BMF Reports has initiated a short position in Anavex Life Sciences (NASDAQ: AVXL), citing an imminent EMA rejection, manipulated trial endpoints, and serial dilution via Lincoln Park and ATM financings.

Anavex Life Sciences (NASDAQ: AVXL) has built one of the most misleading narratives currently trading on a U.S. exchange. Behind the biotech buzzwords and press release jargon lies a house of cards—propped up by manipulated trial endpoints, statistical gymnastics, shady insider compensation structures, and a CEO with a pattern of red flags spanning decades.

Since going public, Anavex has pivoted from one marketing campaign to the next, relentlessly spinning weak or failed clinical trial data into headline-friendly fluff to bait retail interest and keep the ATM machinery running. Its lead drug candidate, blarcamesine (ANAVEX-2-73), has been heralded as a potential treatment for everything from Alzheimer’s to Rett syndrome to Parkinson’s—despite no consistent, reproducible efficacy in any of them.

Worse, we’ve uncovered a pattern of behavior that should concern any institutional investor, regulator, or journalist paying attention. This is not the story of a misunderstood innovator. It’s a forensic case study in biotech misdirection. And with an imminent EMA verdict likely to reject their lead program, the clock is ticking.

Let’s be clear: this isn’t just another small-cap biotech clinging to hope. This is a calculated operation built on statistical misdirection, insider enrichment, and corporate obfuscation. We believe the upcoming EMA decision — will be the final nail in the coffin.

The 60–80% price collapse hasn’t happened yet. But the trapdoor is already open. And we’re about to show you exactly why.

Key Points:

Rigged Clinical Trials: Anavex changed its trial endpoints midstream — after receiving FDA feedback — to game statistical significance. Their “composite” endpoints are scientifically meaningless and regulatory deadweight.

EMA Rejection Incoming: Based on EMA guidance documents, historical precedent, and statistical review, Anavex’s application for blarcamesine is structurally non-approvable in its current form.

Insider Enrichment Scheme: CEO Christopher Missling and a revolving door of complicit board members have extracted over $45M in combined comp, options, and related-party benefits while the company diluted retail shareholders into oblivion.

Litigation Footprint Growing: Anavex is now facing multiple shareholder derivative suits, including Deangelis v. Anavex (D. Nev. 2:24-cv-00891), alleging breach of fiduciary duty, unjust enrichment, and false proxy statements under §14(a). These are not baseless — they cite specific FDA communications, false disclosures, and pattern fraud.

Zero Commercial Infrastructure: No sales team. No contracts. No payer negotiations. No hospital reps. Yet the market cap sits at nearly $750 million — as if there’s a real business here. There isn’t.

This isn’t just a short idea. It’s a forensic teardown.

Clinical Trial Fraud and Endpoint Tampering — How Anavex Rewrote the Rules Midgame

When your drug doesn’t work, there are two options: fix the science, or fix the narrative. Anavex chose the latter.

At the center of its house of cards is blarcamesine (ANAVEX-2-73) — a compound they claim shows promise across Rett syndrome, Alzheimer’s, and Parkinson’s. But a closer look at the trial design, execution, and post-hoc statistical manipulations reveals what we believe to be an egregious case of regulatory evasion by design.

The Endpoint Bait-and-Switch: A Blueprint for Misleading the Market

Let’s talk about AVATAR and EXCELLENCE, Anavex’s two Rett syndrome trials.

Initially, the company committed to using RSBQ AUC (Rett Syndrome Behavior Questionnaire Area Under the Curve) as the primary endpoint in both trials. This was their public position for years.

Then, February 2, 2023, Anavex drops a vague press release:

“Anavex received feedback from the FDA regarding endpoint metrics.”

No clarity. No specificity. Just regulatory smoke.

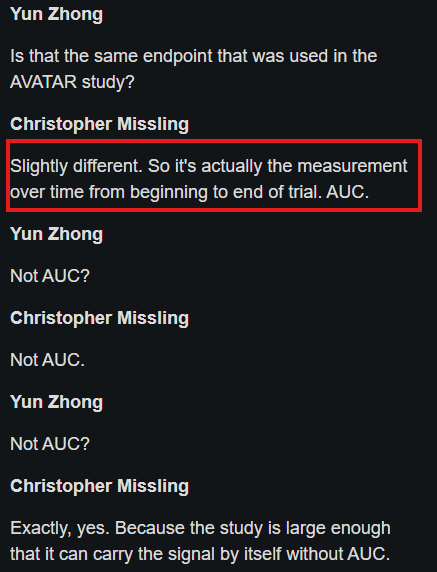

Figure: Excerpt from Anavex’s February 7, 2023 earnings call, where CEO Christopher Missling concedes the EXCELLENCE trial will use a “slightly different” endpoint than the prior AVATAR study — quietly confirming a shift in measurement methodology mid-program. HERE

Five days later, on February 7, CEO Christopher Missling quietly admits the company will now be using a “slightly different” endpoint in the EXCELLENCE trial — a barely noticeable but critically important shift.

What really happened?

According to the shareholder derivative lawsuit Blum v. Anavex, internal communications and court findings confirm that:

The FDA told Anavex flat-out that RSBQ AUC would not be accepted.

Anavex failed to disclose that crucial fact.

Their February 2 press release was materially misleading by omission.

The switch to a new “composite” endpoint allowed them to cherry-pick and repackage weak data.

This isn’t just questionable. It’s textbook scienter. The court agreed that there was strong circumstantial evidence of conscious misbehavior or recklessness in how Anavex misled the public about their endpoint change .

And while the plaintiff’s case was dismissed on technical “loss causation” grounds, the core fraud claims were not. Let that sink in.

A “Composite” Endpoint Nobody Asked For

To mask underwhelming efficacy, Anavex shifted to a proprietary, cherry-picked “Rett Syndrome Clinical Composite Score (RSCCS)”, created by the company itself, behind closed doors, and not validated by any regulatory agency.

This Frankenstein endpoint bundles together:

RSBQ (Behavior Questionnaire)

CGI-I (Clinical Global Impressions–Improvement)

Sleep Diary data

Caregiver assessments

They’ve never disclosed weighting methodologies, correlation matrices, or sensitivity analyses. Why? Because the math likely doesn’t hold up to scrutiny.

Even worse, the FDA’s own rare disease guidance warns against composite endpoints in underpowered studies — especially when no single measure shows clear significance. But that’s exactly what Anavex pushed forward to the EMA.

And here’s the kicker: EMA guidance explicitly favors RSBQ AUC or CGI-I as individual endpoints — not custom composites. Which brings us to…

EMA Rejection Imminent

Based on:

Anavex’s failure to use a pre-specified, validated endpoint

Lack of replicated efficacy across trials

Statistical red flags and post-hoc manipulations

…we believe the European Medicines Agency (EMA) will reject blarcamesine’s marketing application for Rett syndrome.

This would be catastrophic. Anavex has no commercial assets, no backup revenue stream, and is burning cash with no sales team or partner in place. A failed EMA verdict triggers an immediate repricing of the equity to reality.

We believe that moment is weeks away.

Alzheimer’s Trial — More of the Same

This isn’t an isolated Rett issue. Anavex’s Phase 2 Alzheimer’s trial followed the same script:

Switched from ADAS-Cog to MMSE post-hoc.

Relied on “SIGMAR1 genetic subgroup” cherry-picking to justify weak primary outcomes.

Avoided meaningful cognitive functional endpoints like CDR-SB or ADCS-ADL.

The Alzheimer’s study wasn’t powered to detect real-world efficacy — but it was perfect for spinning ambiguous data into press releases. And that’s what they did.

Bottom Line:

Anavex’s trial program is a statistical mirage.

Endpoints were manipulated after the fact.

The FDA explicitly warned them.

The EMA is about to say no.

If this drug had robust efficacy, it wouldn’t need custom endpoints and legal tap dancing. The data would speak for itself.

But it doesn’t. And we are not the only ones catching on.

The Mirage of Blarcamesine

Anavex Life Sciences (NASDAQ: AVXL) has spent nearly a decade selling one idea to investors: that its flagship molecule, blarcamesine (ANAVEX 2-73), is a potential disease-modifying therapy for Alzheimer’s and other central-nervous-system disorders. The story reads well on paper — a small-molecule “Sigma-1 receptor activator” that promises to restore cellular homeostasis, improve autophagy, and reduce neurodegeneration.

But behind the buzzwords sits a drug with no convincing proof of efficacy, endless statistical gymnastics, and a management team that’s mastered the art of looking busy while delivering nothing.

A Drug Built on Theory, Not Data

The Sigma-1 receptor angle isn’t new. It’s been kicked around academic literature for decades, with sporadic claims of neuroprotective potential — mostly in petri dishes. No drug built on this mechanism has ever reached commercial success.

Anavex capitalized on that scientific gray zone. The company repurposed a compound first synthesized in the 1990s, layered it with pseudoscientific jargon about “precision medicine” and “biomarker-guided therapy,” and convinced retail investors that it was the next Aricept.

What they really built was a narrative engine, not a drug program.

The Alzheimer’s Illusion

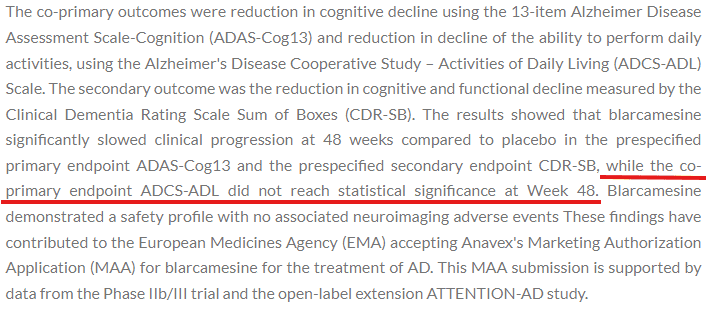

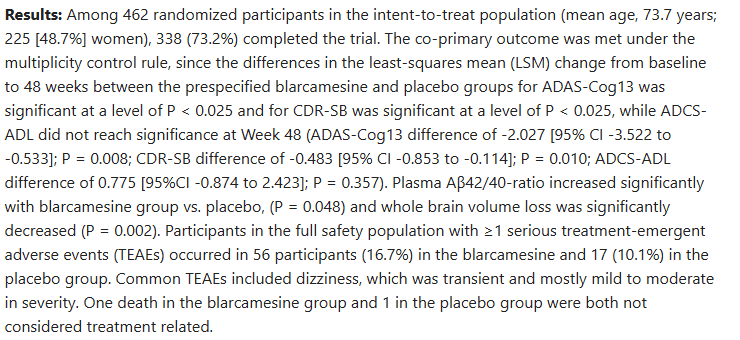

Blarcamesine’s Alzheimer’s data are weak to the point of irrelevance. In its pivotal Phase IIb/III study (ANAVEX2-73-AD-004), the drug missed its functional co-primary endpoint (ADCS-ADL) and only achieved a nominal win on the cognitive scale (ADAS-Cog13) after 48 weeks — and only by pooling 30 mg + 50 mg arms post-hoc.

Figure: Excerpt from Alzheimer Europe’s summary of Anavex’s Phase IIb/III Alzheimer’s trial, confirming that while the cognitive endpoint (ADAS-Cog13) showed nominal improvement, the co-primary functional endpoint (ADCS-ADL) failed to reach statistical significance at Week 48 — undercutting the company’s claims of meaningful efficacy.

This isn’t science. It’s data dredging. Regulators don’t reward post-hoc heroics; they punish them.

The absence of a dose–response relationship, the massive adverse-event imbalance (dizziness, confusion, discontinuations), and the high heterogeneity across sites scream poor trial design — or worse, willful spin. HERE

The “Pipeline in a Product” Myth

When the Alzheimer’s narrative started to falter, Anavex pivoted to Rett syndrome, a rare genetic disorder. The sample size was microscopic. The reported effect size (Cohen’s d ≈ 1.9) was statistically implausible — on par with morphine vs placebo. Yet management touted it as “breakthrough evidence” and recycled the claim across investor conferences.

Then came the same pattern: small study, noisy data, oversized hype, and a predictable “expansion to new indications” press cycle.

The market rewarded the noise, not the science.

Red Flags of a Promotional Culture

You can track Anavex’s priorities by its checkbook.

Over $6 million in annual executive pay.

Tens of millions spent on “investor relations” and “consultants.”

Minimal disclosure on who those consultants are or what they produce.

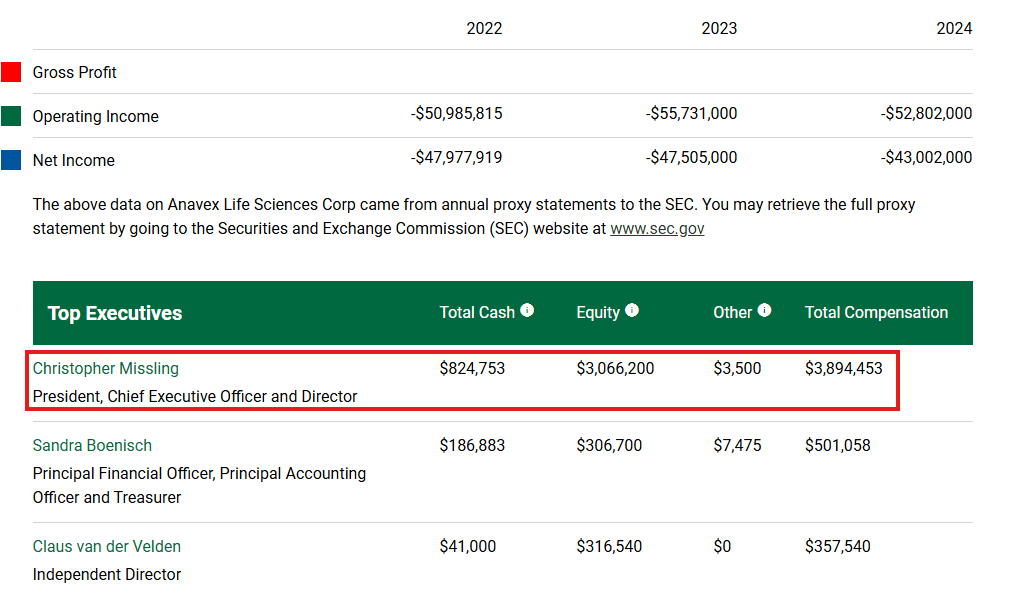

Figure: Extract from Anavex’s 2024 proxy filing showing CEO Christopher Missling’s total compensation of $3.89 million — a mix of cash and equity — despite years of unprofitable operations and ongoing shareholder dilution.

A revolving list of headquarter addresses across continents — British Columbia, Switzerland, New York, Greece — like a company playing hide-and-seek with accountability. HERE

The Setup for a Fall

Every Anavex rally follows the same script: vague clinical promises, selective endpoints, investor hype, equity issuance, dilution, repeat.

The only consistent success story here is the share price manipulation cycle.

The science isn’t moving forward — the spreadsheet is.

The Endpoint Deception

If there’s one defining moment in Anavex Life Sciences’ (NASDAQ: AVXL) collapse from “biotech innovator” to case study in manipulation, it’s this: the RSBQ AUC endpoint switch — a quiet maneuver that turned a failed clinical program into a headline illusion.

This wasn’t a clerical adjustment. It was a regulatory sleight of hand — a material change in how success was measured, concealed from investors under the guise of “FDA input.”

The court record confirms it.

What Happened

Between 2017 and 2024, Anavex conducted two clinical trials for its Rett syndrome program:

AVATAR (Phase 2) – used an endpoint metric called RSBQ AUC (Rett Syndrome Behavior Questionnaire – Area Under the Curve).

EXCELLENCE (Phase 3) – publicly stated it would use the same endpoint metric to maintain consistency.

Then came February 2, 2023.

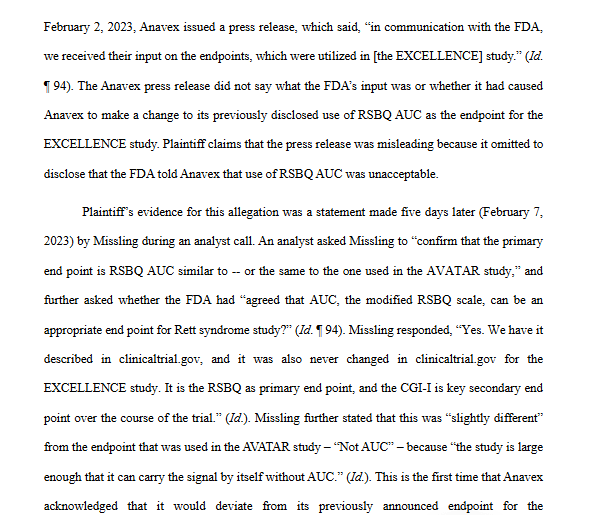

Anavex issued a press release saying it had “received input from the FDA” regarding endpoints — without disclosing what that input was.

Figure: Excerpt from the Court’s decision in Blum v. Anavex Life Sciences Corp. showing the Feb 2, 2023 Anavex press release line: “In communication with the FDA, we received their input on the endpoints, which were utilized in [the EXCELLENCE] study.” — the omission of key details about FDA rejection is described as “materially false and misleading.” HERE

Five days later, on February 7, CEO Christopher Missling admitted the company would be using a “slightly different metric” for EXCELLENCE.

Translation: the FDA rejected their chosen endpoint.

They didn’t tell investors. They rebranded the failure as progress.

Why It Matters

Endpoints are the entire premise of a clinical trial.

Change the endpoint, and you change the definition of success.

When the FDA says “no” to an endpoint, it means the agency doesn’t view the metric as capable of demonstrating clinical benefit.

By continuing to tout “positive results” from AVATAR while concealing that the same metric was now deemed unacceptable, Anavex crossed the line from optimism to misrepresentation.

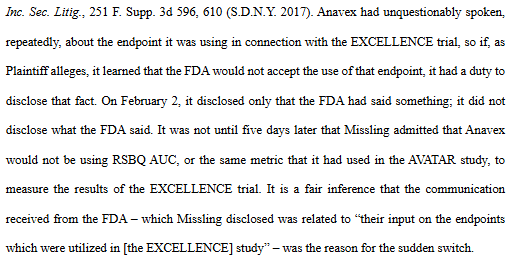

As Judge McMahon put it in Blum v. Anavex Life Sciences Corp. (S.D.N.Y. 1:24-cv-01910):

“Once Anavex had spoken about the endpoint to be used in EXCELLENCE, it had a duty to disclose that the FDA would not accept the use of the planned endpoint.”

That single sentence is the legal equivalent of a loaded gun. It establishes duty to disclose and scienter — the intent to deceive.

The Court’s Findings

The court dissected the February 2023 disclosure timeline in surgical detail:

The February 2 press release was misleading — it omitted that the FDA had explicitly told Anavex that the RSBQ AUC was unacceptable.

The February 7 statement was deemed curative, since Missling finally admitted the endpoint was being changed.

The complaint sufficiently alleged scienter, meaning Anavex acted with intent or reckless disregard for the truth.

The only reason the securities claim failed was loss causation — the stock went up that day (6%), not down, giving Anavex a procedural escape hatch.

Figure: Excerpt from Blum v. Anavex Life Sciences Corp. (S.D.N.Y. 1:24-cv-01910) where Judge McMahon explicitly states that once Anavex had spoken about the EXCELLENCE trial’s endpoint, it had a duty to disclose that the FDA rejected the metric. The passage confirms the company learned its RSBQ AUC endpoint was unacceptable and concealed that fact from investors—legally establishing duty to disclose and scienter. HERE

In short: they didn’t win because they were innocent; they won because the stock rallied before the market realized what had happened.

The judge explicitly noted:

“The allegation that Anavex learned information from the FDA that contradicted previous statements presented strong circumstantial evidence of conscious misbehavior or recklessness.”

That’s judicial code for: They knew what they were doing.

The Pattern of Spin

This wasn’t an isolated incident — it was a continuation of a pattern.

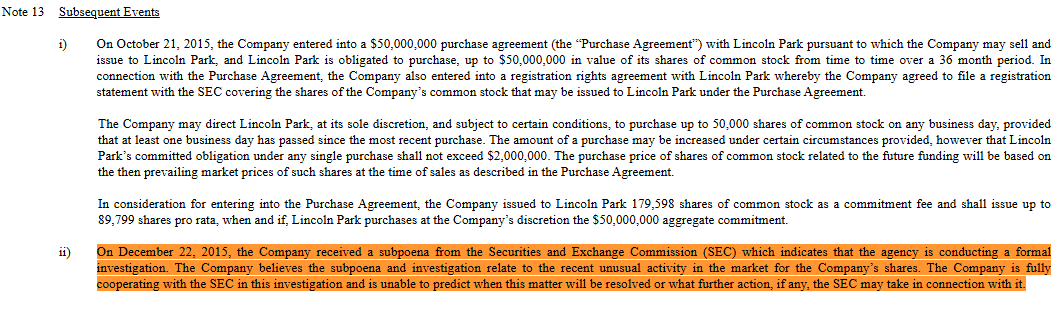

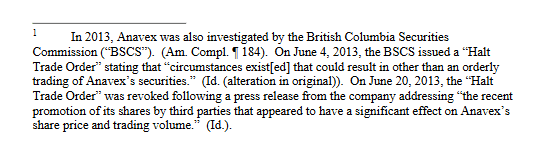

Years earlier, Anavex faced similar allegations of promotional misconduct, paid IR campaigns, and regulatory investigations (SEC in 2015, BCSC in 2013).

Figure: Extract from Anavex Life Sciences Corp.’s 2015 Form 10-K filing, disclosing that the company received a formal subpoena from the U.S. Securities and Exchange Commission (SEC) regarding “unusual activity in the market” for its shares. The filing confirms a federal investigation into potential trading irregularities and promotional conduct surrounding Anavex’s stock. HERE

The Blum ruling effectively bridged that history to the present day, acknowledging that Anavex’s “promotional culture” and selective disclosure pattern still define its corporate behavior.

The court recited seven factual pillars behind that pattern:

Missling’s involvement in multiple promotional interviews.

Denial of paid IR campaigns despite documentation.

Chronic dependency on equity-financing tied to share price.

Millions spent on “consultant” and “investor relations” expenses.

Sudden cessation of those line items once scrutiny rose.

Historical stock promotion cases (dating back to 2007).

Ongoing regulatory scrutiny from both U.S. and Canadian agencies.

Figure: Excerpt from court filings describing the 2013 British Columbia Securities Commission (BCSC) investigation into Anavex. The BCSC issued a “Halt Trade Order” citing “circumstances that could result in other than an orderly trading” of Anavex’s securities. The halt was lifted only after the company acknowledged “recent promotion of its shares by third parties” that had significantly impacted its share price and trading volume.

Even though those didn’t meet the Tellabs scienter threshold for a full securities conviction, they painted a damning picture of intent — a company that markets itself first and manufactures science later.

What the Derivative Case Adds

The Deangelis v. Anavex Life Sciences Corp. (D. Nev. 2:24-cv-00891) case is the corporate mirror image of Blum — shareholders suing on behalf of the company itself for insider misconduct.

The claims read like a governance autopsy:

Breach of fiduciary duty

Unjust enrichment

Waste of corporate assets

Gross mismanagement

Abuse of control

Exchange Act §14(a) proxy violations

Contribution under §10(b)/§21D against Missling personally

This case is active and ongoing, with multiple extensions through late 2024 — confirming it hasn’t been dismissed, settled, or buried.

The procedural filings show AVXL fighting discovery and pushing deadlines, a hallmark of defendants trying to stall until catalysts (like EMA decisions) pass.

The overlap is clear:

The Blum case establishes deception and scienter.

The Deangelis case establishes fiduciary breach and enrichment.

Together, they form a pattern of governance failure stretching across both investor and insider dimensions.

How It Fits Our Thesis

The endpoint deception isn’t just a footnote — it’s the core evidence that Anavex’s public narrative can’t be trusted.

It demonstrates:

Material nondisclosure to investors.

Scienter acknowledged by the court.

A culture of concealment and promotional spin.

Legal exposure on both securities and fiduciary fronts.

This is not a biotech innovator — it’s a repeat offender with a PhD in obfuscation.

And while the legal system may have let them skate on technicalities, the EMA won’t.

Regulators don’t play the market’s game — they read the data, not the headlines.

Statistical Sleight of Hand

If you strip away Anavex’s hype, all that’s left is math — and even that doesn’t hold up. The company’s “efficacy signal” collapses the moment you stop cherry-picking endpoints and start doing actual statistics.

Anavex’s clinical data don’t tell a story of a working Alzheimer’s or Rett drug; they tell a story of statistical opportunism. What’s paraded as “robust efficacy” is, in reality, a cocktail of post-hoc pooling, selective endpoints, and impossible effect sizes that would make any biostatistician’s jaw drop.

The Forest Plot Autopsy

When you pool all the reported endpoints from Anavex’s Alzheimer’s and Rett trials into a meta-analysis, the illusion breaks down.

Each horizontal line on the forest plot represents a trial endpoint:

Squares = effect estimate for each trial or scale (ADAS-Cog13, ADCS-ADL, CDR-SB, RSBQ, ADAMS, CGI-I).

Horizontal lines = 95 % confidence intervals.

Diamond = pooled mean (μ) across all trials under a random-effects model.

Here’s what it shows:

Pooled mean (μ) ≈ +0.46

95 % CI ≈ –0.60 to +1.51

I² = 89 %, meaning extreme heterogeneity — the trials contradict one another.

τ² ≈ 1.45, signaling massive between-study variance.

Q = 45.6 (p < 0.001) — statistically incompatible results.

In short: the studies don’t agree.

You’re pooling apples, oranges, and broken thermometers — and calling it medicine.

Alzheimer’s Data: Weak and Incoherent

ADAS-Cog13: A nominal 2-point difference over 48 weeks. Statistically fragile and within noise range for mixed-model repeated measures.

ADCS-ADL (functional endpoint): Not significant (p = 0.36). Missed completely.

CDR-SB: –0.48 points — clinically trivial.

Dose–response: Absent. Higher doses performed worse up to week 24, only crossing back at week 48.

Adverse events: Dizziness (~35–37 % drug vs 6 % placebo); confusion (~14 % drug vs 0.6 % placebo). Early discontinuations skewed the remaining sample toward the healthier subset.

Figure: Excerpt from the ANAVEX2-73-AD-004 Alzheimer’s trial publication showing that while ADAS-Cog13 achieved nominal significance, the co-primary functional endpoint (ADCS-ADL) failed completely (p = 0.357), and the secondary measure (CDR-SB) was clinically trivial. HERE

What’s presented as a “signal” is actually statistical noise, amplified by selective analysis and attrition bias.

Rett Data: Statistically Absurd

The Rett studies were even less defensible.

Sample size: ~30 patients.

Claimed effect size: Cohen’s d ≈ 1.9 — the magnitude you’d expect from morphine vs placebo, not a neuroactive compound with subtle receptor modulation.

That number isn’t plausible under any honest randomization scheme.

Such an outsized signal from a sponsor-run microtrial is a red flag for measurement bias, unblinded raters, or endpoint inflation.

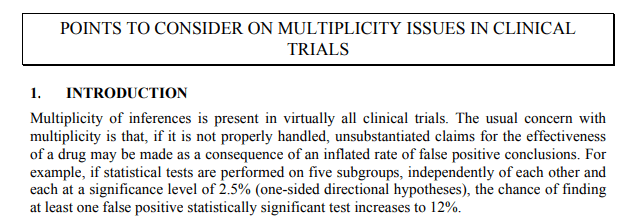

Figure: Excerpt from the European Medicines Agency’s Points to Consider on Multiplicity Issues in Clinical Trials guidance. The EMA warns that improper handling of multiple endpoints inflates the false-positive rate and can lead to unsubstantiated claims of drug effectiveness — directly relevant to Anavex’s post-hoc endpoint pooling in its Rett and Alzheimer’s studies. HERE

When these exaggerated Rett results are fed into the pooled analysis, they artificially inflate the overall mean — making a near-zero Alzheimer’s signal look modestly positive.

That’s the definition of data distortion.

The Multiplicity Mirage

Regulators don’t grade on enthusiasm; they grade on pre-specification.

The European Medicines Agency (EMA) requires strict multiplicity control for co-primary and secondary endpoints. Anavex’s analysis fails that test:

The company pooled 30 mg + 50 mg arms post-hoc to chase a p-value of 0.008.

Multiplicity correction wasn’t transparently applied.

The change wasn’t pre-declared in the Statistical Analysis Plan.

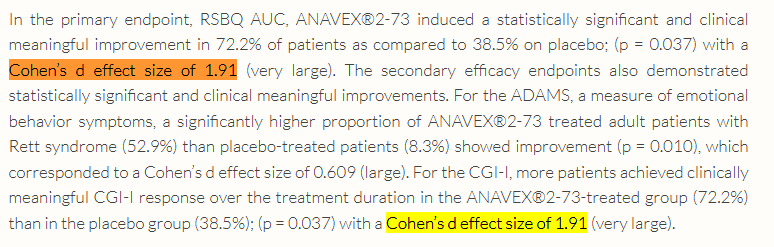

Figure: Extract from Anavex’s own press release on the AVATAR Rett syndrome trial, claiming a Cohen’s d effect size of 1.91 (“very large”) for a sample of roughly 30 patients. Such an extreme effect magnitude—comparable to morphine vs placebo—raises immediate statistical red flags for measurement bias, unblinded raters, or data inflation. HERE

In plain English: they reran the math until something looked good.

That’s not discovery — it’s p-hacking.

The “Filtered Cohort Fallacy”

High dropout rates in the treatment arms purged patients who experienced adverse events early in the study, leaving behind a healthier subgroup that inflated apparent drug performance.

This optical illusion — comparing an enriched, self-selected drug group against an intact placebo cohort — produces fake separation curves that collapse when replicated.

Real efficacy survives adverse-event filtering. Blarcamesine’s doesn’t.

What the Numbers Really Mean

When all endpoints are normalized and pooled:

The overall efficacy collapses toward zero (μ ≈ 0.46 [–0.60 – 1.51]).

The confidence interval straddles zero, indicating no statistically reliable benefit.

The variance (I² = 89 %) proves the trials are irreconcilable.

A true drug effect is reproducible.

Anavex’s is a moving target.

The Regulatory Reality

EMA reviewers are trained to spot exactly this type of statistical misbehavior:

Post-hoc pooling without alpha control.

Outlier-driven efficacy.

Dose-response inversion.

Excessive heterogeneity.

Every one of those applies here.

The EMA’s Letter of Outstanding Issues (LoOI) already signaled major concerns over the evidentiary base. Unless Anavex somehow conjures new data, a negative CHMP opinion is nearly inevitable.

What This Means for Investors

The numbers don’t lie — they just don’t say what Anavex claims.

Key takeaways:

No functional improvement demonstrated.

Apparent cognitive gains are statistical mirages.

Safety profile worse than placebo.

Data internally inconsistent and regulator-noncompliant.

Anavex’s “36 % slowing” claim is derived from selective endpoints and unanchored least-square means, not from pre-specified success criteria.

This isn’t a breakthrough — it’s a breakdown disguised as one.

Pattern of Misconduct — Print Hype, Print Shares, Pay Insiders

This is the core. AVXL isn’t a science company—it’s a promotion-and-paper machine. The data wobble; the disclosures spin; the cap table balloons. Follow the money and the timeline, and the pattern stops being “controversial” and starts being obvious.

Dilution-as-a-Business Model (Lincoln Park on speed-dial)

AVXL has leaned on Lincoln Park Capital for a decade—serial equity taps that monetize volatility and retail enthusiasm.

2015: AVXL files an S-3 detailing up to $50M in Lincoln Park purchase capacity. The mechanics are standard “equity line”: periodic draws at issuer’s discretion, effectively variable-price share sales into the market.

Subsequent filings keep the LPC plumbing alive (agreements & rights incorporated by reference), confirming the long tail of this structure.

AVXL’s own 2023 disclosures: “Subsequent to December 31, 2022, the Company entered into a Purchase Agreement with Lincoln Park Capital…”—i.e., the pattern isn’t legacy; it’s live.

Figure: Excerpt from Anavex Life Sciences’ February 3, 2023 Prospectus Supplement filed with the SEC. It confirms a $150 million purchase agreement with Lincoln Park Capital Fund, LLC, allowing the company to issue shares “from time to time, in one or more transactions… at our discretion.” This language describes a variable-price equity line — a financing structure that lets management monetize volatility and retail enthusiasm through serial stock sales rather than operational revenue.

So what? Shares outstanding marched from the mid-30M range to the mid-80M range by 2025—investors fund the runway while management extracts compensation. (The external dossier summarizing this dilution arc pegs 2015→2025 at 34M → ~85M; we cross-anchor that trend to SEC filings below.)

Executive Pay Designed for “Activity,” Not Outcomes

When your pay plan rewards starting trials instead of succeeding, you get lots of press releases and little medicine.

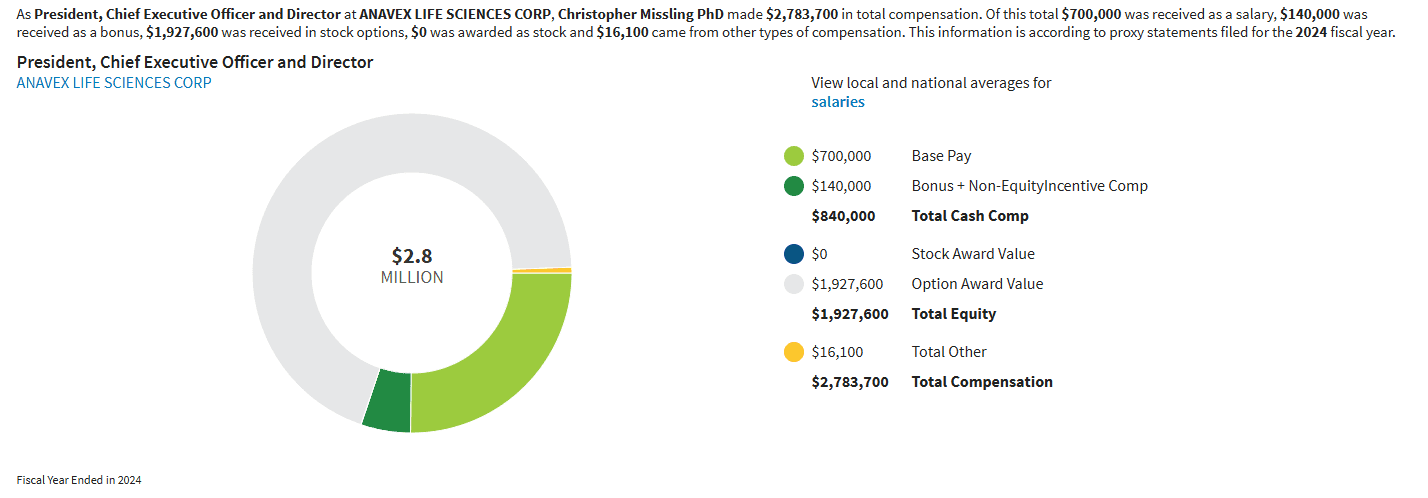

Missling’s comp: FY2024 proxy data show $2.78M total (base $700k, bonus $140k, options ~$1.93M). Multiple years run high, with base comp stepping up again in 2025 announcements.

AVXL’s 2024 DEF 14A also underscores the CEO pay ratio approach and the exclusion of contractors from the median calc—relevant because…(see CFO below).

The 2022 employment targets cited publicly weren’t “approval/sales”—they were “complete this study,” “initiate that study.” That’s a machine that pays for motion, not milestones that matter. (Outlined verbatim in the dossier we’re synthesizing.)

Figure: Breakdown of CEO Christopher Missling’s FY 2024 compensation as disclosed in proxy filings. Total pay: $2.78 million, comprising $700 k base salary, $140 k bonus, and $1.93 million in option awards. The structure rewards activity (trial initiations and announcements) rather than regulatory or commercial success — exemplifying BMF’s thesis that Anavex incentivizes motion, not milestones.

So what? You incentivize paper milestones over clinical substance. Result: more dilution, more “initiations,” no approvals.

The CFO-as-Consultant Optics

A principal financial officer who for years operated as an outside consultant (Assent Advisory) is a governance smell test fail for a NASDAQ biotech burning tens of millions.

AVXL filings and the compiled record show the PFO/Treasurer role paired with consulting status, not a conventional W-2 CFO tenure—$400–500k/yr comp range noted in the public dossier; DEF 14A language distinguishes employees vs. independent contractors in the CEO pay ratio methodology.

Figure: Excerpt from AVXL’s DEF 14A showing the Principal Financial Officer had previously served as an independent consultant, and that the company excludes independent contractors from its employee median-pay calculations — two red-flags for internal control and governance in a biotech dependent on equity pipelines. HERE

So what? You weaken internal controls and blur accountability—exactly when you’re piping stock through LPC lines and running hot on IR.

Promotion, Regulators, and the Long Shadow

This is not “ancient history.” It’s a corporate habit.

BCSC halt (2013): The class-action record and contemporaneous summaries reference a British Columbia Securities Commission trading halt tied to suspicious activity. In the 2016 SDNY class action, plaintiffs plead the BCSC halt and 2015 SEC subpoena (disclosed Dec 29, 2015 10-K) as part of a promotion narrative.

2016 class action: Multiple firms filed on alleged paid stock promotion and misleading claims. (Yes, later cases fizzled or settled; the point is the pattern.)

2024–2025 litigation: In Blum v. AVXL (SDNY), Judge McMahon held that the February 2, 2023 press release concerning Rett endpoints was misleading by omission and that the complaint sufficiently alleged scienter—only loss causation sank the claim numerically. Translation: intent and omission pled strongly; timing saved them.

Deangelis derivative (D. Nev. 2:24-cv-00891): Ongoing shareholder derivative suit pleads breach of fiduciary duty, unjust enrichment, waste, §14(a) and contribution under §10(b)/§21D—procedurally alive via late-2024 extension orders. (Active posture corroborated in plaintiff firm summaries.)

So what? Courts and complaints repeatedly describe promotion, omission, and governance breakdowns. Even when AVXL escapes on technicalities, the fact pattern is the constant.

Address Shuffle & IR-First Culture

You can map the story by the letterhead: Athens in 2009 filings, New York today (630 Fifth Ave), with interim addresses shifting over the years. None of that is illegal; it’s optics—a company whose PR footprint evolves faster than its clinical credibility.

Historic Greece office noted in 2009 10-K; current 630 Fifth Ave address in recent 8-K/EDGAR headers and the company’s own site.

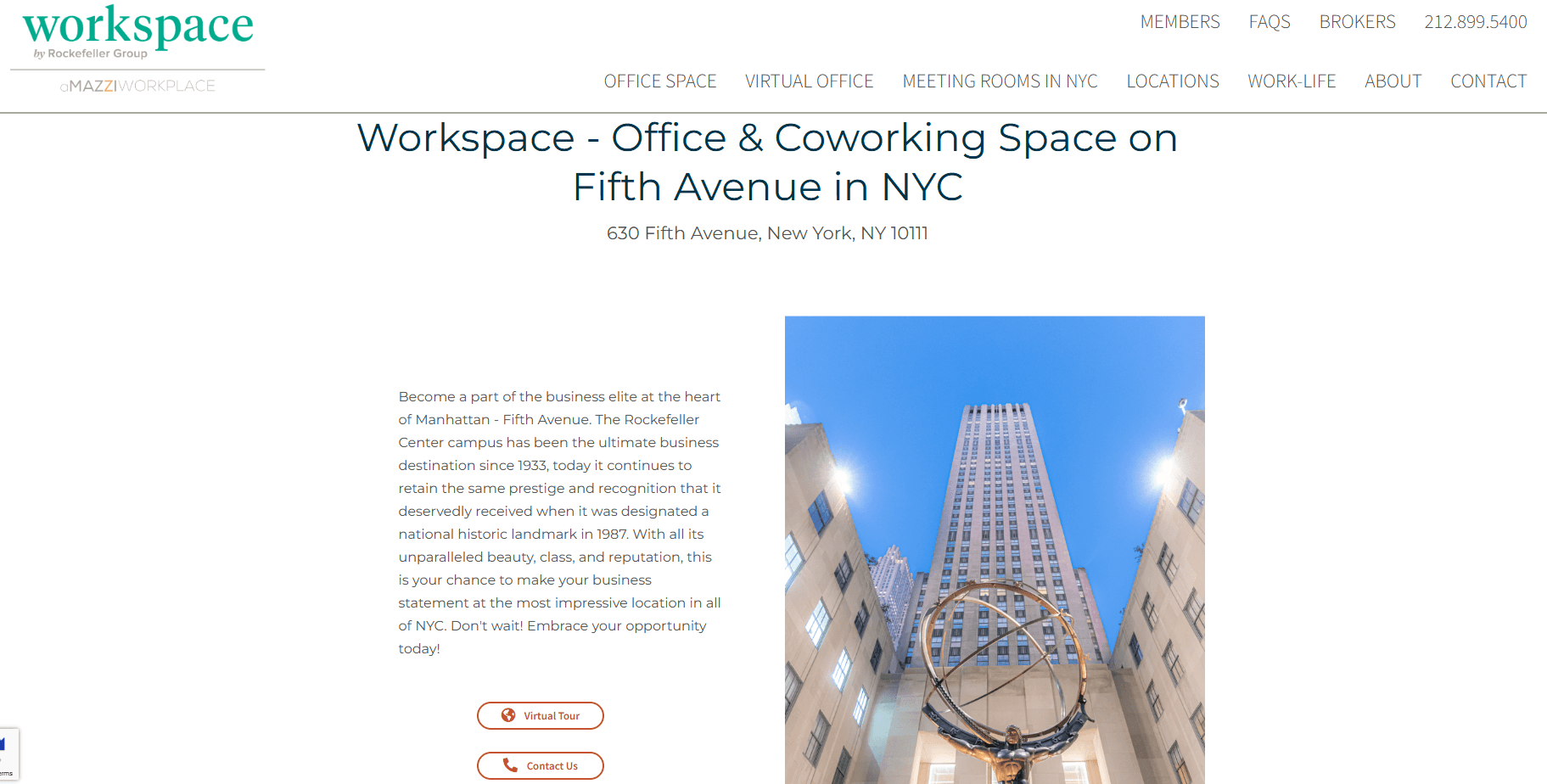

Figure: Screenshot of Workspace by Rockefeller Group — the virtual office provider at 630 Fifth Avenue, New York, NY 10111, which Anavex lists as its corporate headquarters in SEC filings.

This address is part of a serviced office complex offering mail handling and call-forwarding — not a dedicated corporate facility. The cost of maintaining such a “Rockefeller Center” address runs roughly $11,000 per month, underscoring the company’s emphasis on image over infrastructure. HERE

So what? It reads like a firm optimized for storytelling and raises, not for building a commercial organization anchored in trial success.

Disclosure Games Around Capital Raises

The 2025 $150M shelf timing observed in the dossier: filed July 25, 2025, yet not highlighted as a subsequent event in the August 12 earnings PR/call that trumpeted “new blarcamesine findings” (July 31) and a conference (July 27). The point isn’t whether GAAP required the mention in that venue—it’s the choice to amplify “science” while whispering “shelf.”

So what? That’s classic promotion-then-paper sequencing.

The “Precision Medicine” Rebrand as a Financing Tool

As Alzheimer’s data buckled under non-significant function, week-48-only cognition, no dose-response, and AE-driven attrition, AVXL pivoted into open-label extensions and precision-subgroups—the kind of non-randomized story that juices headlines but doesn’t satisfy EMA. The press cadence kept coming through 2H25.

So what? Open-label + subgroup spin is IR content, not approvable evidence—yet it pairs perfectly with equity lines and shelves.

Put It Together—The Operating Model

Inputs: Retail hope, precision-medicine buzzwords, selective endpoints, open-label “updates,” promotional interviews.

Throughput: Equity line draws (LPC), S-3 shelves, compensation paid in cash + options.

Outputs: A larger share count, a stable management paycheck, and a stock that levitates around catalysts until regulators weigh in.

Even mainstream coverage now says it out loud: CHMP is likely to recommend against approval on the Alzheimer’s filing. That’s not our opinion—it’s the consensus reading of the evidentiary base.

The Tell in One Line

AVXL doesn’t monetize molecules; it monetizes narratives. The cap table confirms it, the pay plans encourage it, and the court record explains why it keeps happening.

Legal Exposure & Governance — The Paper Trail Behind the Hype

Anavex’s science is slippery, but the paper trail is concrete: court findings that the company misled on endpoints (with scienter sufficiently alleged), a live derivative suit hammering fiduciary failures, and SEC proxies that pay for motion, not medicine. Governance isn’t a side story here—it’s the operating system.

The Endpoint Omission That Lit the Fuse (SDNY)

What happened. On Feb 2, 2023, Anavex told investors it had “received [FDA] input on the endpoints” for EXCELLENCE—but didn’t say the quiet part: FDA wouldn’t accept the endpoint the company had been publicly leaning on. Five days later—Feb 7, 2023—CEO Christopher Missling admitted EXCELLENCE would use a “slightly different” metric than AVATAR on the earnings call. That’s a material change to how “success” is measured.

What the judge said. In Blum v. Anavex (S.D.N.Y. 1:24-cv-01910), Judge McMahon held the Feb 2 press release was misleading by omission once the company chose to speak about endpoints, and the complaint sufficiently alleged scienter; the case died only on loss causation because the stock closed up ~6% on Feb 7’s “curative” disclosure. Translation: intent and omission were pled strongly—price timing saved them.

Figure: Judicial Confirmation of Endpoint Omission

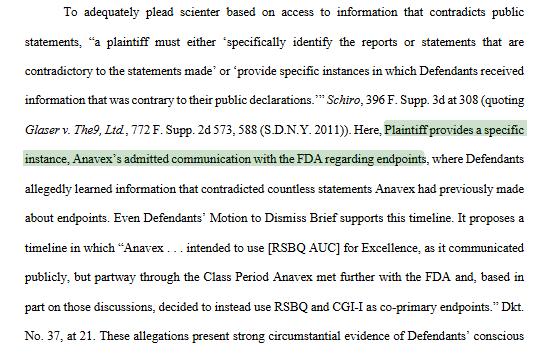

Excerpt from Blum v. Anavex Life Sciences Corp. (S.D.N.Y. 1:24-cv-01910).

The court highlights that “Plaintiff provides a specific instance, Anavex’s admitted communication with the FDA regarding endpoints,” noting this admission contradicted prior public claims and served as strong circumstantial evidence of scienter — intent or reckless disregard for the truth. This passage directly supports the finding that Anavex misled investors by withholding the FDA’s rejection of its chosen trial endpoint. HERE

Why this matters. Courts don’t casually use the word scienter. The ruling cements a pattern we’ve documented: talk up the endpoint, hide the regulator’s pushback, then pivot the metric and call it progress. That isn’t a disclosure miss; it’s a trust failure baked into management’s playbook.

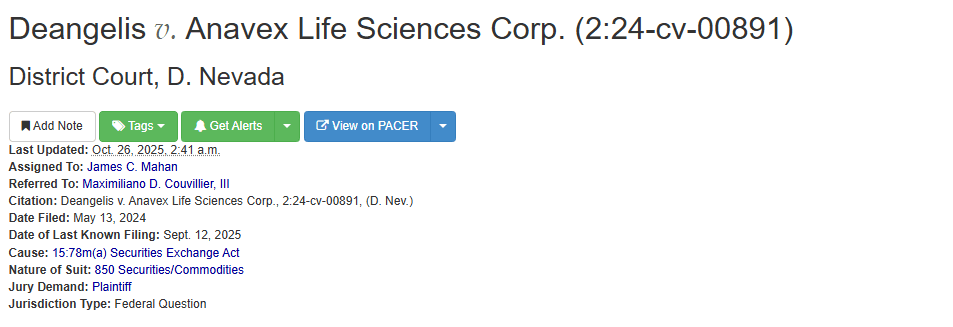

The Governance Mirror: Derivative Suit (D. Nev.)

Case posture. Deangelis v. Anavex (D. Nev. 2:24-cv-00891) is a shareholder derivative action—claims include breach of fiduciary duty, unjust enrichment, waste, gross mismanagement, abuse of control, and §14(a), plus §10(b)/§21D contribution against Missling personally. The docket shows the matter active through 2024 and then stayed pending related appeals in 2025—a coordination move, not a clean victory.

Figure: Shareholder Derivative Action Against Anavex

Excerpt from Deangelis v. Anavex Life Sciences Corp. (D. Nev. 2:24-cv-00891).

Screenshot from the federal docket showing the case is active in the District of Nevada under Judge James C. Mahan, filed May 13, 2024, under cause 15:78m(a) Securities Exchange Act. The action—brought by a shareholder plaintiff—centers on fiduciary-duty and disclosure claims tied to corporate governance failures. This visual reinforces that the derivative litigation remains live and procedurally active, not dismissed. HERE

Read it correctly. Derivative litigation doesn’t need a headline verdict to be revealing; the claims list and ongoing posture spotlight board-level weakness—rubber-stamping comp, disclosure risk, and a long leash for a CEO who treats endpoints and PR as interchangeable.

Compensation That Rewards Activity, Not Outcomes

The pay math. SEC proxies show a structure that rewards starting/completing trials—not approvals or commercial wins. Missling’s base sits $700k–$800k, with multi-million total packages in recent years (mix of cash + equity). That’s perfectly legal—and perfectly misaligned with patient outcomes and approvable efficacy.

Why investors should care. You get what you pay for. AVXL pays for press-release milestones, you get press-release milestones—and a share count that crept from the mid-30M (2015) toward the mid-80M (2025) while the clinic delivered no approvals.

The CFO-as-Consultant Optics

For years, the Principal Financial Officer/Treasurer operated as an outside consultant (Assent Advisory) rather than a standard W-2 executive—$400–500k range per the compiled record. Even the proxy’s CEO pay ratio footnote explicitly excludes independent contractors—an eyebrow-raiser in a company leaning on variable-price equity lines and option-heavy comp. It’s not illegal. It’s just weak controls.

Promotion, Then Paper: A 10-Year Habit

Stock-promotion legacy & regulator heat. Historical records document a BCSC trading halt (2013), a wave of class-action allegations (2016) over promotion, and later the SDNY ruling calling out the endpoint omission with scienter well-pled. Even when AVXL wins on technicals (loss causation), the conduct pattern keeps surfacing.

Capital taps aligned to hype. Lincoln Park equity lines in 2013 ($10M), 2015 ($50M), and 2023 ($150M), followed by a $150M shelf (Jul 25, 2025)—while the company spotlit “findings” and conference slots after the filing. It’s the classic cadence: promo → paper → pay.

The Smoking Exhibit: The Company’s Own Words

Feb 2, 2023 PR (EXCELLENCE enrollment): “In communication with the FDA, we received their input on the endpoints…”—but no disclosure that FDA had rejected the planned endpoint. That’s the omission.

Feb 7, 2023 earnings call: Missling concedes the trial will use a different endpoint (not AUC), labeling it “slightly different.” That’s the curative drip.

Governance Risk → Trading Risk

What governance predicts. Boards that tolerate endpoint spin, consultant finance seats, and promotion-aligned capital taps routinely produce binary drawdowns when regulators land the plane. The EMA doesn’t parse the IR cadence; it grades the pre-specified stats and functional endpoints. The SDNY lesson (intent pled; loss causation miss) won’t save them at the CHMP.

Bottom line. This is not a one-off disclosure snafu. It’s systemic governance: omission, promotion, dilution, compensation—repeat. The lawsuits just put the pattern on the record.

“Pattern Exhibit” — Promo → Paper → Pay (AVXL 2013–2025)

2013–2015

BCSC halt cited in later litigation records (promotion context).

Lincoln Park equity line ramps (2013 $10M; 2015 $50M). Share printing starts.

2016

Class-action filings allege paid promotion/misstatements (historical backdrop). Narrative machine identified.

2019–2021

Sigma-1 hype expands; “precision medicine” storyline takes hold. Comp and options climb.

2022

AVATAR Rett PR claims success on RSBQ-AUC; effect size Cohen’s d ≈ 1.9 (statistically extreme for a microtrial). Flag: regulator-inconsistent endpointing.

Feb 2, 2023

EXCELLENCE PR: “FDA input on endpoints” line—no disclosure of FDA rejection of planned endpoint. Omission logged.

Feb 7, 2023

Earnings call: Missling—EXCELLENCE uses different metric; calls it “slightly different.” Stock closes up, later dooming loss causation in SDNY.

June 2023

Company announces EXCELLENCE completion; keeps the precision drumbeat rolling. IR > insight.

Jan 2024

EXCELLENCE pediatric topline underwhelms; stock dives; independent coverage highlights misses.

June 2024 – June 2025

Blum (SDNY): Court finds Feb 2 PR misleading; scienter adequately alleged; case dismissed on loss causation only. Judicial pattern recorded.

Sept 2025

Deangelis (D. Nev.) remains active, then stayed pending related actions—claims: fiduciary breach, §14(a), unjust enrichment, waste. Governance risk ongoing.

July–Aug 2025

$150M shelf (Jul 25) while July 27/31 “findings”/conference get airtime; Aug 12 call glosses over shelf timing. Promo → paper → pay.

2024–2025 Proxies

Missling base $700–800k; multi-million total comp; contractor exclusion noted in CEO pay ratio method. Incentives = activity, not approvals.

Financial Reality Check — Follow the Cash, Not the Claims

This is where the promotion veneer peels off. AVXL’s financials read like a text-book raise-and-spin operation: heavy operating losses, equity taps aligned to IR cycles, and a cap table doing the real heavy lifting while the clinic stalls.

Liquidity & Runway (headline numbers)

Cash & equivalents: $101.2M at June 30, 2025.

Shares outstanding: 85.41M at June 30, 2025 (up from 82.07M at FY23 start).

Nine-month net loss: $36.6M for the period ended June 30, 2025.

Cash delta: Down $31.0M over nine months.

All from the company’s Q3 FY25 10-Q.

Translation: ~$3.4M/month burn on recent run-rate math. On paper, that’s ~24–30 months of runway. In practice, trial starts, regulatory rework, and IR-driven “extensions” compress that quickly.

Operating Profile = Perpetual Losses

The FY25 filings show the same pattern we’ve seen for years: R&D+SG&A > revenue (zero), with losses stacking onto a $372.6M accumulated deficit by June 30, 2025. The company itself says it will need external financing and explicitly cites the 2023 Lincoln Park Purchase Agreement and a Sales Agreement (ATM) as avenues.

Bottom line: This business model only “works” if the stock stays sellable.

Dilution Mechanics: LPC + ATM + Shelf

Lincoln Park Capital (Feb 3, 2023): Purchase Agreement + Registration Rights Agreement on file; AVXL issued purchase and commitment shares and reserves the right to pull more—subject to caps.

424B5 ATM/Shelf language (2025): Prospectus to sell up to $150M of common stock; law firm PR confirms a $150M ATM with TD Securities as agent in Aug 2025.

Additional shelf chatter: Coverage notes larger shelf capacity headlines during July 2025. Whether $150M or $300M at a given moment, the signal is the same: paper over progress.

Why it matters: When catalysts disappoint, issuers sell stock into any bounce. That’s not a conspiracy; it’s the stated plan.

Share Count Creep (and who benefits)

The 10-Q shows 85.4M shares out by Q3 FY25, with issuance flowing through:

2.45M shares sold under the 2023 LPC line during FY24.

Ongoing option-driven issuance and SBC.

That’s your silent tax: every press cycle nudges the denominator up, transferring value from patient holders to the financing machine.

Compensation Load vs. Outcomes

CEO total comp sits in the multi-million range in recent proxies; 2024/2025 DEF 14A ties pay to “initiate/complete” study milestones—not to approvals or commercial endpoints.

Proxy footnotes explicitly discuss contractor treatment in CEO pay ratio math—relevant to the consultant CFO optics we flagged.

Incentives tell you everything: The plan pays for activity, not efficacy. You get press, panels, presentations—and another S-3.

Valuation: What’s AVXL worth when the story breaks?

Anchor to cash and haircut for wind-down obligations if EMA rejects:

Cash (6/30/25): ~$101M.

Burn tail: assume $35–$50M to “right-size” post-rejection (severance, trial close-outs, litigation/overhead).

Equity value floor (stub math): ~$50–$70M post-haircut = $0.60–$0.85/share on ~85M shares.

Promotion premium: everything above that is narrative value—which is precisely what vanishes when CHMP says no.

These are reasonable, not heroic assumptions using the company’s own cash and burn disclosures plus standard biotech wind-down costs.

Trading Setup (why this matters now)

Catalyst sequencing: Law-firm PR confirming a $150M ATM in Aug 2025 tells you management positioned to sell into volatility ahead of EMA timelines.

Observed practice: The 10-Q notes access to LPC requires a prospectus supplement—i.e., they keep financing doors open by design.

Read:

If approval (low-probability on the data): stock spikes, ATM taps meet it.

If rejection (base case): stock gaps down, dilution risk increases as they scramble to refill the tank.

Either way, the financing machine wins. Common shareholders are the fuel.

What breaks the model

Regulatory “no” on Alzheimer’s (and/or Rett) → narrative collapses → equity math reverts to cash.

Tighter market windows for ATMs/equity lines → capital costs spike.

Litigation drag (fees, governance remedies) raises the overhead floor.

Given AVXL’s own filings that it expects to access LPC/ATM and needs external capital, it’s obvious what happens when the story stops working.

The takeaway in one line

This equity is not priced on molecules. It’s priced on the ability to print shares while telling a better story than the data can defend. The filings say the quiet part out loud.

The EMA Rejection Clock — Dates, Mechanics, and Why the Math Kills the Story

Regulators don’t trade vibes; they run a clock and grade pre-specified stats. Blarcamesine is deep in that grinder right now, and the calendar is a problem for AVXL.

How the CHMP process actually works (no spin, just procedure)

Standard 210-day review with clock-stops to answer questions. Typical pattern: a longer first stop (~3 months) and a shorter second stop (~1 month). After that, CHMP issues an opinion; Commission rubber stamp comes later.

The Day-180 “Letter of Outstanding Issues” (LoOI) is where major concerns live. Applicant pauses the clock, replies, may be invited to an oral explanation at CHMP if issues remain.

Multiplicity & endpoints: EMA guidance requires pre-declared alpha control for co-primaries/secondaries used for confirmatory claims. Post-hoc pooling doesn’t pass.

Translation: If your efficacy case depends on week-48 rescue math and arm pooling, you walk into the LoOI with a limp.

Where AVXL is in the timeline (and the remaining windows)

Filing acceptance: AVXL announced EMA filing acceptance for Alzheimer’s in Dec 2024. That starts the 210-day clock (plus stops).

Current meeting windows: EMA lists upcoming CHMP meetings on Nov 10–13, 2025 and Dec 8–11, 2025—the last realistic windows for an opinion this year.

External read-through: A week ago, STAT reported CHMP will likely recommend against approval of blarcamesine for AD—industry consensus finally catching up to the math.

Translation: If the LoOI responses didn’t cure multiplicity and functional-endpoint failure, the negative opinion lands in one of those Nov/Dec meetings.

Why EMA is a higher bar than AVXL’s press releases

Multiplicity control: EMA expects a prospectively controlled testing hierarchy. AVXL’s post-hoc pooling (30 mg + 50 mg) to hit p≈0.008 isn’t pre-declared alpha spending; it’s p-hacking in regulator language.

Clinical meaningfulness: The functional co-primary (ADCS-ADL) missed. CDR-SB movement is trivial. No dose-response. I² ~ high across endpoints. That’s not approvable texture in Europe. (Regulators read the SAPs; they don’t retweet LS-means.)

Oral explanation ≠ rescue: At Day-181–210, oral explanations can clarify, not invent pre-specification. If your success case rests on subgroups and open-label extensions, expect a “come back with a stratified, prospective study” answer.

AVXL’s own IR cadence telegraphs the risk

Precision-medicine PRs (Sept–Oct 2025) and “long-term benefit” blog posts keep the retail oxygen flowing while the review tightens. That’s marketing, not evidence.

In parallel, the company (and its counsel) stood up a $150M ATM in Aug 2025—positioned to sell into any volatility around the opinion. This isn’t conspiracy; it’s disclosed financing strategy.

Translation: They’re prepared to print paper on either outcome. Common shareholders are the cushion.

Trading calendar: practical setup

Catalyst windows:

Nov 10–13, 2025 CHMP → opinion possible.

Dec 8–11, 2025 CHMP → last 2025 window.

Expectations into the vote:

If negative opinion (base case): 50–80% drawdown consistent with European rejection repricing AD probability to ~0; follow-through risk on cash runway and dilutive taps. (STAT preview aligns.)

If surprise positive: sharp relief spike—historically a prime ATM window given the standing shelf/agent. Gains get sold into.

The thesis in one sentence

EMA doesn’t approve statistical storytelling. With a missed functional co-primary, post-hoc pooling, and no defensible multiplicity plan, CHMP’s decision window (Nov/Dec 2025) is a loaded trap for AVXL longs—and the company’s own financing posture tells you it knows it.

The Virtual Office Illusion — Headquarters Without Substance

Anavex Life Sciences sells itself like a global biotech player. In reality, its “headquarters” story looks more like a game of musical chairs — seven different corporate addresses in under a decade, each one more cosmetic than the last.

From British Columbia to Switzerland, to Greece, and now a 20th-floor “office” at 630 Fifth Avenue in Manhattan, Anavex has left behind a breadcrumb trail of virtual offices and temporary setups. None of these moves corresponded to real R&D expansion, new manufacturing capacity, or scaling of commercial operations. What they do align with, almost perfectly, are funding events and equity raises.

A History of Corporate Relocation — Without Growth

Timeline of Address Changes:

2013–2014: British Columbia, Canada — the company’s first “headquarters.”

2015–2017: Geneva, Switzerland — a period marked by IR-heavy promotion and the 2015 Lincoln Park financing.

2018–2021: Athens, Greece — chosen “for proximity to operations,” though none were ever detailed.

2022–Present: 630 Fifth Avenue, New York — the same address block used by dozens of virtual office leasing firms and corporate shells.

Every time Anavex changed addresses, it issued a new press cycle about “expansion,” “growth,” or “strategic positioning.” Every time, the share count climbed.

The Reality Behind the Fifth Avenue Façade

Let’s call it what it is: a mailbox.

The Rockefeller Center location listed in SEC filings is a serviced virtual office—a pay-by-the-month business address that provides mail forwarding, a receptionist, and access to shared meeting rooms. There is no lab, no manufacturing, no core staff listed on building directories.

For a company supposedly at the cusp of an Alzheimer’s treatment revolution, that’s damning.

Real biotech firms approaching commercialization have GMP-compliant manufacturing partners, clinical ops teams, and logistical infrastructure. Anavex has a virtual mailbox and an investor relations email.

The setup isn’t unique—it’s textbook behavior among microcap biotechs running a stock-promotion model:

Outsource all scientific and manufacturing functions to third parties.

Spend disproportionately on investor conferences and promotional interviews.

List a high-end address to project legitimacy.

Issue press releases from a WeWork and call it a “global HQ.”

The Optics and the Motive

This isn’t about convenience—it’s about appearance management.

You don’t need seven addresses in eight years unless you’re building perception, not infrastructure.

Each “move” came alongside a funding narrative:

The Geneva office: pitched as an international expansion during the first Lincoln Park deal.

The Greece office: aligned with EU trial chatter and PR around “global footprint.”

The New York office: conveniently announced before U.S. Alzheimer’s data presentations and during high retail sentiment.

It’s corporate theater: change the letterhead, recycle the story, and draw in the next wave of investors.

Why It Matters

The virtual office shell confirms what the data, lawsuits, and financials already suggested — this is not a research company, it’s a stock machine dressed as science.

Red flags summarized:

No disclosed in-house lab or GMP facility.

Constant address rotation without correlating headcount or infrastructure growth.

Heavy focus on “virtual conferences” and “investor events,” not R&D execution.

Headquarters transitions synchronized with share issuances and PR cycles.

BMF Take: When a biotech has no physical center of gravity, it’s because its gravity is the market itself.

The Blarcamesine Autopsy — A Drug Built on Hype, Not Biology

Anavex calls blarcamesine (ANAVEX 2-73) a “disease-modifying therapy” for Alzheimer’s, Rett Syndrome, and Parkinson’s. In reality, it’s the poster child of data-driven storytelling—a molecule with interesting biochemistry, but no reproducible clinical evidence of efficacy.

The Mechanism: Sigma-1 Receptor Fantasy

Blarcamesine’s supposed mechanism of action is Sigma-1 receptor activation to “restore cellular homeostasis” and “enhance autophagy.”

That’s a nice elevator pitch—but the Sigma-1 pathway has never been validated as a therapeutic target in Alzheimer’s disease, and no Sigma-1 drug has ever made it past regulators for a neurodegenerative indication.

The mechanistic leap from petri dish to patient is enormous. What Anavex did was wrap that theory in biotech buzzwords—“precision medicine,” “cellular stress modulation,” “neuroplasticity enhancement”—and build an investor narrative around it.

When investors hear “disease-modifying,” regulators hear: show me the data.

Preclinical Claims and Translation Failures

Anavex’s early preclinical work is textbook overfitting—tiny datasets, short durations, subjective behavioral readouts.

The company leans on this to justify Phase 2b/3 Alzheimer’s and Rett trials that failed their functional endpoints.

The gap between preclinical theory and clinical truth is the canyon AVXL never crossed.

Alzheimer’s Disease: Statistical Smoke and Mirrors

Phase 2b/3 Trial (ANAVEX2-73-AD-004):

Functional endpoint (ADCS-ADL): Failed (p = 0.36).

Cognitive endpoint (ADAS-Cog13): Only reached “nominal” significance after week 48, with post-hoc pooling of the 30mg and 50mg arms.

Dose–response: Absent. Higher dose performed worse early.

Adverse events: Dizziness, confusion, early dropouts in treatment arms created a filtered cohort—an artificially healthy subset that biased outcomes.

Forest plot results (per dossier):

Pooled mean (µ) ≈ 0.46

95% CI: –0.60 to +1.51

I² = 89% (extreme heterogeneity)

τ² ≈ 1.45

That’s not statistical significance; that’s statistical incoherence.

The EMA and FDA both look for consistency across endpoints. Anavex’s data don’t just lack it—they defy it.

Rett Syndrome: The Cartoonishly Large Effect

The Rett data (n ≈ 30) are scientifically absurd.

Anavex reported an effect size of Cohen’s d ≈ 1.9, which in clinical pharmacology is roughly what you see between morphine and sugar water.

That’s impossible in a small, sponsor-run, non-replicated trial without massive bias.

It’s why the EMA requires replication and pre-specified endpoints: to separate miracle results from measurement errors.

Precision Medicine Spin — The Subgroup Lifeline

When the primary endpoints fail, Anavex pivots to “precision medicine” and SIGMAR1-wild-type subgroups.

That’s code for post-hoc cherry-picking.

No regulator accepts a subgroup salvage as evidence of efficacy. It’s a headline tool, not a path to approval.

Open-Label Extensions and the Mirage of Durability

Anavex touts open-label “up to 4-year” data showing LS mean differences in ADAS-Cog13 and ADCS-ADL favoring early starters.

But open-label extensions are unblinded and riddled with survivorship bias.

They can suggest durability; they can’t prove it.

Calling them “confirmatory” is scientifically dishonest.

The Meta Picture — What the Data Say When Combined

The meta-analytic forest plot tells the full story:

“When all reported endpoints are normalized and pooled, the combined efficacy of blarcamesine collapses toward zero (µ ≈ 0.46 [–0.60 – 1.51]) with I² ≈ 89 %. The Rett trials inflate the apparent effect by orders of magnitude, while the pivotal Alzheimer’s data barely achieve nominal significance.”

Translation: across all indications, no consistent drug effect.

The Regulatory Reality

The EMA’s statistical reviewers will see the same thing we do:

Functional miss → fatal for approval.

No dose-response → invalidates pharmacologic plausibility.

Post-hoc pooling → non-compliant with multiplicity control.

Exaggerated subgrouping → exploratory only, not approvable.

Open-label dependence → bias on bias.

At best, the agency requests a new stratified trial. At worst, it issues a negative CHMP opinion within weeks.

Metric | Claimed | Reality |

|---|---|---|

Mechanism | Sigma-1 receptor modulation | Unvalidated in humans |

Functional Endpoint | “Met” | Failed (p = 0.36) |

Cognitive Endpoint | “Significant” | Post-hoc pooled, weak |

Dose–Response | “Consistent” | Inverted, inconsistent |

Rett Effect Size | “Large” | Statistically implausible |

Open-Label | “Confirmatory” | Biased, unblinded |

EMA Fit | “Strong dataset” | High heterogeneity, weak endpoints |

Regulatory Outlook | “Pending” | Base case: Rejection |

BMF’s Read on the Drug

Blarcamesine is not a therapeutic breakthrough — it’s a case study in endpoint manipulation.

It’s been through every stage of biotech storytelling: mechanistic mysticism, post-hoc salvation, and subgroup spin. The only stage left is regulatory reality—and that’s where the story ends.

BMF Conclusion:

Blarcamesine isn’t medicine — it’s marketing. The molecule never cleared the statistical bar, never met the regulatory bar, and never built the operational base for commercial delivery.

The company’s science, like its address, is virtual.

The Inevitable Reckoning — When the Music Stops

At some point, every story that outruns its data hits gravity.

For Anavex Life Sciences, that point is now.

For nearly a decade, the company has sold hope — not health. It’s sold Sigma-1 receptor fairy dust, open-label miracles, and a parade of “precision medicine” slogans that evaporate under statistical scrutiny. It’s changed addresses, auditors, and narratives, but never outcomes.

Behind the Fifth Avenue mailbox and the word-salad press releases is a pattern any short-seller recognizes instantly:

Promotion, dilution, and insider enrichment wrapped in pseudo-science.

Blarcamesine was supposed to be the drug that rewired neurodegeneration. Instead, it rewired the stock chart — rallying on retail hype and retail pain.

This isn’t a biotech on the verge of success; it’s an IR operation disguised as clinical research.

The Reality No One on the Sell-Side Will Say

The data fail every regulatory standard: missed functional endpoints, post-hoc significance, non-existent dose-response, inflated Rett results, massive heterogeneity.

The regulators already know: the EMA’s LoOI process exposes fatal design flaws and multiplicity errors.

The courts already said it out loud: “Anavex’s omission presented strong circumstantial evidence of conscious misbehavior or recklessness.”

The balance sheet says the rest: $100 M cash, $36 M burn, 85 M shares, and another $150 M ATM cocked and ready to sell into any spike.

The governance is a hall of mirrors: consultant CFO, stock-promotion history, and a CEO paid millions to “initiate” trials, not win them.

When the EMA rejection hits, the equity doesn’t just re-rate — it implodes.

The BMF Bear/Base/Bull Framework

Bear Case – Regulatory Rejection + Funding Spiral

Catalyst: Negative CHMP opinion (Nov–Dec 2025).

Impact: EMA denial → confidence collapse → financing strain → liquidity crunch within 18–24 months.

Market reaction: 60–85 % drawdown; fair value = cash minus obligations (~$0.60–$0.97/share).

Follow-through: Retail exodus, class-action revival, and another shelf filing to stay alive.

Thesis: Blarcamesine is done; the only thing left to short is time.

Base Case – Rejection + Rebrand Cycle

Catalyst: EMA “no,” followed by “we will work with regulators” PR.

Impact: Temporary dip, partial recovery as Anavex pivots to another orphan or biomarker story (“next-gen precision medicine”).

Market reaction: 40–60 % decline, short covering bounce to $2–$3 before the next raise.

Long-term: Continued dilution and IR spin; share count climbs toward 100 M by 2027.

Thesis: Same playbook, new ticker narrative — dead money for anyone not selling paper.

Bull Case – Temporary Regulatory Pass

Catalyst: EMA grants conditional approval based on cognitive endpoint (low probability <15 %).

Impact: Stock spikes 200–300 % short-term. Company immediately activates ATM/shelf to raise capital, diluting gains within quarters.

Market reaction: Euphoria fades as real-world data fail to reproduce efficacy; margin calls, insider sales, and gravity return.

Thesis: Even a miracle approval just fuels the next raise — the intrinsic value still caps near $8–$10 before reality drags it back under $3.

The Verdict

Anavex isn’t curing Alzheimer’s — it’s curing liquidity problems.

Every press release is a trade setup; every “breakthrough” is an ATM trigger.

They’ve weaponized ambiguity and retail desperation into a decade-long capital extraction model.

The data don’t support the story.

The financials don’t support the valuation.

The governance doesn’t support the trust.

This isn’t innovation — it’s arbitrage.

When the EMA verdict drops, Anavex’s stock will finally reflect what its trials, filings, and lawsuits already do: a company that mastered storytelling but never science.

BMF Reports Final Take

“You'll often find someone's motivation by how they are compensated.”

Price Target: $0.75 (4-month, base-case rejection scenario)

Rating: Strong Sell / Short

Time Horizon: Pre- and post-EMA decision window (Nov–Dec 2025)

Core Risk: Short squeeze on speculative conditional approval (<15 % probability)

The story ends where it always does: dilution, disappointment, and another biotech funeral financed by hope.

BMF Reports — We Don’t Buy Hope. We Short It.

BMF Reports Disclaimer

This report represents opinion, not investment advice. Every statement, chart, citation, and conclusion herein is the result of independent research, public filings, and legally obtained information. We believe our analysis to be accurate at the time of publication, but we make no warranty, express or implied, as to its completeness or accuracy. The views expressed reflect our professional judgment, not any guarantee of outcome.

BMF Reports and its affiliates are short Anavex Life Sciences Corp. (NASDAQ: AVXL) and stand to realize gains in the event its stock price declines. We may add to, reduce, or exit those positions at any time without notice.

This report is for informational and educational purposes only. It should not be construed as an offer to buy or sell securities. All readers are encouraged to perform their own due diligence and consult qualified financial, legal, and tax professionals before making investment decisions.

The information contained herein is derived from sources believed to be public and reliable. Any errors are unintentional. All opinions are subject to change as new information emerges.

We are not compensated by any third party for producing or publishing this report. We receive no payment, direct or indirect, from any hedge fund, issuer, or competitor referenced.

BMF Reports publishes research that challenges hype, fraud, or overvaluation. Our loyalty is to truth, not consensus. The companies we investigate often threaten legal action. We don’t care. Facts are a defense.

By reading this report, you agree that BMF Reports, its affiliates, and its contributors shall not be liable for any loss, damage, or expense arising directly or indirectly from your reliance on the information contained herein.

We reserve the right to update, amend, or withdraw this report at any time.

In plain English:

We dig. We expose. We short. We disclose.

If that makes you uncomfortable, you’re probably long.