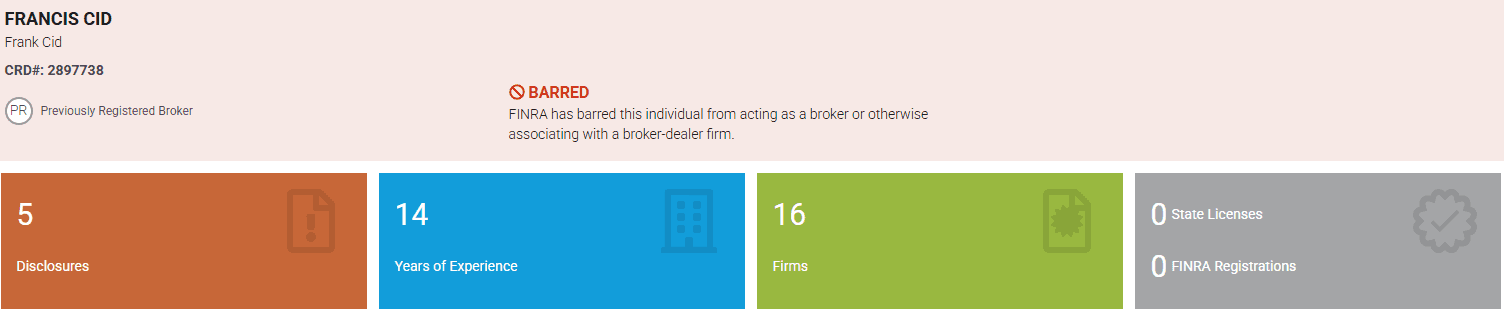

Figure: FINRA BrokerCheck Screenshot for Francis Cid

This image is a damning snapshot from FINRA’s BrokerCheck database showing that Francis Cid, also known as Frank Cid, is BARRED from acting as a broker or associating with any broker-dealer firm. His CRD# is 2897738.

His BrokerCheck record reads like a rap sheet:

17 firms in two decades

CloudChayne Inc. (IT “consulting” firm tied to shell activity)

Monolith Global Group (expense payment entity—often code for funneling insider cash)

Numerous past employers now defunct, fined, or expelled from FINRA

This isn’t a legitimate executive.

This is a penny stock hitman — the guy you call when you want to move paper through a sketchy newsletter, convince retail to chase hype, and create just enough noise to offload restricted shares quietly.

And here’s where it gets even dirtier:

Frank Cid is a General Partner at 28 Ventures.

That’s the same shell that ATHR used to offload 428,572 shares on day one of the IPO — the same resale registration that lied to the SEC and claimed 28 Ventures had “no material relationship” to the company.

So what’s Cid’s play?

He’s:

Co-running the offload vehicle (28 Ventures)

Positioned inside the company as the “business development” guy

Barred from handling securities or giving advice

Tied to multiple bankrupt, fined, and suspended entities

Involved in the pump-friendly acquisition of AltcoinInvesting.co, a dead traffic site

And they didn’t even bother to disclose his FINRA bar in any ATHR filings. It’s not in the S-1. It’s not in the 10-Q. It’s not in any press release. They’re pretending the guy doesn’t exist — while he’s helping run the operation from the inside.

Let’s be blunt:

If you were trying to build a pump-and-dump machine with plausible deniability, you’d hire Frank Cid.

He’s the archetype.

He doesn’t leave a trail — because he’s already burned the bridges behind him.

We believe:

Cid is operating in violation of his FINRA ban.

He is funneling or helping offload ATHR shares through undisclosed shells.

His past — including CrowdChayne, a company tied to bankruptcy filings — suggests a long history of financial misconduct.

This isn’t just a compliance oversight — this is an active concealment of a barred individual embedded in a public company’s capital structure and share distribution engine.

If the SEC has any spine left, it will subpoena Cid’s communications, bank accounts, and involvement in ATHR’s cap table, newsletters, and financing arrangements. There’s no way a man this radioactive landed at ATHR by accident.

SHAM ACQUISITION — ALTCOININVESTING.CO

In July 2025, ATHR proudly announced it was “expanding into the digital asset space” via the acquisition of a crypto newsletter — AltcoinInvesting.co.

They pitched it as the crown jewel of their media rollout. In reality?

It’s a dead website with less traction than a Yahoo GeoCities page in 2005.

Let’s call it what it is: a fake acquisition to justify a fake company.

The Numbers Don’t Lie:

AltcoinInvesting.co recorded only 169 visits in June 2025

Website traffic peaked for one week in mid-June — right before the acquisition

There is zero evidence of sustained subscriber growth, content delivery, or community engagement

No visible authors, archives, or actual research product — just recycled blog copy and buzzwords

And yet ATHR framed this like they acquired Decrypt or CoinDesk.

They even used it to explain their entry into the “multi-vertical financial media” market — as if acquiring a broken newsletter with triple-digit traffic counts as vertical integration.

This isn’t strategy. It’s narrative laundering.

The Playbook:

ATHR announces acquisition → Stock pops pre-market

Media and investors get baited by “digital asset” hype

No financial terms disclosed = No accountability

ATHR insiders and selling shareholders offload shares into the hype

One month later? Crickets. No updates, no roadmap, no follow-through.

Why this matters:

ATHR claims to be building a financial media empire.

Their only “asset” is a ghost-site acquisition with no operating history, revenue, or audience.

It’s the exact same playbook we’ve seen in past pump-and-dumps: acquire vaporware, claim expansion, dump stock, disappear.

We’ve seen this before with crypto newsletters, failed SPACs, and “Web3 media rollups” — but ATHR is taking it to a new level.

They aren’t even trying to hide it.

They slapped a logo on a dead domain, wrapped it in a press release, and pitched it as strategic growth — all while burying worsening financials and hiding 10-Qs on Friday nights.

Let’s be blunt:

If you’re buying ATHR based on its acquisitions — you’re buying a fucking jpeg of a newsletter.

Nothing more.

VIRTUAL OFFICE, VIRTUAL COMPANY

Aether Holdings wants you to believe it’s a bleeding-edge fintech powerhouse — slinging AI, machine learning, blockchain research, financial media rollups, and investor analytics tools.

In reality?

They’re running this entire operation out of a 235-square-foot virtual office for $12,000 a year — the equivalent of a Manhattan broom closet with a receptionist that forwards your mail.

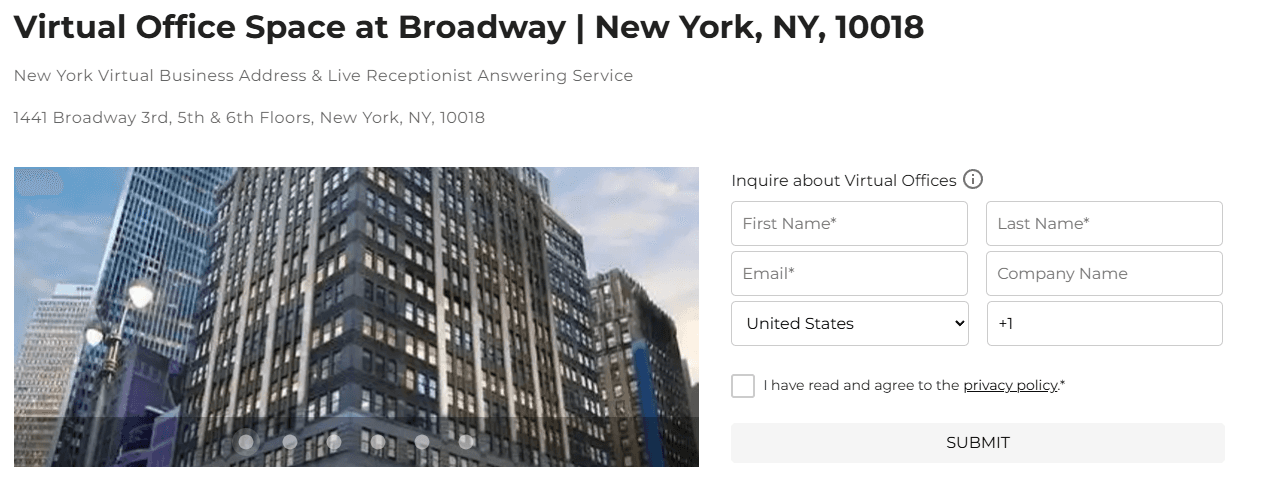

Figure: Aether’s “Headquarters” — 1441 Broadway, New York, NY

What you’re looking at isn’t the hub of a $200M AI and fintech media empire.

It’s a virtual office.

This image comes directly from the office leasing website that rents out mailboxes and fake receptionist services at 1441 Broadway — a glorified P.O. box dressed up in glass and stone. Aether leases 235 sq ft here for $12,000/year — barely enough space for a Keurig and a filing cabinet.

If you or your friends are interested in starting your own securities fraud, plans start at just $99/month and go up to $299 if you want to really impress regulators with a fake receptionist on the 3rd, 5th, or 6th floor. HERE

This is the actual listed business address for a public company claiming to operate:

Proprietary machine learning tools,

Data-driven financial media platforms,

And an aggressive M&A strategy across digital verticals.

You can't run AI analytics from a shared co-working front desk. But you can run a great pump-and-dump.

Let that sink in.

$200M market cap.

“Proprietary tech platforms.”

“Advanced tools built on machine learning.”

And they don’t even have a real office.

They also report having 11 full-time employees.

How are 11 people building AI infrastructure, analyzing multi-asset class markets, launching crypto newsletters, managing acquisitions, and running public company filings — all without desks?

$3,000 in PPE. That’s it.

From the latest 10-Q:

ATHR only lists $3,000 in property, plant & equipment.

That includes computers, office hardware, and any tangible infrastructure.

That’s not enough to furnish a high school classroom, let alone build a financial data empire.

Figure 2: ATHR’s Total Property, Plant & Equipment — A Grand Total of $2,268

This isn't a typo.

Let’s be generous and say they bought four laptops and a printer. Even that math barely works.

So where is the AI infrastructure? The computing stack? The security protocols? The data science team?

They don’t exist.

It’s smoke and mirrors — designed to inflate ATHR’s image long enough for insiders to unload stock.

The Hypocrisy is Peak Comedy:

They claim AI/ML innovation… from a rented inbox.

They claim fintech scale… with no infrastructure.

They claim research expansion… with no staff.

ATHR is the tech version of a lemonade stand pretending to be Bloomberg.

They aren’t running a company.

They’re renting a mailbox and pumping a press release machine.

Let’s be absolutely clear:

You cannot build proprietary analytics on $3,000 worth of equipment.

You cannot run a public company from a Regis co-working space.

You cannot claim scalability without infrastructure, bandwidth, or staff.

And if you do all of the above while hiding it from investors?

That’s securities fraud through omission.

This company is virtual in every way that matters — except the millions insiders are quietly extracting.

UNDISCLOSED SPAC TIES & EMPLOYMENT CONTRACT BREACH

Nicolas Lin doesn’t just run Aether Holdings — he’s moonlighting as the Chief Financial Officer and Director of another publicly traded entity: Origin Investment Corp I (ORIQ), a SPAC that IPO’d in early 2025.

Here’s the problem:

📌 ATHR never disclosed this in any of their filings.

📌 Lin’s employment agreement at ATHR forbids it.

Let’s go straight to the smoking gun clause from his contract:

“The Executive agrees to devote his full customary business time and energies to the business of the Company and/or its affiliates and to perform his duties hereunder on an exclusive basis…”

There’s no gray area here. No loophole. No ambiguity.

Lin legally agreed to exclusivity. Then he turned around and took an executive position at another public company.

And this wasn’t some side hustle that popped up later — ORIQ filed its first S-1 on January 8, 2025, a full three months before ATHR’s April IPO. Lin’s been listed as CFO since January 7, 2025.

This is textbook breach of fiduciary duty.

But the real kicker? This isn’t just a governance issue — it’s a deliberate omission of a material executive conflict during an IPO.

Let’s break down why that’s a huge deal:

Lin is signing financial statements and SEC filings at two separate public companies simultaneously.

He failed to disclose this dual role in Aether’s 424B4 Prospectus.

He violated the very employment agreement that gave investors confidence he’d be full-time at ATHR.

The SPAC world is notorious for backdoor enrichment and shadow deal flow — and Lin’s ties to 28 Ventures and ORIQ suggest he’s playing both sides.

Whether it’s incompetence or concealment — this is a black hole of governance.

Investors trusted Lin to run ATHR.

Instead, he’s juggling shell games across multiple tickers and acting like the rules don’t apply.

They do. And we’re making sure the SEC gets the memo.

RELATED PARTY ENRICHMENT — MONIC WEALTH SOLUTIONS

If there’s one thing ATHR does consistently — it’s pay insiders while pretending they don’t exist.

Let’s talk about Monic Wealth Solutions Ltd., a so-called consulting firm that received 50,896 shares of ATHR stock (valued at $42,753) for “consulting” and “marketing services” during the six months ending March 31, 2024.

But here’s the catch:

📌 In the same SEC filings, ATHR states that Monic Wealth Solutions is a "related party."

📌 The company paid them again — $10,689 in Q1 and $50,127 over six months — for so-called “sales channel support.”

📌 Then suddenly in 2025? No payments. No shares. No services. Nothing.

Looks like the job was done: prop up the books, move the stock, and vanish.

But who exactly is behind Monic Wealth?

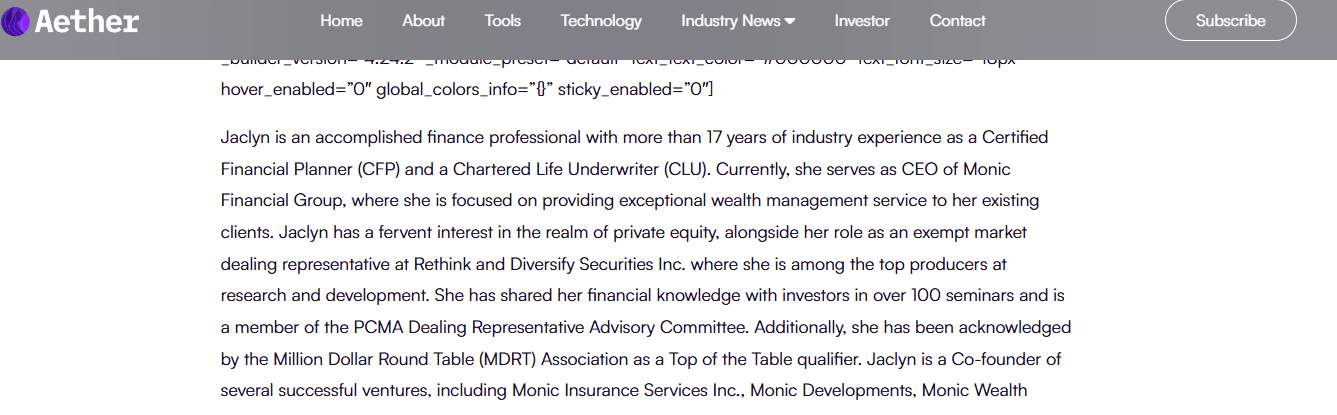

Enter Jaclyn — the CEO of Monic Wealth Solutions, Monic Insurance, and Monic Developments.

She's also proudly listed on Aether’s site as a “top R&D representative” and has deep ties across this entire ecosystem of shells.

According to Aether’s own site (Figure: below), Jaclyn is:

A “Certified Financial Planner”

An “exempt market dealer” at Rethink and Diversify

A co-founder of multiple Monic-branded ventures

Deeply involved in “private equity” and wealth management

Supposedly unaffiliated? Give us a break.

This is a textbook related-party pump:

Issue insider shares to a friendly firm.

Classify it as “consulting.”

Clean up the cap table and financials right before IPO.

Avoid disclosing the full scope of insider ties.

Figure: Screenshot from Aether’s team bio page confirms Jaclyn’s ownership of Monic entities and her role as a private equity operator tied to the company. This completely undermines the notion of Monic as an arm’s-length service provider. HERE

Figure: SEC filing (Note 8B) shows 50,896 shares issued to Monic Wealth Solutions Ltd. — equating to $42,753 worth of “consulting” in a conveniently pre-IPO window.

So let’s ask:

Where’s the deliverables?

Where’s the third-party validation?

Why did all services suddenly stop the moment ATHR went public?

You don’t have to be Sherlock Holmes to figure it out — this was a pre-IPO insider enrichment scheme.

And guess what?

That same Monic network is now gone silent — no contracts, no press, no pipeline.

Just the kind of cleanup you’d expect once the pump is complete.

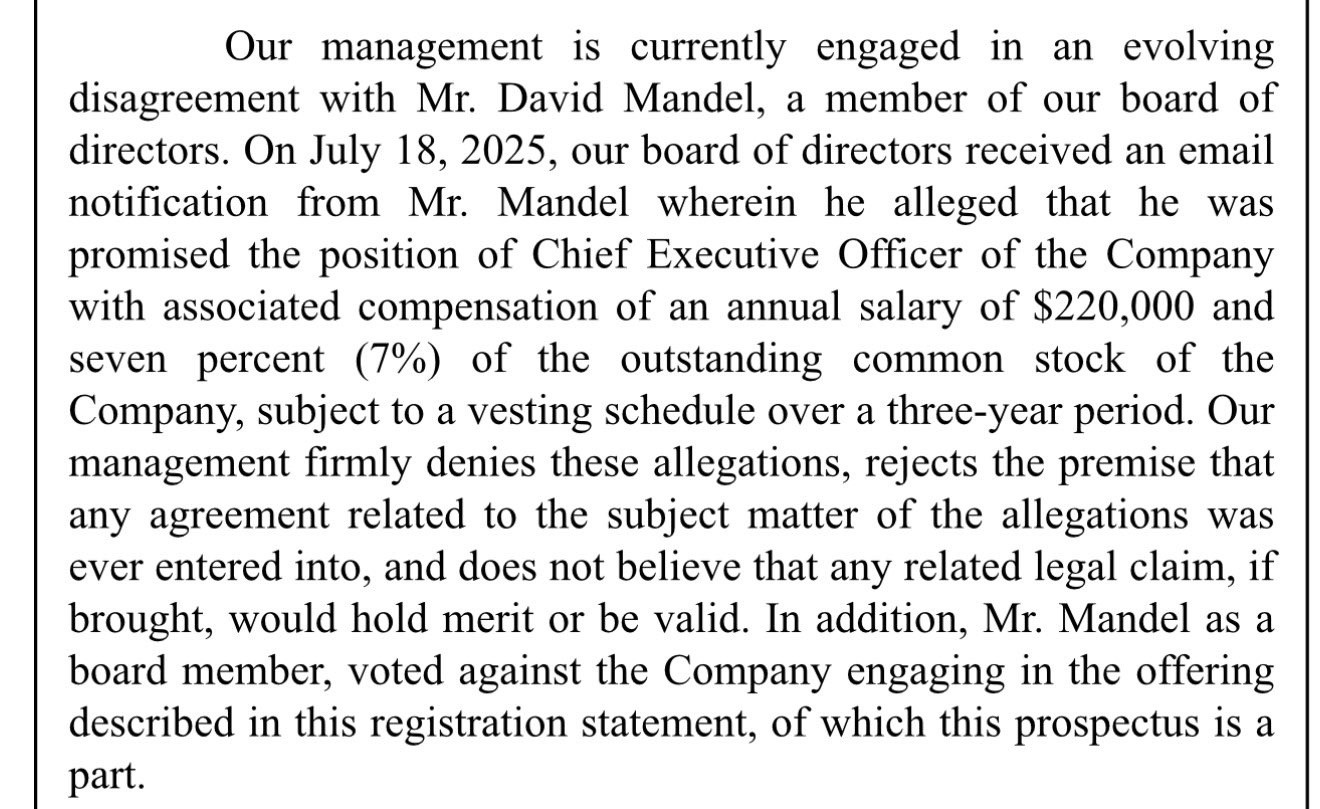

Boardroom Betrayal: The David Mandel Dispute

Just days before this report’s release, Aether Holdings ($ATHR) revealed it’s embroiled in an internal fallout with board member David Mandel—and it’s not some minor squabble.

Figure:

Excerpt from Aether Holdings' registration statement disclosing an internal dispute with board member David Mandel. Provided by X account @maninapurpledr1

According to SEC filings, Mandel claims he was promised the CEO role, a $220,000 salary, and a 7% equity stake, vesting over three years. In response, ATHR management issued a classic “we deny everything” boilerplate, claiming no such deal ever existed and preemptively dismissing any legal action as “meritless.”

But here’s the kicker: Mandel voted against the very offering this prospectus represents.

That’s not just dissent—that’s a flashing red warning from inside the boardroom.

We’ll let readers decide who’s lying.

But it’s clear the internal fractures are now too big to hide.

DUMP-AND-DISAPPEAR — THE FRIDAY NIGHT 10-Q DUMP & ALTCOININVESTING PR GAME

You know a company’s full of shit when it hypes fake acquisitions on weekdays…

…but dumps earnings when nobody's watching.

On Friday night, May 16, 2025, Aether filed its 10-Q for the quarter — without a press release.

No earnings call. No investor update. No transparency. Just a quiet, late-week filing buried under the radar.

This isn’t coincidence.

It’s a move straight from the penny stock fraud playbook:

File bad or embarrassing results on a Friday night — when retail and institutional investors are offline.

Skip the press release so no media outlet or algorithmic alert catches it.

Hope no one notices the abysmal fundamentals.

Let’s be clear — ATHR had every reason to hide:

Just $2,268 in net property & equipment (See Figure: hardware assets totaled less than what you'd spend on a mid-range gaming PC).

A glorified mailbox office in Manhattan.

No revenue-generating operations of substance.

Instead of addressing any of that, they tried to distract the market with a shiny object — the acquisition of a dying crypto blog.

THE ALTCOININVESTING.CO SHAM

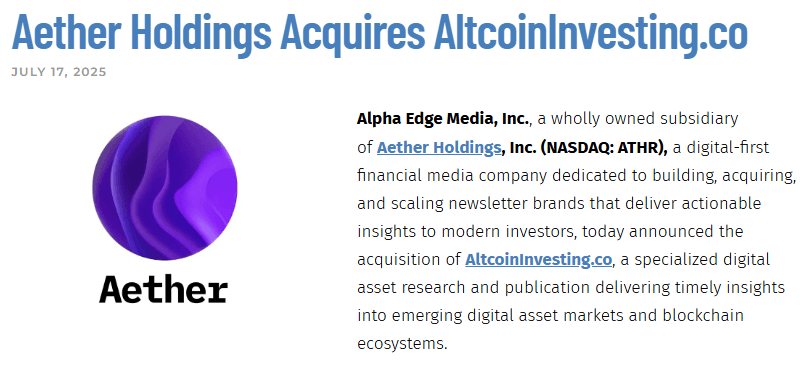

In July 2025, ATHR announced its “strategic acquisition” of AltcoinInvesting.co — a supposedly “growing Web3 media brand.”

Figure: Press release from Aether Holdings (NASDAQ: ATHR) dated July 17, 2025, announcing the acquisition of AltcoinInvesting.co by its wholly owned subsidiary, Alpha Edge Media, Inc.

Reality? It’s a dead site.

Here’s the data:

169 total visitors in June 2025.

Traffic peaked for a single week, then flatlined.

No active newsletter, podcast, or content cadence.

Zero visible monetization or customer funnel.

This was not a business.

This was a domain with Google dust on it.

So why buy it?

To distract from their non-existent business operations.

To inject buzzwords like “crypto,” “blockchain,” and “Web3” into their press cycle.

To justify executive pay and stock-based comp by pretending to execute on “acquisitions.”

This is what pump schemes do:

Hype acquisitions no one asked for.

Keep investors focused on momentum.

Use narrative noise to cover financial rot.

Figure: AltcoinInvesting.co’s June traffic analytics show <200 visits — laughable for a “leading crypto media outlet.”

This is textbook manipulation and a flashing red signal for regulators:

Hide the truth.

Flood the market with hype.

Let insiders quietly exit.

We’ve seen it before.

And unless the SEC, DOJ, or FINRA steps in — we’ll see it again.

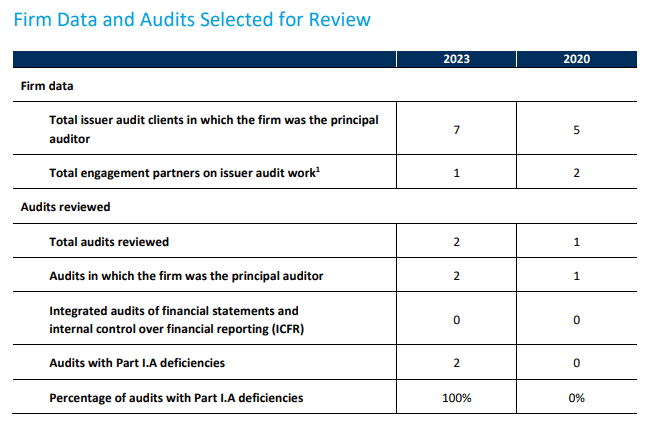

THE AUDITOR FROM HELL — ZH CPA’S LONG TRAIL OF TRASH AUDITS

When a company wants to keep regulators out and the truth buried, it hires a “see-no-evil” audit firm.

ATHR did exactly that — by selecting ZH CPA, LLC as its independent auditor.

Let’s be blunt:

ZH CPA isn’t a real watchdog — it’s a rubber stamp factory for sketchy microcaps.

WHO IS ZH CPA, LLC?

A little-known audit firm based in New Jersey.

Flagged by Canadian audit regulators (CPAB) for deficiencies.

Raised red flags by PCAOB for audit quality and oversight failures.

Frequently used by reverse merger shells, Chinese backdoor listings, and companies with histories of restatements.

You don’t hire ZH CPA if you want real scrutiny —

You hire ZH CPA when you want creative accounting, minimal oversight, and plausible deniability.

ATHR’S AUDIT TIMING SCAM

Let’s rewind:

📉 On May 16, 2025, ATHR filed its Q2 10-Q late on a Friday night — the classic time window used to bury bad news.

📭 The company issued no press release, made no media outreach, and hid the filing from retail radar.

🧾 The filing was signed off by ZH CPA, LLC, who — unsurprisingly — didn’t flag:

The CEO’s lock-up violations

The CEO’s undisclosed SPAC employment

The firm’s lack of tangible assets (just $2,268 in net PP&E — see Figure)

The virtual office scheme

The related-party deals with Monic Wealth Solutions

The insider relationship with 28 Ventures

ZH CPA didn’t miss this because it was subtle.

They missed it because they weren’t looking.

ZH CPA’S TRACK RECORD: FAILURE TO PROTECT

Let’s be clear — this isn’t the first time ZH CPA has been involved in questionable auditing.

In fact:

Multiple PCAOB inspection reports cite them for audit failures.

ZH CPA was the auditor of record for at least three companies that later restated financials or were delisted.

Hiring ZH CPA is like installing a screen door on a submarine — you’re going to sink, and everyone knows it.

Figure: PCAOB Inspection Results — ZH CPA, LLC (2023)

Screenshot from the PCAOB’s 2023 inspection report on ZH CPA, showing a 100% failure rate in audits reviewed. This level of deficiency underscores the auditor’s unreliability and calls into question the integrity of Aether’s financial statements. HERE

CONCLUSION: ZH CPA ENABLES THE SCHEME

The audit process is supposed to protect investors.

But in this case, it protected fraud.

Aether Holdings didn’t hire an auditor to keep them honest —

They hired ZH CPA to look the other way while they ran the playbook.

And ZH CPA delivered —

with a clean opinion on what we believe is one of the most deceptive microcaps currently trading on NASDAQ.

SHADOWY PAST — THE PATTERN OF DECEPTION BEHIND ATHR’S ARCHITECTS

If you think ATHR’s problems began with its April IPO, you’re not paying attention. This isn’t a one-off — it’s a repeat performance from serial operators who’ve weaponized disclosure rules, recycled shell games, and operated in regulatory blind spots for years.

Let’s take a closer look at the playbook they’ve run before — and are running again.

1. CrowdChayne & Frank Cid’s Skeletons

Before resurfacing at ATHR and 28 Ventures, Frank Cid was tied to CrowdChayne, a failed crowdfunding platform riddled with irregularities. Court filings reveal its presence in bankruptcy documents. This isn’t just a failed startup — it’s a vapor trail of unpaid debts, zero transparency, and broken promises. Cid didn’t stumble into fraud — he’s been orbiting it his entire career.

Why this matters: ATHR investors are once again placing their faith in a man permanently barred by FINRA, whose last venture ended in court.

2. Melissa Garlough & the Silent Filing

A Form D linked to an entity tied to ATHR was signed by Melissa Garlough, a name rarely found elsewhere in the ecosystem — until you start digging. We reached out via email and phone — no response. Not a denial, not a defense — just silence.

Why this matters: Key disclosures are being rubber-stamped by people who appear to play “hit-and-run” roles in these filings, then disappear from view. This isn’t governance — it’s a legal smokescreen.

3. Lin’s Past Track Record

Aether CEO Nicolas Lin is no stranger to failing upward. Before ATHR, he sat on the boards of multiple low-float penny stocks, including:

St. James Gold Corp (TSXV: LORD; OTCQB: LRDJF) — a speculative mining firm that cratered.

Technovative Group Inc. — long dormant.

Moxian, Inc. — a failed China-based social media play.

Rebel Group, Inc. — another forgotten shell.

None of these companies produced durable value for shareholders. What they did produce? Dilution, glossy press releases, and exit opportunities for insiders.

4. Advance Opportunities Fund & SPAC Recirculation

Lin’s involvement with Advance Opportunities Fund (a known Hong Kong-based financier of microcaps) shows a consistent strategy of:

Taking control of distressed or thinly traded shells

Injecting vague “AI” or “media” narratives

Raising low amounts of capital

And quietly exiting before regulators catch on

Now with ATHR, it’s déjà vu — but this time the stakes are higher.

Conclusion: The Architects Haven’t Changed — Just the Paint Job

Aether Holdings didn’t emerge from innovation — it emerged from a recycled ecosystem of shady operators, empty entities, and regulatory neglect.

The CEOs, promoters, and financiers involved in ATHR have consistently left a trail of destruction behind them — and we believe ATHR is merely the next domino in line.

This isn’t incompetence.

It’s a business model.

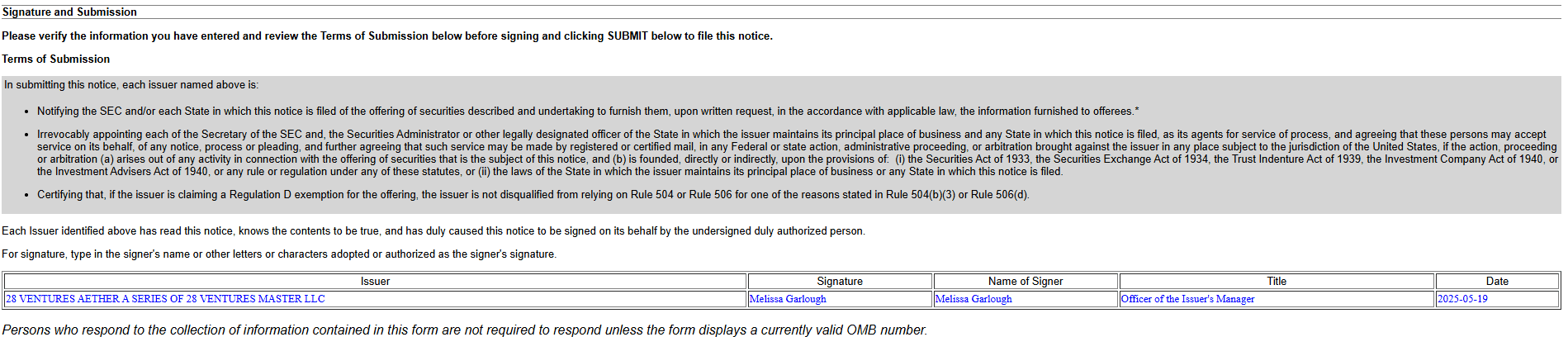

THE PHANTOM SIGNATORY — WHO IS MELISSA GARLOUGH?

Let’s start with the Form D filing:

SEC Form D (Filed Jan 2, 2025):

Entity: 28 Ventures Aether, a Series of 28 Ventures Master LLC

Figure: Screenshot of Form D Signature Section Showing Melissa Garlough Signing as Officer of the Issuer’s Manager

This figure shows the official SEC Form D submission for 28 Ventures Aether, a Series of 28 Ventures Master LLC, filed on May 19, 2025. The form is digitally signed by Melissa Garlough, who is listed as the “Officer of the Issuer’s Manager.”

Signed by: Melissa Garlough, claiming to be the Manager of the issuer. On paper, it looks like a standard regulatory filing. But there’s one massive problem: Melissa Garlough has no visible connection to 28 Ventures, its affiliates, or the securities industry at all.

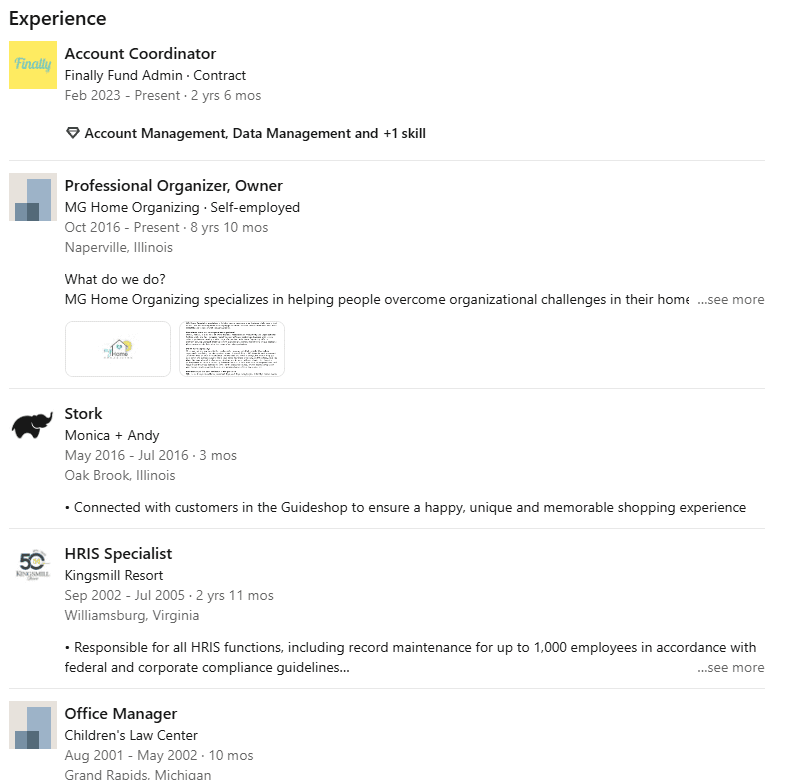

Her Background: A Strange Fit for Securities Filings

A quick search of Melissa Garlough’s LinkedIn profile shows a radically different career trajectory:

Role | Dates | Details |

|---|---|---|

Account Coordinator at Finally Fund Admin | Feb 2023 – Present | Contract admin work |

Professional Organizer, Owner | 2016 – Present | MG Home Organizing (personal productivity) |

Stork at Monica + Andy | 2016 | Retail sales in baby boutique |

HRIS Specialist at Kingsmill Resort | 2002 – 2005 | HR and data recordkeeping |

Office Manager, Children’s Law Center | 2001 – 2002 | Administrative work |

Nowhere — not once — is there a trace of:

Experience in venture capital

Involvement in private placements

Participation in startups, finance, or securities compliance

Connection to Nicolas Lin, Frank Cid, or 28 Ventures

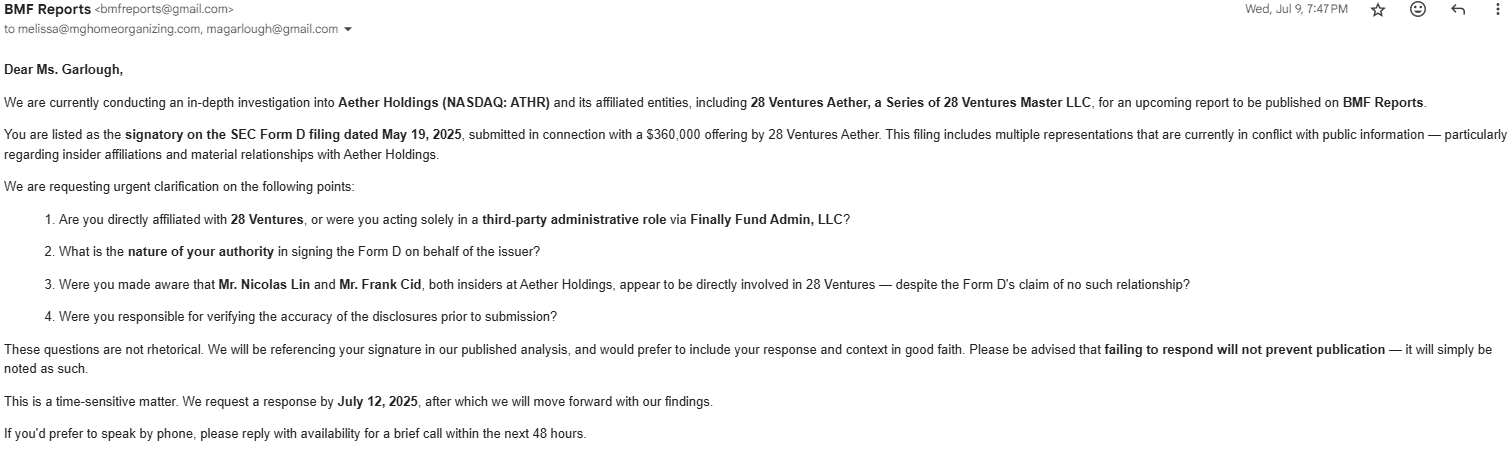

Figure: Screenshot of BMF Reports' email correspondence to Melissa Garlough requesting clarification regarding her signature on the SEC Form D submitted by 28 Ventures Aether.

We reached out to Melissa Garlough via multiple calls and emails to clarify her affiliation with 28 Ventures. Despite repeated attempts, she declined to comment. We’ve included a screenshot of our outreach below for transparency (see Figure: Email Correspondence with Garlough).

This silence is deafening. When the only person willing to sign the Form D can’t—or won’t—explain her role, you know the foundation is rotting.

This is fraud. On paper. In plain sight.

Yet somehow, this suburban home organizer from Naperville, Illinois, is filing securities documents with the SEC on behalf of a venture firm selling hundreds of thousands of dollars in stock?

Why This Stinks

This isn’t just odd — it’s suspicious as hell.

There are two possibilities here, and neither are flattering:

Melissa was used as a “clean” name — someone disconnected from the scheme who could sign documents and avoid scrutiny. Think: plausible deniability.

She’s a ghost signer — a complicit party signing off on deals with no actual role in the issuer, potentially to obscure who’s really running the show (Lin and Cid).

Regulatory Implications

Signing an SEC Form D falsely — especially on behalf of an entity where you're not actually a manager — violates securities laws. The penalties range from:

Civil enforcement actions

Criminal referrals

Invalidating the exempt offering

Disgorgement of profits

If Melissa is not legally managing 28 Ventures Aether, her signature is fraudulent. If she is managing it… where’s the proof?

Figure: Screenshot from Melissa Garlough’s LinkedIn profile showing a total lack of professional background in venture capital or securities — yet she is listed as a “Manager” on Form D filings for 28 Ventures Aether. HERE

Conclusion: Another Shell, Another Ghost

The appearance of Melissa Garlough in Aether’s filings isn’t just a paperwork quirk. It’s evidence of a deliberate effort to obscure ownership, mislead regulators, and bury accountability behind a firewall of plausible nobodies.

This is how fraud operates — not with fireworks, but with quiet signatures and invisible names.

THE 28 VENTURES PIPELINE — A SERIAL DUMP ENGINE IN MOTION

At first glance, 28 Ventures looks like an emerging VC fund or boutique finance firm. But beneath the generic website and buzzword-laden copy lies a repurposed securities dumping vehicle, recycling equity across microcap schemes with minimal oversight.

Here’s the pattern:

28 Ventures shows up post-IPO with large share allocations.

It rapidly resells these shares under the guise of a “registration for resale” while insiders pretend to stay locked up.

The firm hides its insider ties to the issuer — see the false no-relationship claim in ATHR’s S-1.

It installs paper officers like Melissa Garlough to execute filings, keeping the real control structure hidden.

Why does this matter?

This isn’t 28 Ventures' first rodeo.

We’ve identified multiple shell entities and pseudo-series LLCs operating under the 28 Ventures Master LLC umbrella — each used to:

Accept large pre-public equity stakes,

Quietly list resale registrations on EDGAR,

And distribute shares to anonymous buyers or insiders under the radar.

This pattern is eerily similar to classic Reg D / Reg S pump-and-dumps that dominated penny stock frauds in the 2000s. But now they’re dressed in Series LLC wrappers and Delaware boilerplate.

28 Ventures is not a passive investor. It’s a conduit for illicit liquidity events — and in ATHR’s case, it served as the CEO’s own off-ramp.

The SEC should audit all 28 Ventures filings and investigate:

How many issuers are tied to Lin or Cid?

How many resale registrations were filed during lock-up periods?

Who are the beneficial owners behind the Series entities?

This isn’t a one-off. It’s a replicable blueprint.

And Aether Holdings is just the latest mark.

CLOWN CAR CAP TABLE — WHO ACTUALLY OWNS AETHER?

Let’s talk ownership — or rather, the obfuscation of it.

Aether’s cap table is a chaotic mess of loosely affiliated shell entities, shady offshore structures, and intentionally opaque disclosures. Here's what we found:

28 Ventures Aether, which dumped 428,572 shares post-IPO, claims in its own SEC filing that none of its principals have any material affiliation with ATHR.

This is a lie. It’s co-managed by ATHR CEO Nicolas Lin and FINRA-barred Frank Cid.

The Form D for 28 Ventures was signed by Melissa Garlough, a woman with no known employment, board seat, or formal affiliation with 28 Ventures. Her name appears nowhere else in Aether's ecosystem — not in press releases, corporate docs, or LinkedIn.

We reached out via email and phone. No comment. No explanation. Nothing.

The deeper we dig, the more this looks like an intentional shell game designed to:

Hide insider selling.

Dodge lock-up rules.

Obscure beneficial ownership.

The SEC mandates that material relationships be disclosed in resale filings.

Instead, ATHR’s team swore there was none — while dumping shares through a firm they control.

This isn’t a sloppy oversight — this is deliberate fraud.

It’s not just who owns ATHR — it’s how they’ve structured it to avoid telling you.

CROWDCHAYNE — THE ROTTING CORPSE IN CID’S CLOSET

Before Frank Cid was helping dump ATHR shares through 28 Ventures, he was running another operation — CrowdChayne.

You won’t find it in Aether’s filings.

You won’t hear it mentioned in any press release.

But it shows up where it matters — in bankruptcy court.

CrowdChayne was a now-defunct "fintech marketing" firm founded by Frank Cid that popped up in multiple bankruptcy records — and, like clockwork, it followed the same playbook:

Pump microcaps through shady newsletters and fake momentum

Act as a proxy marketing firm to goose early volume

Disappear into the ether when liabilities surface

Sound familiar?

Why it matters:

CrowdChayne’s failure is never disclosed in any of Cid’s public bios or ATHR filings.

The firm is likely a predecessor shell to the current newsletter/marketing operation Aether is trying to run via AltcoinInvesting and other acquisitions.

Cid’s pattern of starting hype firms, dumping shares, and walking away is undeniable.

This is what you get when you hire a FINRA-barred broker with a trail of failed ventures and court filings as your head of biz dev.

This isn’t just a red flag. It’s a fucking flare gun.

FINAL STATEMENTS: THIS ISN’T A COMPANY — IT’S A FUCKING EXIT PLAN

Let’s be crystal fucking clear:

Aether Holdings is not building a media empire. It’s building a runway — for insiders to cash out and vanish.

Behind the AI buzzwords and ghost acquisitions lies a virtual office, $3,000 in assets, 11 employees, and a CEO who's too busy violating lock-up agreements and lying to regulators to pretend this is anything but a glorified liquidation vehicle.

The facts aren’t gray. They’re radioactive:

Nicolas Lin sold shares through a shell entity he controls with a FINRA-barred fraudster — while legally locked up.

SEC filings outright lied about 28 Ventures’ relationship to the company.

The company used shady auditors and dumped its 10-Q late on a Friday, hoping no one would notice the rot.

Every acquisition is smoke and mirrors — AltcoinInvesting.co had less traffic than a middle school blog.

The only thing “proprietary” here is how brazen the playbook is.

This is what fraud looks like when it puts on a suit and files an S-1.

Our conviction? Maximum.

This isn’t a valuation mismatch. This is a regulatory time bomb — and we believe it’s only a matter of time before the SEC slaps a freeze on this house of cards.

ATHR isn’t misunderstood.

ATHR isn’t early.

ATHR is a ticking fucking grenade.

And when it blows — we won’t be surprised.

*We're short at $12.63*

HONORABLE MENTIONS

Some people don’t just watch — they warn. This report exists because of the voices that kept speaking up when everyone else stayed quiet.

To "Cashflow" — the real MVP behind the curtain. Your late-E-Mails, brutal honesty, and steady loyalty lit the path. You were in the trenches with us.

To @maninapurpledr1 — your words hit when they needed to. You reminded us this work isn’t just data, it’s a mission.

To @joinyellowbrick — months ahead, fearless and loud. You saw the scam unfolding and never flinched.

And to @iotaresearch — sharp, relentless, and always a step ahead.

Thank you all. You made this more than a report — you made it a reckoning.

LEGAL DISCLAIMER

This report contains opinions, analysis, and commentary based entirely on publicly available information, regulatory filings, corporate disclosures, and the authors’ own investigative interpretation. At the time of publication, we hold a short position in Aether Holdings (NASDAQ: ATHR). We stand to benefit if the company’s stock declines in value. We’re not hiding that — we’re proud of it. We put our money where our mouth is. We are have not received compensation from any third party to produce this report. Everything here is our honest belief — blunt, sharp, and unfiltered.

We are not financial advisors, nor are we responsible for your trades. We do not give investment advice. We expose fraud. We connect dots. We publish facts. If you buy this stock after reading this — that’s on you. If you sue us for writing it — that’s on your lawyer’s malpractice insurer.

To Nicolas Lin and Francis Cid:

Let’s be clear. This isn’t market noise — this is a forensic trail of your own dirty laundry. We didn’t fabricate documents. We didn’t forge your signatures. We didn’t falsely file Form D with a random stranger’s name. You did all that. We just read it, connected the dots, and hit "publish."

Don’t like the heat? Maybe don’t light the match.

And before you waste your weekend drafting some 3-page cease and desist letter: don’t. Save it for the SEC, FINRA, DOJ, or the class-action lawyers already circling this dumpster fire. We’re not afraid of you. We don’t need a PR firm or a legal team on retainer to call bullshit when we see it. We’ve got something more powerful — the truth, the filings, and a growing crowd of pissed-off investors ready to hold you accountable.

To disgruntled shareholders, bagholders, or anyone who fell for the smoke and mirrors:

We’ve been there. We don’t mock you — we warn you. If this report helps you exit the con before the collapse, consider that a win. If it lights the fuse on a class action, consider that justice.

We publish under the BMF banner for a reason:

Bad. Mother. Fuckers.

No filters. No sponsors. No backroom deals.

Just the facts — raw, ugly, and razor sharp.

Now go ahead — forward this to your lawyer. We’ll forward it to ours.

And to the regulators: your move.

— BMF Reports