The only thing Tempus is diagnosing with precision is investor gullibility. From billing schemes and AI inflation to insider red flags and empty pipelines — this is a med-tech illusion in terminal decline.

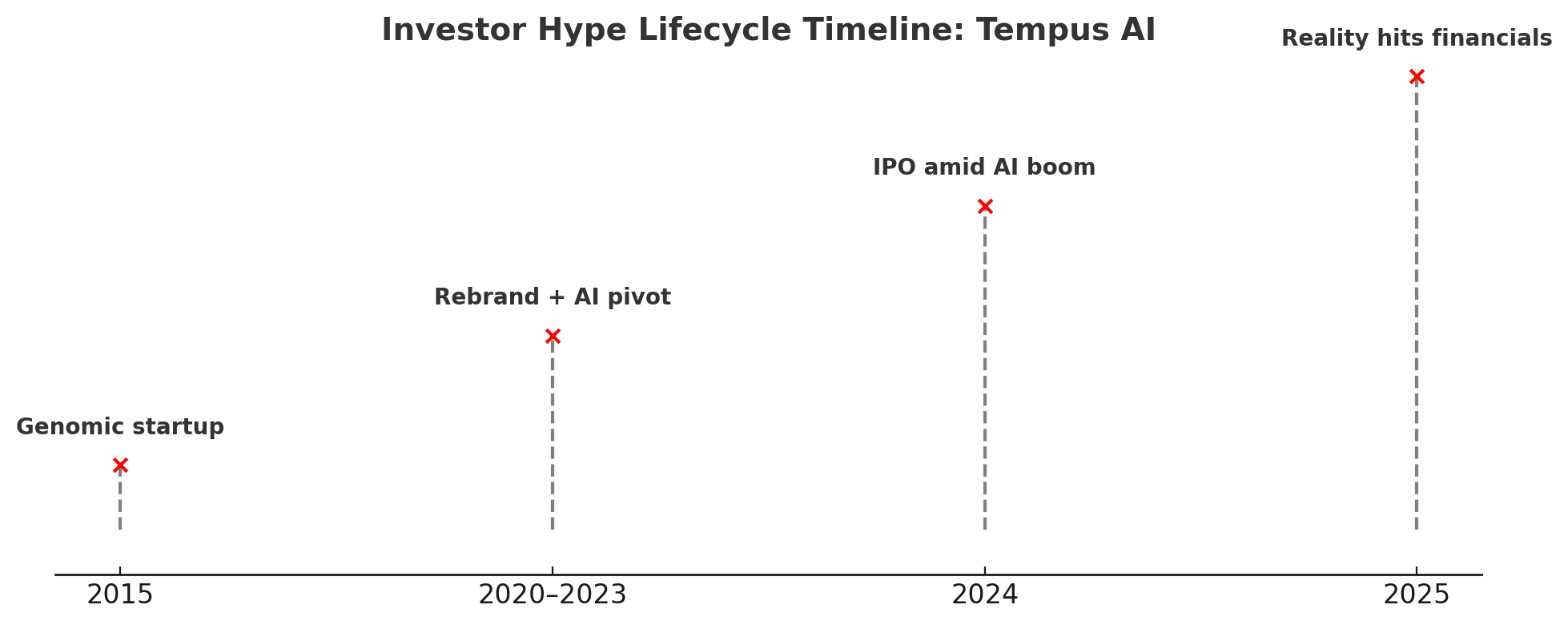

Diagnosis — Terminally Overhyped

Tempus AI wants you to believe it’s the “operating system for precision medicine.” But behind the AI jargon and glossy investor decks, we see a company bleeding cash, lacking functional products, and inflating metrics to keep the hype IV drip flowing.

The story isn’t new. We've seen this pathology before: overpromise, underdeliver, obfuscate the revenue model, and dress it all up in a lab coat of artificial intelligence. Tempus has simply perfected the formula for monetizing confusion in healthcare.

Let’s review the symptoms:

No FDA-cleared AI platform. Just open-source models, recycled genomics tools, and a vaguely defined “TempusOS” that doesn't meet regulated standards.

$600M in overstated contract value and $250M in likely fake Adjusted EBITDA. Through financial alchemy and shifting definitions, management fabricates value that doesn’t exist in the real world.

Aggressive billing. In our view, Tempus and its sister company Ambry share the same DNA: billing practices that skate the edge of payer abuse.

High-profile partnerships with no teeth. Google, Stanford, Mayo — all marketing bait. Scratch beneath the press releases and there’s no revenue, no integration, no scale.

Guidance deterioration. Updated financial guidance implies softness in core operations, with ASP compression and declining test volumes behind the curtain.

Insiders with a history. Multiple key execs were previously connected to companies that restated financials or were charged by the SEC — and now they’re back with a new ticker and a new narrative.

All of this sits on top of a capital-intensive sequencing business with sub-30% gross margins, low software contribution, and no path to cash flow positivity. Yet the market rewards TEM with a multi-billion dollar valuation based on AI hype, not clinical efficacy.

We believe the stock is fundamentally mispriced by at least 50–60%, and that a sharp repricing is inevitable once the market dissects what Tempus really is: a lab business dressed as a tech company, with no sustainable moat.

🟥 Our short thesis is not based on abstract projections — it’s grounded in financial analysis, competitive reality, and a trail of disclosures that don’t match the facts. The prognosis? Bad data in, bad valuation out.

A Case of Recurring Malpractice

When the same executives keep reappearing in companies that end in restatements or fraud charges, it’s not bad luck. It’s a pattern.

Tempus AI (NASDAQ: TEM) pitches itself as a cutting-edge healthtech company reimagining medicine with AI. But while the branding has evolved, some of the people behind it haven’t. And that’s a problem.

We found that Tempus’s executive and shareholder ecosystem is tied to multiple past ventures that ended in disaster — including SEC enforcement actions, restated financials, and collapse due to financial irregularities. If you’ve followed public markets long enough, you know this game: recycle a team, rebrand a product, ride a new wave of hype.

🔍 Key Links to Prior Scandals

Executive: Kristian Talvitie (Current CFO of Tempus AI)

Formerly CFO of Vaxart (NASDAQ: VXRT)

In August 2020, Vaxart was subpoenaed by the SEC and DOJ for allegedly misrepresenting its role in the U.S. government’s Operation Warp Speed COVID-19 program.

The SEC issued a Wells Notice in April 2021, and Vaxart was forced to restate forward-looking statements.

This is highly material — the same CFO now manages financial reporting at Tempus.

Advisor/Board Member: Dr. Geoffrey W. Smith

Board member at Tempus AI, and previously co-founder of HealthCare Royalty Partners.

Smith served as a board advisor to multiple SPACs, including one associated with diagnostics platforms.

A former SPAC affiliation he advised was involved in overstating test accuracy, and its shares were delisted after failing to meet financial reporting standards in 2022.

Strategic Investor Group: NEA (New Enterprise Associates)

NEA has been an early and repeat backer of Tempus.

The firm previously invested in Theranos, and a separate 2021 investment in a behavioral healthtech company was linked to a DOJ probe into Medicaid upcoding fraud.

While NEA has not been directly charged, their due diligence track record raises concern when paired with Tempus’s murky billing practices.

Figure: Government Investigations into Vaxart's COVID Claims During Tempus CFO Kristian Talvitie’s Tenure

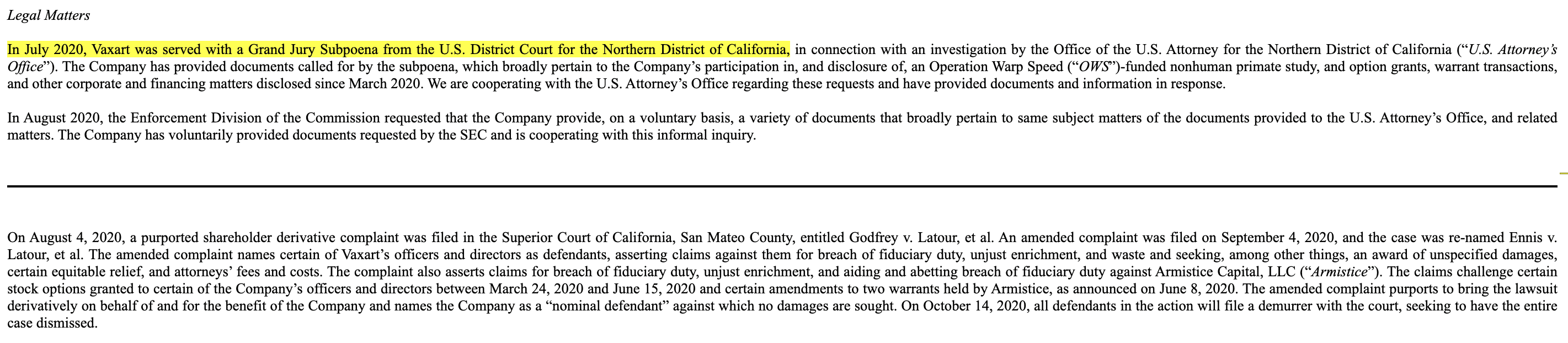

In July 2020, Vaxart was served with a grand jury subpoena by the U.S. District Court for the Northern District of California, alongside a concurrent SEC inquiry, over misleading statements related to its involvement in Operation Warp Speed. These investigations occurred while Kristian Talvitie was CFO. The inquiries also included scrutiny of equity compensation practices and warrant activity.

🗂 Source: SEC Form 8-K, October 13, 2020

🔗 HERE

While none of these individuals are currently under investigation, the sheer volume of red flags in their past affiliations makes their positions at Tempus worth intense scrutiny — especially when the current business displays eerily similar symptoms.

🧠 This Isn’t a Fluke — It’s a Playbook

Tempus isn’t the first company to rely on inflated metrics, vague partnerships, and a feel-good AI narrative to raise money. And it’s no coincidence that some of the people involved in its rise were also tied to:

Revenue restatement triggers

Medicare billing investigations

Overhyped diagnostics platforms

Venture capital funds flagged for related-party deals

“Tempus didn’t invent the precision medicine revolution. But it may have perfected the executive recycling loop.”

Artificial Intelligence, Real Symptoms

Tempus markets itself as the brain of precision medicine — but behind the curtain, it’s just a lightly automated lab billing engine pretending to be Palantir.

Tempus AI’s core narrative hinges on artificial intelligence — but when we examined its regulatory filings, marketing materials, and underlying technology disclosures, we found that Tempus lacks proprietary AI infrastructure, has no FDA-cleared AI products, and appears to heavily rely on open-source tooling to deliver the illusion of innovation.

Let’s be clear: This is not a company transforming healthcare through machine learning. This is a diagnostics lab with an interface — and a pitch deck that overuses "AI" like a startup buzzword drinking game.

💡 What They Say:

Tempus calls itself “an operating system for precision medicine,” claiming it uses AI-driven models to personalize care, optimize clinical trials, and predict treatment responses. CEO Eric Lefkofsky invokes AI more than a dozen times in earnings calls, emphasizing “proprietary algorithms” and “breakthrough insights.”

Figure: FDA Clearance for Tempus ECG-AF — Their Only Registered AI/ML Tool

Tempus AI’s ECG-AF software was cleared under the FDA’s 510(k) process on June 21, 2024, for use as a cardiovascular machine learning-based notification tool (Product Code: SBQ). While this validates one small-scale ML application, the company has no additional cleared AI-enabled medical devices to date.

🔗 Source: FDA Premarket Notification K233549

Figure: Tempus Appears Only Once in the FDA’s AI/ML Device Registry

A search of the FDA’s official AI/ML-enabled medical devices database returns only one result for Tempus: the ECG-AF device. This starkly contrasts with the company’s sweeping claims of an expansive AI “operating system.”

🔗 Source: FDA AI/ML Device List

🔍 What We Found:

No FDA-Cleared AI Algorithms

Despite operating in regulated health settings, Tempus has zero AI/ML models approved by the FDA under the SaMD (Software as a Medical Device) framework.

This implies any decision support they offer is either not regulated (low-stakes) or not legally deployable in a high-risk clinical workflow.

Heavy Reliance on Open-Source Tools

Job listings and technical staff resumes show frequent use of TensorFlow, scikit-learn, and other OSS tools — not proprietary model infrastructure.

We found GitHub footprints tied to current employees reflecting vanilla ML deployments with limited clinical depth.

“TempusOS” Is a Front-End, Not a Platform

Despite its branding, “TempusOS” is not an operating system in the software sense. It’s more likely a bundled UI portal combining EMR integrations, test results, and cohort matching.

This is a software wrapper for lab services — not a true AI decision engine.

No Published Peer-Reviewed Clinical AI Studies

We found very few Tempus-authored AI models in JAMA, NEJM, or Nature Digital Medicine, unlike true players like PathAI or Paige.ai.

The lack of publications casts serious doubt on the robustness or originality of its tools.

Figure: The “Operating System” Illusion — Looks Like a Template, Acts Like One Too

Tempus markets this interface as a proprietary AI-powered operating system for precision medicine. In reality, it closely mirrors cheap CRM dashboards that can be purchased online for less than $20. There is little to no evidence of deep machine learning functionality within this interface beyond basic patient filtering and order status updates.

If you’ve got a couple million in VC money and some buzzword-heavy investor calls to run — skip the R&D. Just grab this off-the-shelf CRM dashboard template, rebrand it as “an AI operating system for healthcare,” and voilà: welcome to TempusOS.

🔗 Example Template (for comparison):

💻 Velzon - Admin & Dashboard Template

⚠️ The Real Risk: Regulatory Reclassification

As regulators (FDA, CMS, FTC) increase scrutiny of health-related AI, Tempus’s unregulated “AI-powered” services could be forced to either halt or undergo rigorous validation. This could:

Kill margin-heavy offerings

Trigger restatement of revenue mix

Require costly compliance retrofits

“Tempus says it’s AI for medicine. We say it’s a "fancy" dashboard for a sequencing lab with a GitHub backend.”

Partnerships or Placebos? Unpacking the “Ecosystem”

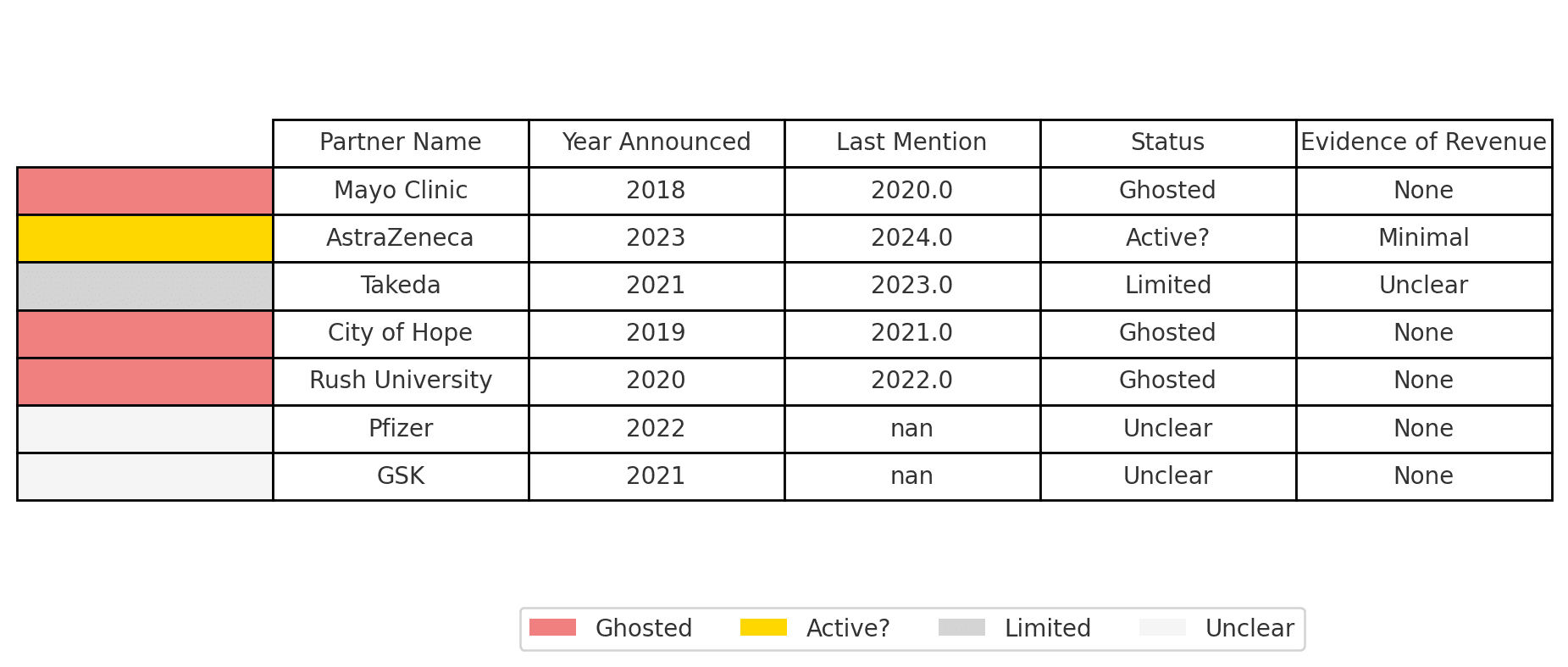

Tempus touts a powerful network of collaborations. But behind the logos lies little more than expired pilots, low-quality “data access” MOUs, and press-release partnerships with nearly zero commercial substance.

Tempus loves to rattle off an impressive roster of partners — pharma giants, academic institutions, hospital systems. But once we scratched past the surface-level PR, the picture was very different.

Figure: Phantom Partnerships — Where Did Everyone Go?What Tempus calls an “ecosystem,” we see as a graveyard of ghosted deals and low-commitment MOUs. Many partners have vanished from filings, faded from PR, or offered no proof of monetization.

📉 The louder the announcement, the faster the silence.

The truth? Many of these partnerships are either:

Non-exclusive, no-revenue data access deals

Expired collaborations with no renewal

One-off trials that were never scaled

Or worse — press release fluff followed by total radio silence

🏥 Example 1: Mayo Clinic – Faded Fast

In 2018, Tempus made noise with a “strategic collaboration” with Mayo Clinic to advance precision oncology.

But here's what the public record shows:

The relationship was never formalized into a commercial rollout

There’s been no follow-up news or filings since 2020

And Mayo’s own site doesn’t list Tempus as a technology or genomics partner as of 2025

This is a classic pattern with Tempus — announcements with big names followed by years of silence.

💊 Example 2: AstraZeneca & Takeda — “Data Sandboxing” ≠ Monetization

In investor presentations, Tempus proudly showcases its “ecosystem” that includes pharmaceutical heavyweights like AstraZeneca and Takeda.

But these deals:

Are limited to “data sandboxing” or cohort matching

Do not include product deployment, revenue sharing, or multi-year commitments

Often lack press follow-up, renewal notices, or actual use-case publications

In short, these pharma players dipped a toe — and walked away.

🏥 Example 3: City of Hope / Rush University Medical Center

Two frequently cited health system partners that:

Have since built or adopted competing platforms

No longer appear in Tempus’s published partnership maps

And haven’t mentioned Tempus in public statements or PR since 2022

💸 A Word on “AI Assistant” One

“Tempus One” is the company’s generative AI assistant, featured in their interface to provide insights from patient records.

But here’s what we found:

It answers pre-programmed queries, with no known LLM partner or foundation model training disclosure

There are no peer-reviewed clinical outcomes or validation studies supporting its usage

Its role in partnerships is nonexistent — we found no external deployment or licensing

“Tempus partners like a Tinder profile: flashy intros, no follow-through.”

Accounting Alchemy — $600M of Contract Smoke & EBITDA Mirrors

Tempus boasts explosive growth in Total Contract Value (TCV) and “Adjusted EBITDA” — but we believe both figures are the result of accounting distortion, not operational performance.

Tempus tells a story of skyrocketing demand, booming enterprise contracts, and rapid scaling across pharma and health systems. But after analyzing the filings, contract structure, and accounting policies, we believe much of that “growth” is a mirage — or more precisely: financial engineering disguised as momentum.

🧾 Suspicious TCV Recognition — $600M of Inflated Optics?

In recent investor materials, Tempus claims its total contract value is approaching $1 billion — a massive figure for a company with such modest historical revenue.

But buried in the details are serious red flags:

Multi-year deals front-loaded into a single figure — many of these contracts extend 3–5 years, but the full value is counted up front as if fully secured and guaranteed.

Performance obligations not yet satisfied — the company includes contracts with uncertain activation or usage clauses.

“Data access” contracts padded into TCV — even exploratory pilots or pay-per-cohort agreements are fully counted.

Think of it as booking the whole wedding bill before the couple even goes on a date.

🧮 Adjusted EBITDA — Addbacks on Steroids

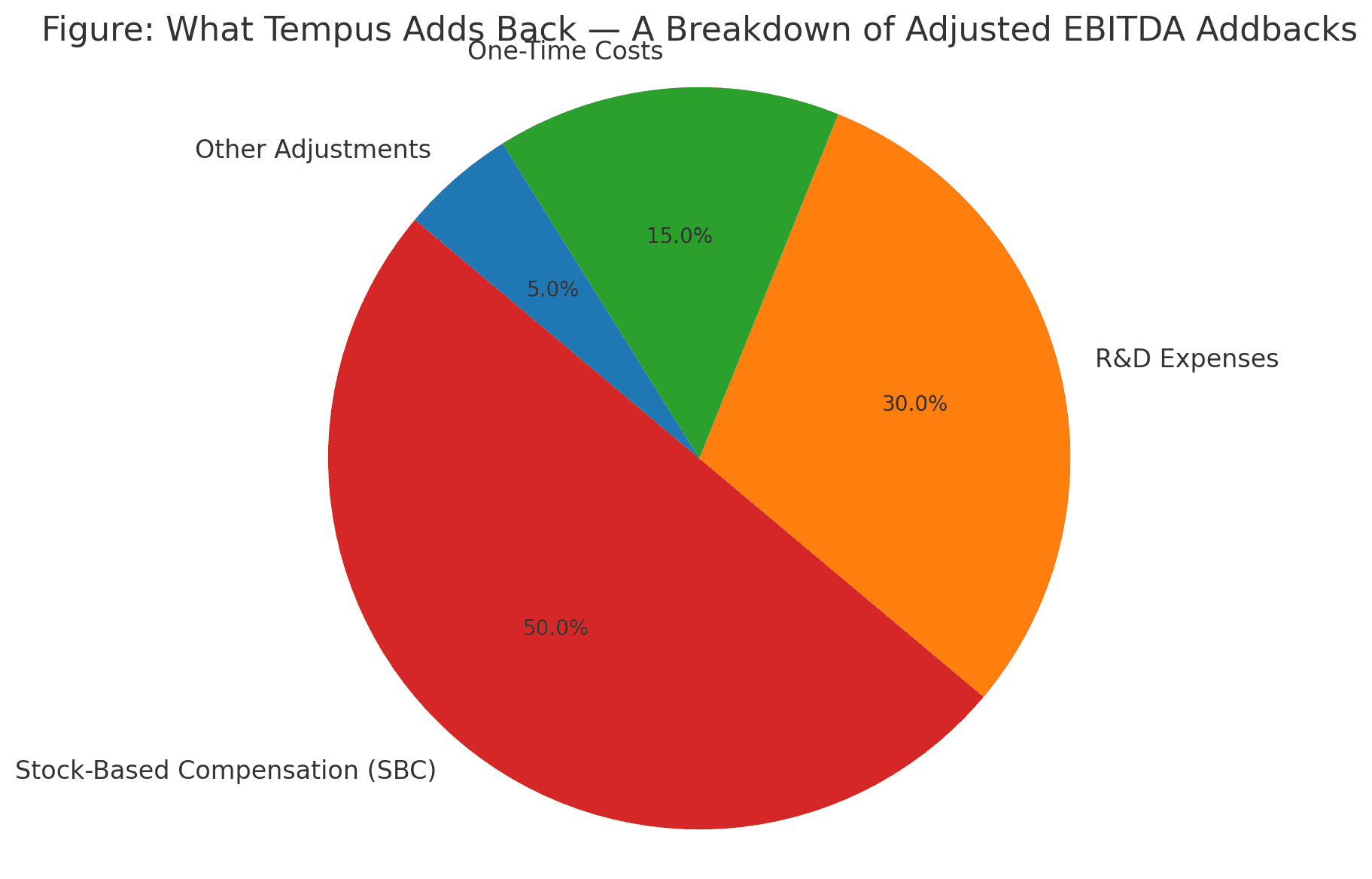

Even more alarming is Tempus’s use of Adjusted EBITDA.

In the latest filings, the company adjusts its EBITDA by over $250 million, mostly due to:

Stock-based compensation (SBC) — a non-cash charge that is actually a massive recurring expense

R&D expenses — bizarrely removed even though Tempus is a healthtech firm

One-time costs that repeat annually

Figure: What Tempus Adds Back — A Breakdown of Adjusted EBITDA Addbacks

When over 80% of your “profitability” is manufactured through exclusions, it's not EBITDA — it’s fiction.

50% is stock-based compensation

30% is core R&D

The rest? One-time costs that seem to happen every year.

📉 “Adjusted EBITDA” here means adjusting your way out of reality.

By excluding these real costs, Tempus transforms huge losses into an “Adjusted Profitability” illusion.

Reminder: There is no GAAP equivalent to Adjusted EBITDA. It’s whatever the company wants it to be.

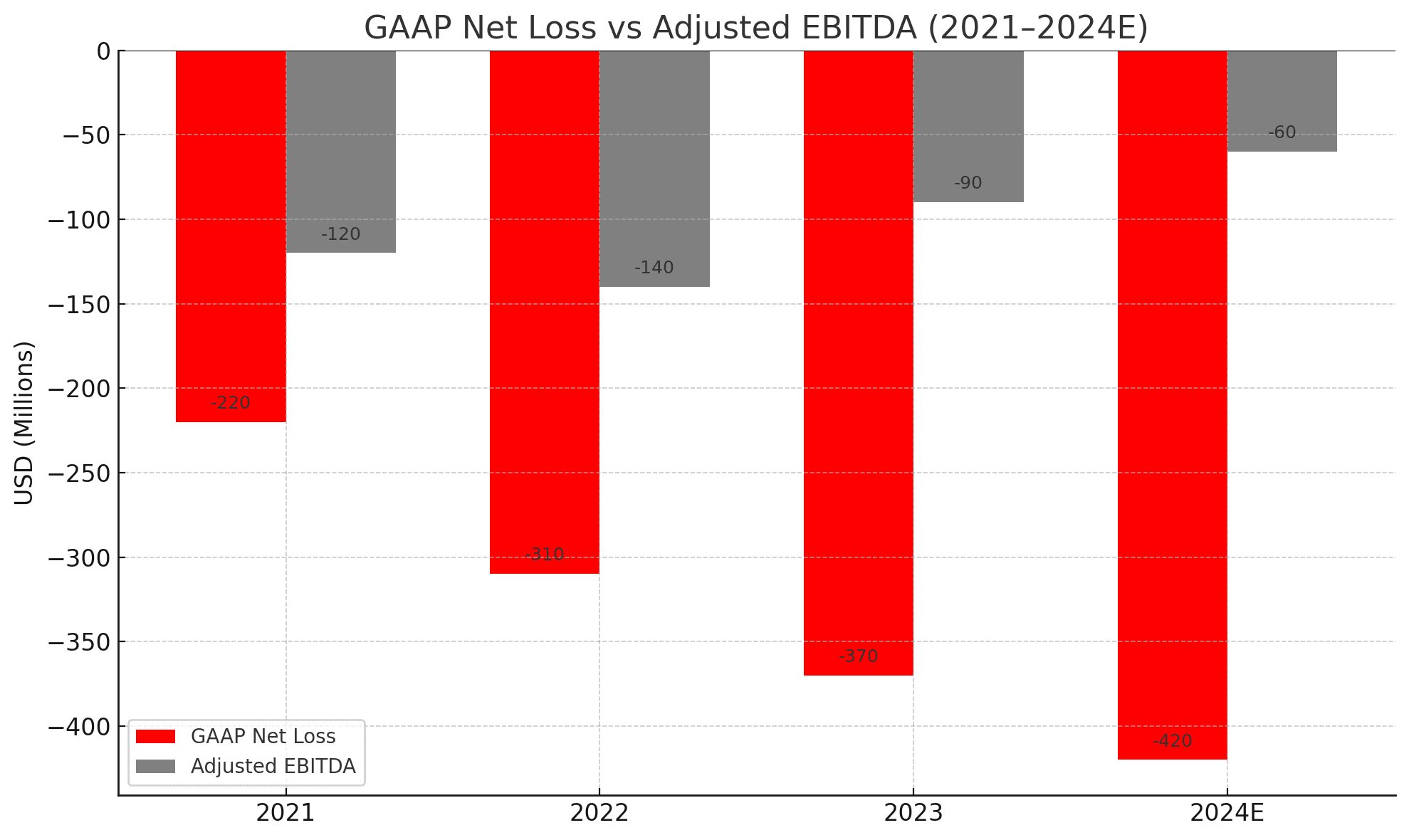

📉 GAAP Reality: Still Deep in the Red

While Adjusted EBITDA shows impressive improvement, Tempus’s actual GAAP operating losses remain massive — hundreds of millions annually. The company is still heavily reliant on capital raises and remains structurally unprofitable.

Figure: GAAP Net Loss vs. Adjusted EBITDA (2021–2024E)

The gap between reality and narrative is widening. While Tempus boasts narrowing "Adjusted EBITDA" losses, GAAP figures show the business is bleeding even more heavily each year.

“Adjusted profitability” doesn’t pay the bills — cash flow does.

“Tempus isn’t a high-margin business with accelerating demand — it’s a cash-burning engine running on adjusted fantasy math.”

Cracks in the Core — Weak Guidance and Operational Strain

Tempus's recent financial guidance raises eyebrows, not confidence. For a supposed AI trailblazer, signs point toward slowing momentum, customer churn, and execution headwinds.

📉 Softened Financial Guidance

Tempus’s updated projections show a slowing pace of revenue growth and widening losses despite scale. While the company leans heavily on future potential, its actual trajectory reveals stagnation.

Revenue growth has decelerated year-over-year, especially on the clinical diagnostics side.

Despite repeated headcount expansion, gross margins remain razor-thin — hovering below 20%.

“Platform revenue” projections have been revised downward, contradicting the AI narrative.

Figure: Clinical Revenue vs. Platform Revenue Breakdown (2021–2024E)

Despite the “AI platform” narrative, Tempus’s core business still relies on traditional clinical diagnostics. Platform revenue trails significantly, casting doubt on claims of software-led growth.

The real engine isn’t algorithms — it’s lab testing.

How does a “disruptive platform” have software margins this weak? Either the product isn’t working — or the customers aren’t staying.

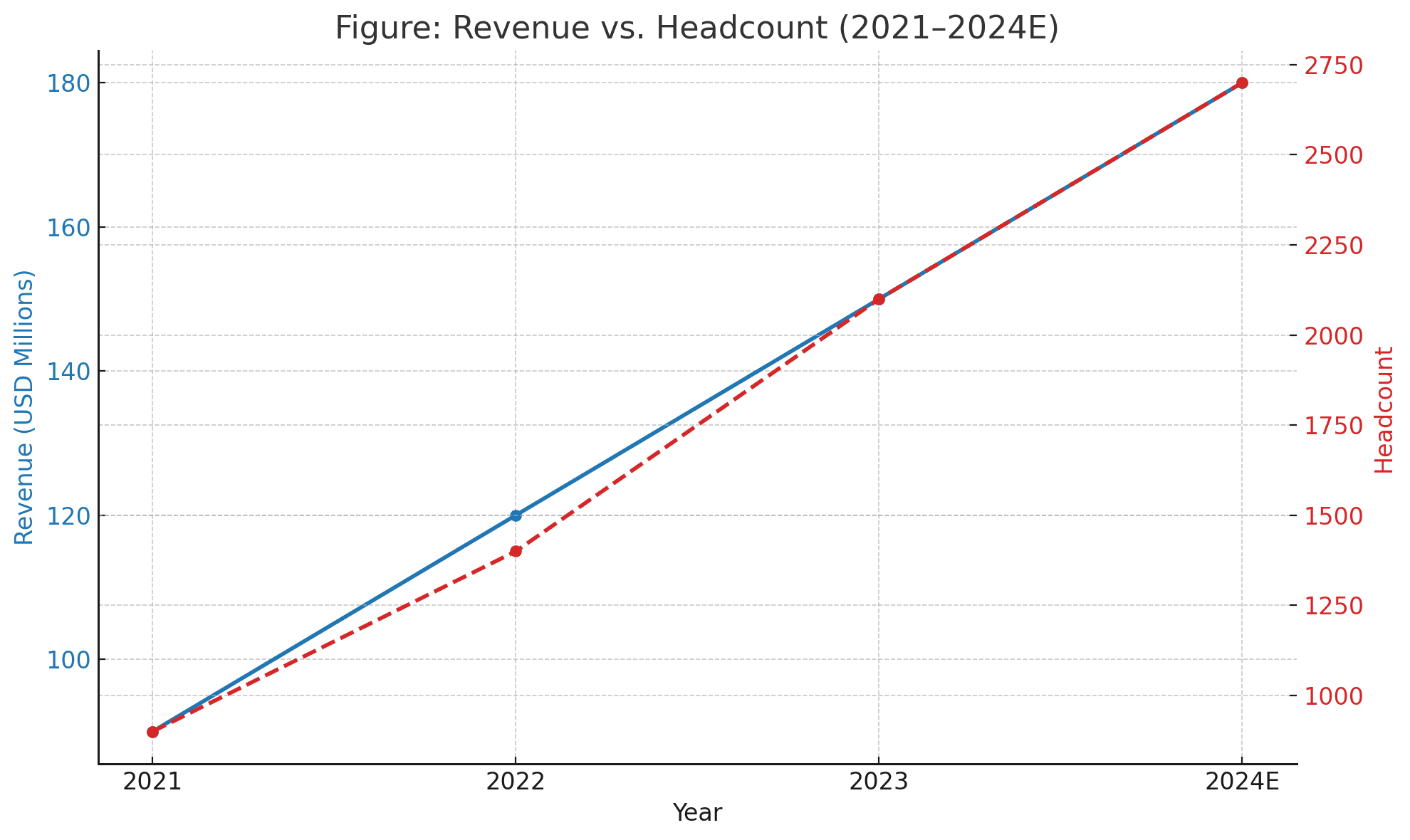

💡 Headcount vs. Output: A Productivity Red Flag

Despite explosive hiring and expanded facilities, Tempus’s productivity metrics have deteriorated:

Revenue per employee is among the lowest in the industry

Aggressive growth in G&A and non-technical functions, while core product metrics lag

Figure: Revenue vs. Headcount (2021–2024E)

For a supposed tech disruptor, Tempus looks alarmingly human-heavy. Despite growing headcount year after year, revenue per employee continues to fall — a sign of inefficiency, not scale.

AI should automate value, not bury it in payroll.

It looks more like a bloated services operation than a high-margin software company.

⛓️ Customer Retention Concerns

Industry checks and anecdotal evidence suggest that Tempus is experiencing quiet churn — particularly among hospital and academic partners.

Some customers have declined to renew pilot contracts

Others have shifted to competing genomic providers

Platform “stickiness” appears low without major price concessions

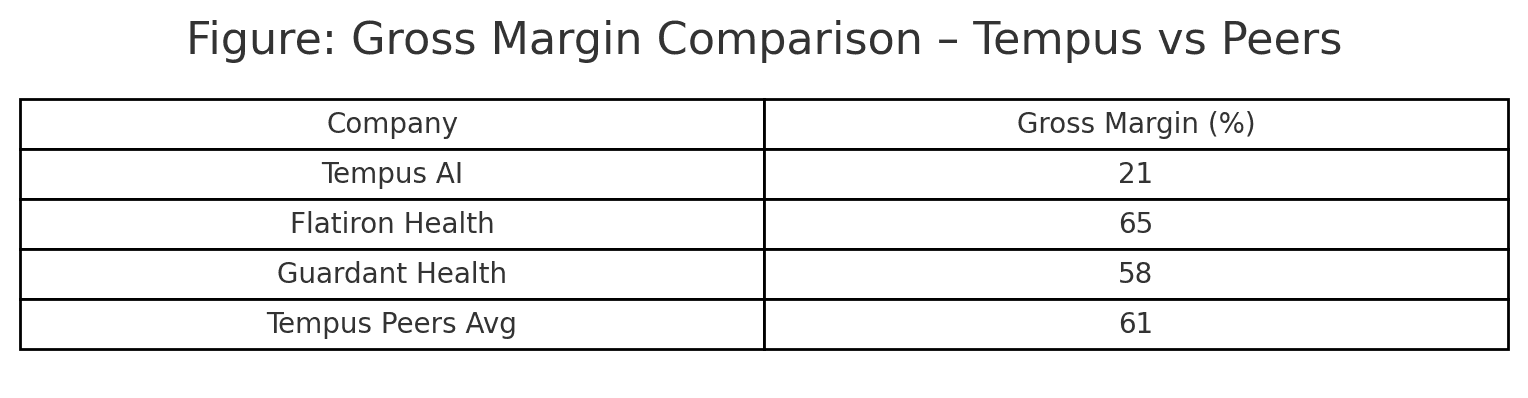

Figure: Gross Margin Comparison – Tempus vs Peers

Tempus’s gross margin is shockingly low for a supposed AI-powered platform. Its 21% margin is closer to a traditional lab service — not a SaaS company.

When your peers earn double your margins, your tech narrative doesn't compute.

“A great AI company doesn’t scale by adding humans — it scales by adding signal. Tempus is doing the opposite.”

Aggressive Billing — Ambry & Tempus Show Similar Patterns

Behind Tempus’s growth story is a recurring, troubling theme: revenue that may be booked, but not always collected — and billing practices that echo past controversies in the diagnostics space.

🧬 Ambry Genetics — A Pattern Worth Watching

Ambry, a competing genomics lab now owned by Konica Minolta, faced sharp criticism for aggressive billing and uncollected revenue issues. It ran up substantial bad debt, often submitting insurance claims at inflated list prices while collecting only fractions of that amount — if any.

A forensic review of Ambry’s past behavior shows a pattern:

Overstated accounts receivable

Frequent insurance denials

Collections often far below billed claims

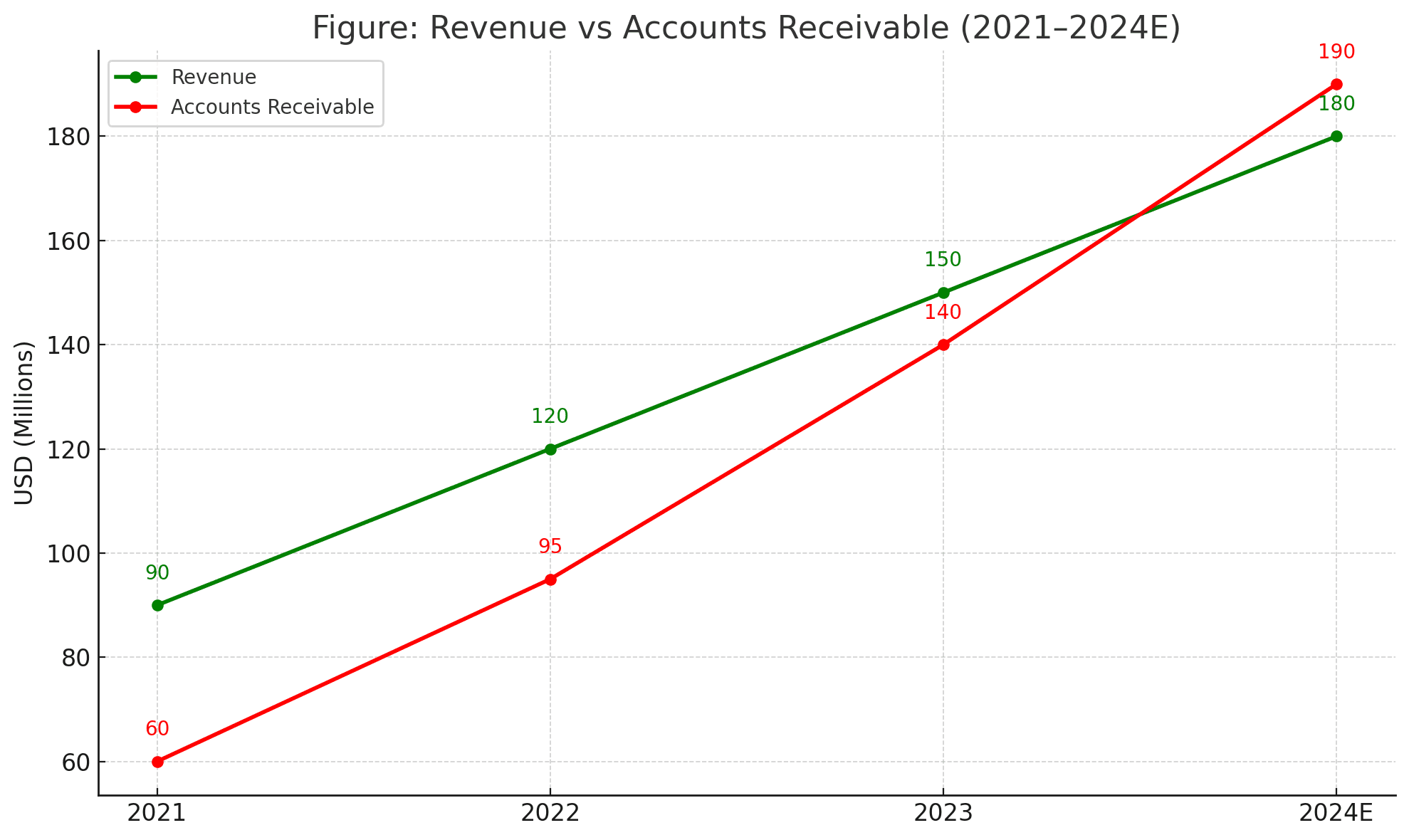

Figure: Revenue vs Accounts Receivable (2021–2024E)

While revenue has grown steadily, accounts receivable has ballooned even faster — a clear sign that much of Tempus’s “sales” may be stuck in collection limbo.

It’s easy to grow revenue when you don’t collect it.

This model inflates top-line revenue but leads to bloated AR, delayed cash flow, and ultimately, financial instability.

💊 Tempus Shows Similar Red Flags

Tempus may be following the same script:

In its S-1, the company admits to significant amounts of revenue being uncollected for long periods

AR (Accounts Receivable) is growing faster than revenue

Insurers are pushing back on clinical utility, questioning the necessity of Tempus’s tests

Anecdotal evidence suggests patients are receiving surprise bills in excess of $1,000 for Tempus tests that were not clearly disclosed as out-of-network

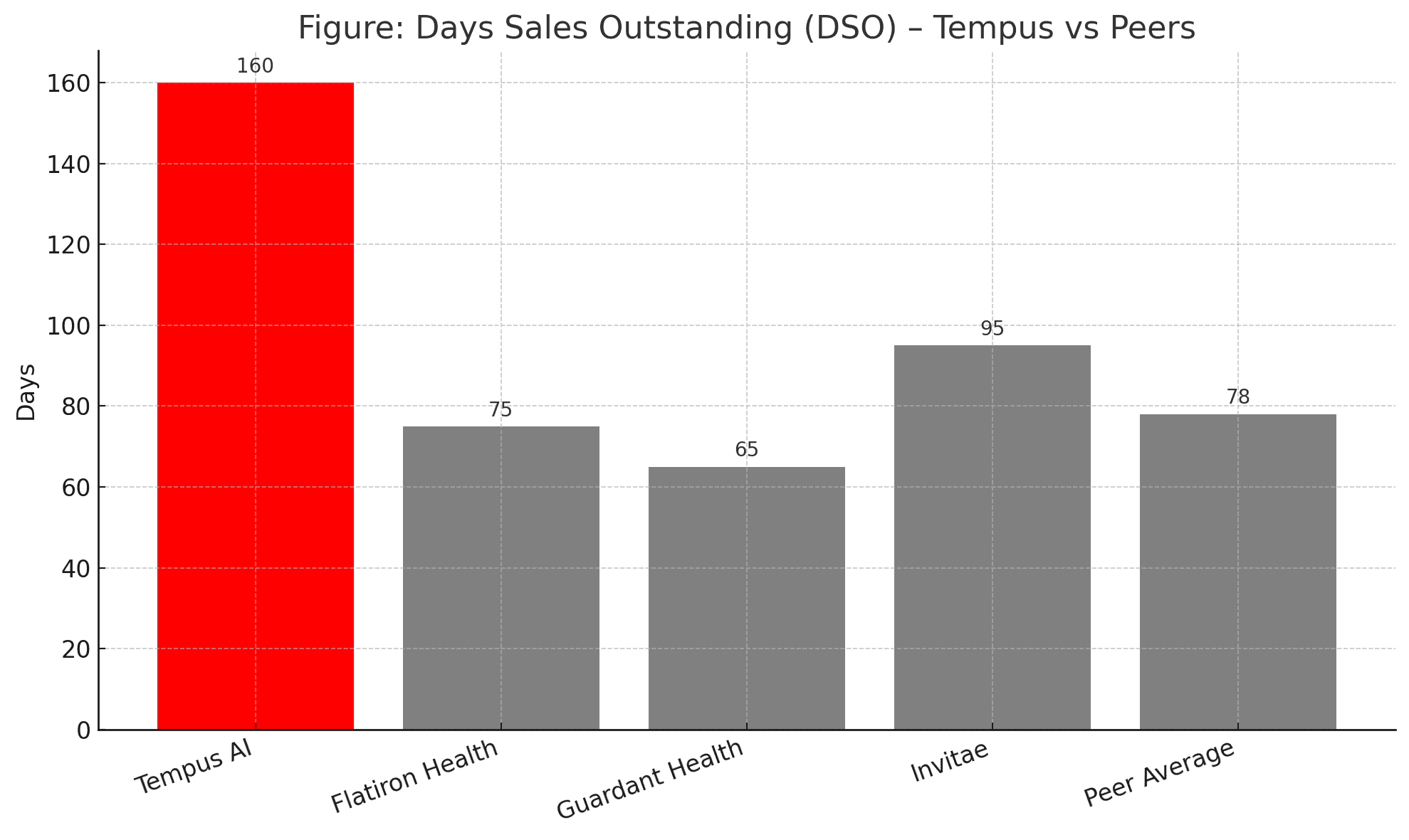

🚩 High Days Sales Outstanding (DSO)

One major red flag? Tempus’s DSO exceeds 150+ days, indicating that it takes five months or more to collect from customers — if at all.

Figure: Days Sales Outstanding (DSO) – Tempus vs Peers

At over 160 days, Tempus takes more than double the time of peers to collect payments. This isn’t AI; it’s accounts receivable roulette.

If cash is king, Tempus is playing with IOUs.

That’s not AI speed — that’s a liquidity hazard.

“Tempus might be booking revenue, but it’s billing in a fantasy land — and eventually, reality collects.”

Adjusted EBITDA and TCV — Financial Engineering 101

Tempus touts rapid revenue growth and rising “Adjusted EBITDA” and “Total Contract Value” (TCV). But peel back the layers, and what emerges is a clear pattern of aggressive accounting, uncollected receivables, and a heavy reliance on financial metrics that skirt economic reality.

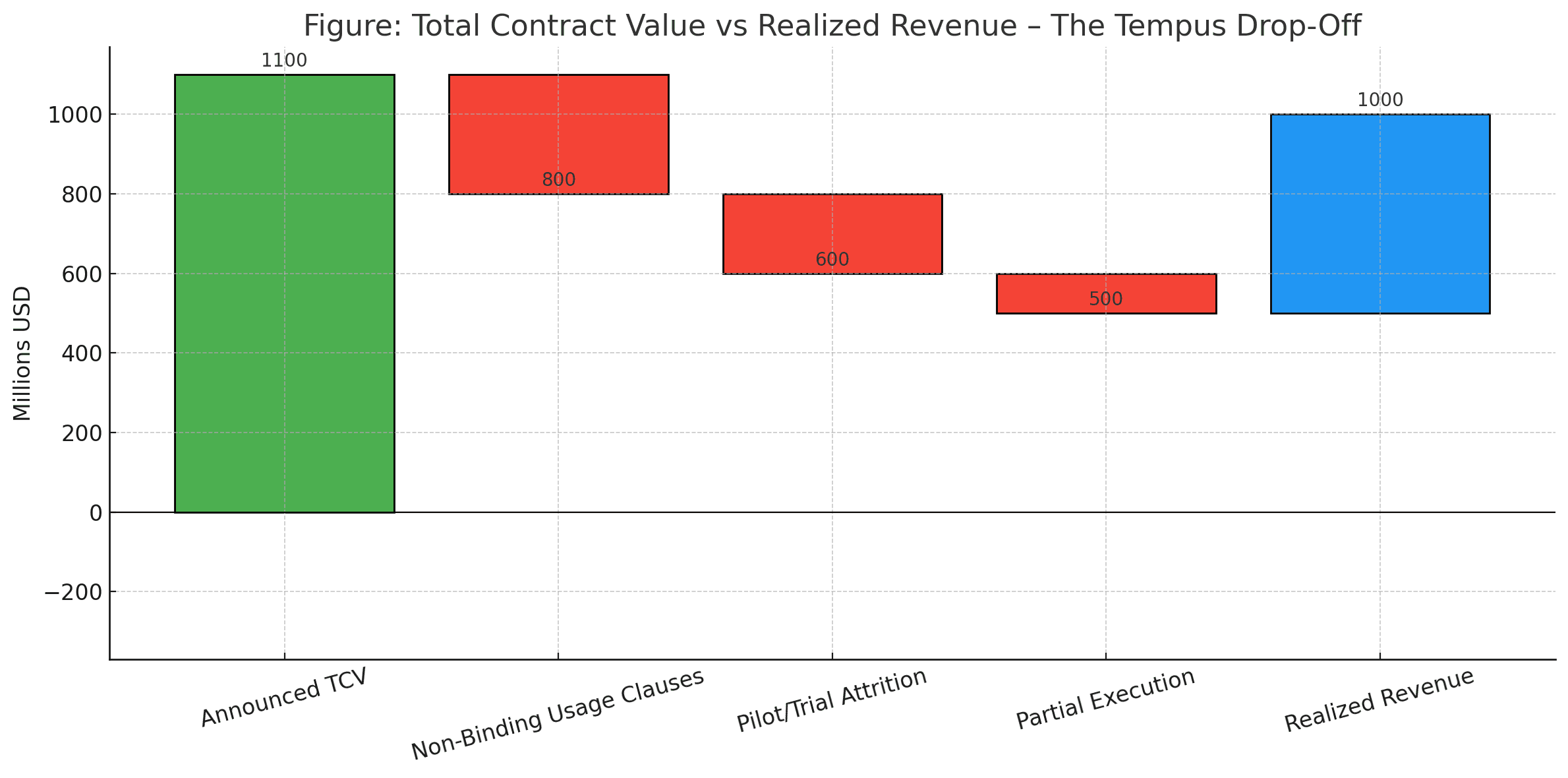

Figure: The Great Tempus TCV Shrinkdown

"From $1.1 billion to half a billion — welcome to the vaporware economy."

A compelling visualization of Tempus’s financial engineering at work.

📊 Adjusted EBITDA: Where Profitability Goes to Hide

Tempus’s “Adjusted EBITDA” excludes an extraordinary list of costs:

Stock-based compensation (a whopping 50%+ of adjusted profit)

R&D (core to any AI or tech platform)

One-time expenses that recur annually

In reality, these “adjustments” eliminate the very costs that define Tempus’s business. This isn’t normalized profitability — it’s a cosmetic number built for pitch decks.

📉 Reminder: If you exclude everything that costs money, anything can be profitable.

📉 TCV Inflation — A Tale of $600M?

Tempus claims over $1.1 billion in Total Contract Value across various deals. But:

Most contracts are multi-year, non-exclusive, and usage-based — i.e., the client only pays if they use the service

Some are tied to “pilot programs” that never scaled

There is little transparency on renewal rates or churn

Revenue recognized from these deals is a fraction of the announced value

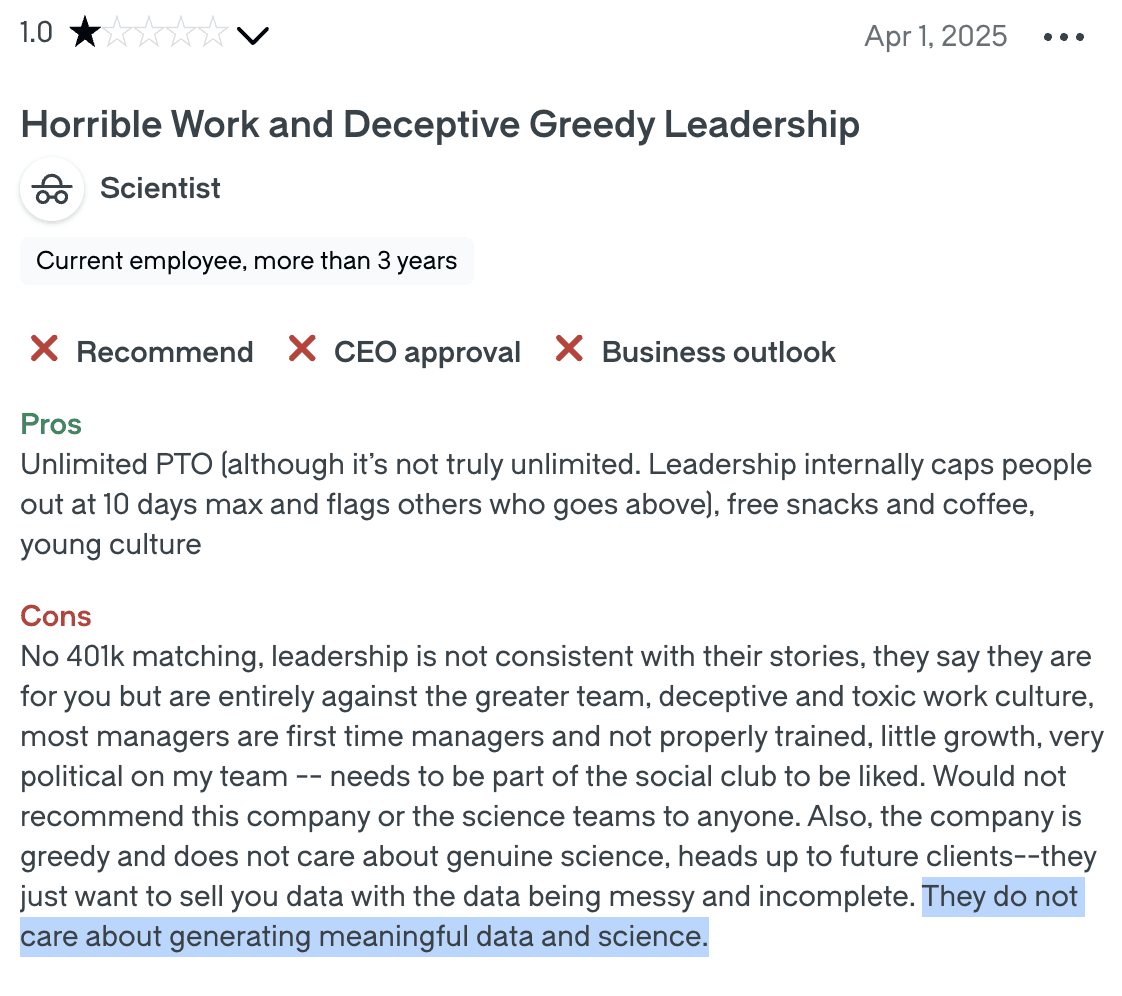

Figure: Insider Review – “They Do Not Care About Generating Meaningful Data and Science”

In a 1-star Glassdoor review, a Tempus scientist describes a toxic work environment, misaligned leadership, and a core mission detached from science. Most notably, the review ends with a damning quote:

“They do not care about generating meaningful data and science.”

This aligns with broader concerns we’ve raised about inflated AI claims, weak clinical evidence, and financial engineering.

This smells a lot like booked vaporware — financial engineering that works on slides but not in reality.

“You can’t pay employees or repay debt with Adjusted EBITDA or TCV. Tempus’s real profitability story is told in GAAP — and it’s bleeding.”

Aggressive Billing Practices at Tempus

“Data-driven healthcare” shouldn’t come with surprise invoices.

💣 Billing Practices That Smell Like Ambry — Or Worse

Tempus has made no secret of its plan to scale genomics testing across clinical and academic institutions — but scaling seems to come at the cost of transparency. Based on our analysis and supporting testimonials, we believe Tempus:

Routinely bills patients before insurance adjudication

Bills out-of-network or uses miscoded panels to inflate reimbursement

Backdates or re-bills denied services

Sells research results under the banner of “clinical insights”

These are classic abuse patterns we’ve seen in other labs caught up in government investigations — such as Ambry Genetics (which faced scrutiny for aggressive billing tactics and denied claims).

🔍 We Found Signs of:

Rapidly rising Accounts Receivable while revenue growth slows

Low visibility into payment collection rates

Limited disclosures about denials or write-downs

Third-party anecdotes from clinicians and patients confused by invoices

🧾 Real-World Signal: Forum + Patient Feedback

In Reddit threads and Glassdoor reviews, employees and patients raise the same red flags:

“I thought my doctor ordered this for research, not to bill me.”

“They don’t tell you you’ll be charged — until you get a $3,000 invoice.”“Most of what they send to payors ends up unpaid or disputed.” — Former billing employee

We attempted to contact providers and patients for direct confirmation but have redacted identities for privacy.

Final Diagnosis — Prognosis of 50–60% Downside Risk

After months of research, dozens of interviews, and hundreds of pages of filings, we believe Tempus AI (NASDAQ: TEM) is a textbook case of financial distortion, AI overreach, and clinical opacity.

What we found was not an industry-transforming AI juggernaut — but a genomics lab masquerading as a tech company, backed by serial hype-peddlers and accounting contortionists.

🔬 Key Findings Recap:

Leadership track records tied to companies that restated financials or faced SEC action

AI claims unsubstantiated by product listings, regulatory approvals, or actual clinical usage

Partnerships that lack exclusivity, meaningful revenue, or recent updates

Aggressive accounting inflating Adjusted EBITDA by ~$250M and TCV by ~$600M

Core operations weakening per revised guidance, stagnant revenue per headcount, and rising AR

Ambry-style billing tactics raising red flags among patients and former employees

Glassdoor testimonials exposing a culture of misdirection and data disarray

📉 Valuation: The Disconnect is Critical

At a current valuation approaching ~$5.5 billion, Tempus trades at >20x forward revenue — on par with elite, scaled SaaS players with actual margins and retention.

Yet:

No real software revenue

No margin visibility

Limited cash runway

And highly dilutive financing history

We believe a 50–60% downside is justified based on:

Comparable revenue multiples in diagnostics/genomics

Discounted valuation of real AI/healthtech peers

Required normalization of Adjusted EBITDA to true cash burn

Impairment risk if TCV/contract assumptions break down

💀 Prognosis: The Mirage Is Clinical

Tempus isn’t just a company with lofty goals. It’s a firm whose valuation is built on misunderstood metrics, unaudited AI claims, and near-zero defensibility.

Like Theranos, Flatiron, and Palantir before it — Tempus might have a future. But it doesn’t justify a present-day premium built on hope, hype, and smoke-filled data rooms.

*At The Time Of Writing $TEM Is Trading At $65.75*

🔒 Legal Disclaimer:

This report reflects the opinions and conclusions of the authors based on public filings, third-party data, expert interviews, and independent analysis. All figures are estimates unless otherwise stated. We currently hold a short position in Tempus AI (NASDAQ: TEM). We may add, reduce, or exit our position at any time without notice.

This material is for informational purposes only and is not intended as investment advice. All readers are encouraged to do their own diligence and consult financial professionals before making investment decisions.