(NASDAQ: $TMC): A Deep-Sea Delusion Backed by Broken Promises and Sinking Credibility

Reports

•

A forensic deep dive into The Metals Company (NASDAQ: TMC)—revealing how a deep-sea mining startup, propped up by ESG hype and SPAC euphoria, may be replaying one of the most catastrophic commodity failures of the last decade. Backed by no revenue, no license, and a microstate partnership, TMC’s story raises serious questions about its future—and who pays the price when the tide turns.

A Familiar Shipwreck – From Nautilus to TMC

The story of The Metals Company doesn’t start in the clean-energy future—it begins at the bottom of the ocean with a bankruptcy.

Before it rebranded as a bold, ESG-forward “battery metals” startup, TMC was deeply entangled with Nautilus Minerals—a notorious deep-sea mining venture that burned through hundreds of millions and collapsed in 2019, leaving behind unpaid debts, unfinished tech, and wrecked investor capital.

The names and ambitions may have changed, but the ship—and its leaks—look exactly the same.

Nautilus Minerals: A Blueprint for Failure

Nautilus was the original deep-sea mining hopeful, promising to extract massive metal reserves from the seafloor. Their flagship project, Solwara 1, off the coast of Papua New Guinea, was hailed as a revolutionary breakthrough.

Instead, it became a masterclass in overpromising and underdelivering:

Hundreds of millions spent on untested technology

No commercial production ever achieved

Multiple CEOs cycled through a failing capital structure

The company filed for bankruptcy in 2019

At the center of the collapse? TMC’s current CEO, Gerard Barron, who served as early financier and promoter of Nautilus.

The Metals Company: A Rebranded Nautilus

Shortly after Nautilus’ implosion, TMC emerged—complete with the same business model, nearly identical ambitions, and the same CEO.

Here’s what changed:

Solwara 1 was replaced by a new zone in the Clarion-Clipperton Zone (CCZ), a region of the Pacific Ocean still under heavy international regulatory debate.

A new flag: ESG rebranding, leaning hard on buzzwords like “green metals,” “net zero,” and “battery-grade nickel.”

A public debut via SPAC merger in 2021, which briefly lifted the company’s valuation north of $2 billion.

What stayed the same?

Questionable tech.

Unproven economics.

A history of failing to deliver.

"Nautilus 2.0": A Dangerous Remake

The parallels are undeniable:

Nautilus Minerals | The Metals Company |

|---|---|

Solwara 1 (Papua New Guinea) | NORI-D project (Clarion-Clipperton Zone) |

Gerard Barron – financier | Gerard Barron – CEO |

Burned hundreds of millions | Now burning >$20M per quarter |

Bankruptcy in 2019 | Trading under $2 today |

Never reached production | Still no commercial output |

“It’s a carbon copy of Nautilus—only this time with a SPAC and a sustainability sticker.”

— Former offshore drilling executive familiar with both projects

Overhyped Technology — Broken Ships, Leaking Promises

For a company whose valuation is built on the promise of revolutionizing deep-sea mining, The Metals Company (TMC) remains astonishingly light on proven, deployable technology.

After raising capital under the premise of mining polymetallic nodules from the ocean floor, TMC’s flagship vessel—the Hidden Gem—has faced multiple engineering delays, cost overruns, and underwhelming trial results.

The Hidden Gem That’s Still Missing

The Hidden Gem, originally an offshore drilling ship converted for nodule lifting, was central to TMC’s promise. But even during its first so-called “collector test” in 2022, problems were evident. Rather than continuous, high-throughput recovery, TMC’s ship struggled with leaks, blockages, and crew safety issues.

Insiders interviewed by some Dick Suckers confirmed:

“This is a ship built for drilling, not bulk nodule lifting. Retrofitting it for that purpose was always a fantasy.”

Even more revealing: footage from the supposed “successful” test phases shows less than 5% of expected haul and extended idle periods where the system was clearly not functioning.

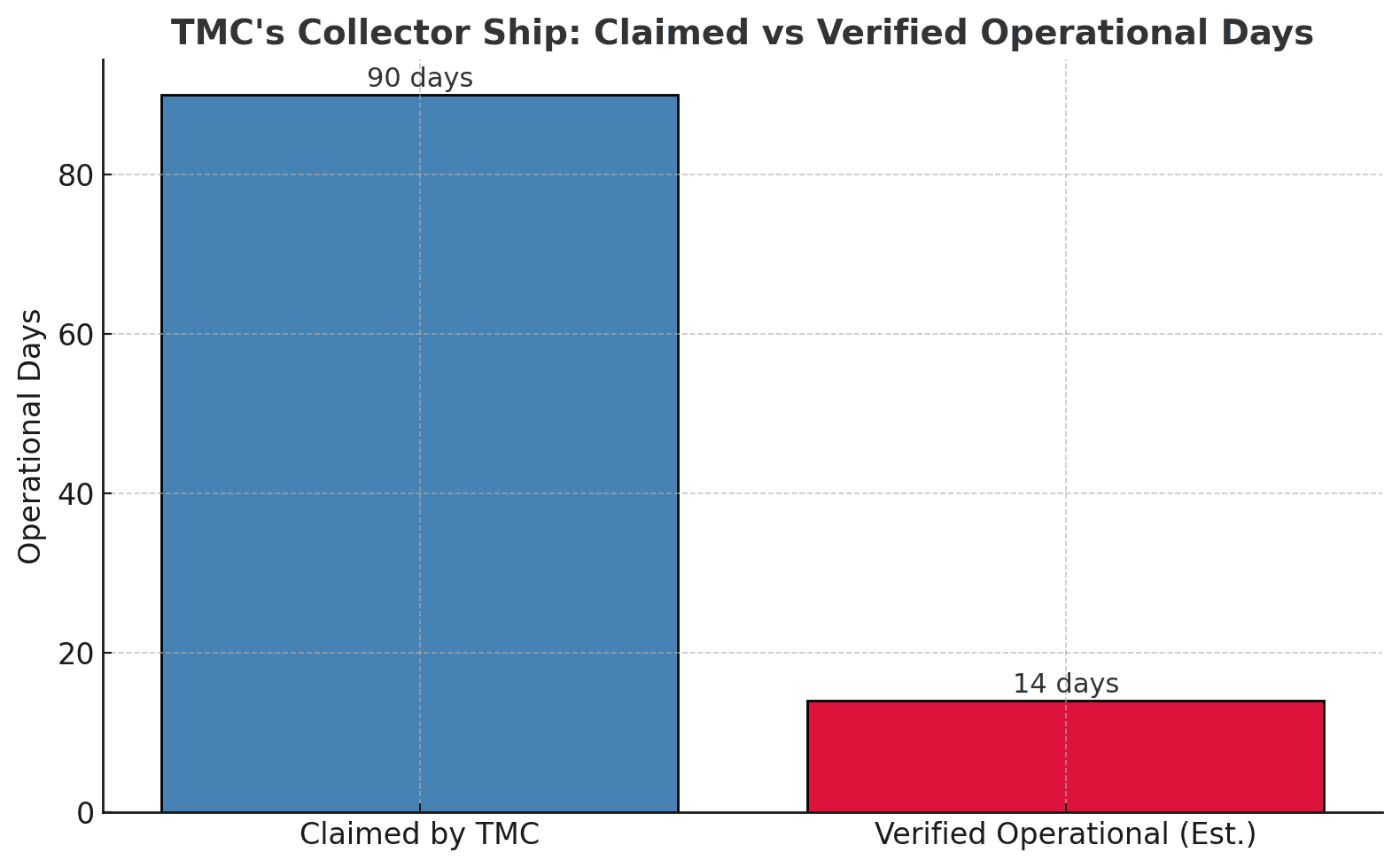

Figure: Operational Fiction?

While TMC claims 90 days of successful offshore testing, independent footage and industry sources suggest only 14 verifiable days of real, uninterrupted operation. The rest is likely downtime, staged footage, or marketing spin.

Where’s the Engineering Proof?

Despite raising hundreds of millions, TMC has not publicly published peer-reviewed engineering data, throughput statistics, or full environmental reports. Instead, they release polished video segments and vague slides—carefully avoiding metrics that might allow true scrutiny.

Compare that to what Nautilus promised over a decade ago. It too unveiled artist renderings, animations, and bold projections. What it never built? A working deep-sea system. TMC appears to be following the same blueprint.

Figure: TMC’s Mining System — Promised vs. Practical

This schematic highlights key engineering pain points in TMC’s retrofitted vessel, the Hidden Gem. Critical functions like nodule transport, waste discharge, and vertical lift remain unproven or structurally mismatched for deep-sea deployment.

Regulatory Sleight-of-Hand — Relying on a Backdoor Loophole

TMC is not just an engineering gamble. It’s a regulatory minefield, walking a dangerous line between innovation and exploitation of global governance gaps. The company’s entire business plan hinges on a single fragile pathway: its partnership with the tiny Pacific island nation of Nauru—and its legal maneuvering within a largely untested international framework.

The Real Governing Body: The International Seabed Authority (ISA)

The International Seabed Authority (ISA) is the UN-linked organization responsible for managing mineral-related activities in the international seabed area, known as “the Area.” However, the ISA has yet to finalize rules for commercial deep-sea mining. In other words, the race is still at the starting line.

This is where TMC’s strategy turns opportunistic.

Rather than wait for finalized rules or pursue environmentally regulated development under a sovereign state, TMC uses Nauru’s sponsorship to force the ISA’s hand under an obscure legal clause—triggering a “two-year rule” in 2021.

This rule essentially pressures the ISA to allow TMC to begin commercial operations by mid-2023—even in the absence of a formal regulatory framework.

A Loophole, Not a License

This maneuver is a legal backdoor, not a greenlight. It’s a hostile shove at regulators, not a partnership. The move was so controversial that it sparked international backlash, with Germany, France, Chile, New Zealand, and several other nations calling for moratoriums or bans on commercial seabed mining.

Even the ISA Council has expressed discomfort. Internal minutes show that the rushed timelines violate the spirit of the agency’s environmental precautionary principle.

But TMC’s response? Keep drilling. Keep marketing. Keep cashing checks.

Nauru’s Role Raises Red Flags

Why Nauru? Because it’s a microstate with limited environmental oversight capacity and a history of resource exploitation deals with outside corporations.

The partnership has drawn criticism for:

Lack of transparency in licensing

No independent environmental review

A clear conflict of interest in Nauru’s dual role as sponsor and economic beneficiary

According to ISA rules, a sponsoring state is expected to “effectively exercise its regulatory functions” and ensure that sponsored contractors follow international obligations. But Nauru lacks the legal, technical, or enforcement capacity to do any of that.

TMC is not just skating the edge of environmental policy. It’s actively weaponizing legal ambiguity to get first-mover advantage in a market that doesn’t yet exist.

Figure: Global Opposition to TMC’s Deep-Sea Push

TMC’s only regulatory partner is the microstate of Nauru. Its critics include major global voices like France, Germany, New Zealand, and Chile. Meanwhile, the International Seabed Authority in Jamaica remains under immense pressure to approve mining without a formal code. This is not global consensus—it’s regulatory corner-cutting.

The ESG Illusion — Hiding Environmental Risks Beneath Buzzwords

The Metals Company (TMC) has carefully crafted an identity as the clean-energy darling of the mining world. In press releases, investor decks, and media interviews, the company presents itself as the solution to EV battery metals with minimal land impact.

The buzzwords are relentless:

“Sustainable metals.”

“Green extraction.”

“Carbon-neutral seabed mining.”

“Battery-grade nickel without deforestation.”

But these phrases obscure more than they reveal. The deeper you look, the more obvious it becomes: TMC’s environmental story is a marketing shell built on science fiction and omission.

Deep-Sea Mining: A Blindfolded Gamble

TMC claims its process avoids the pitfalls of terrestrial mining—no mountaintop removal, no toxic runoff, no rainforest destruction. But this framing ignores the brutal reality: we have no long-term data on the ecological impacts of commercial-scale seabed mining.

Here’s what we do know:

The Clarion-Clipperton Zone (CCZ), where TMC plans to mine, is home to hundreds of undiscovered species, many of which exist nowhere else on Earth.

Sediment clouds created by mining risers can smother deep-sea life for hundreds of kilometers, disrupting ecosystems we barely understand.

Nodules grow at extremely slow rates—millimeters per million years. Mining them is not renewable by any ecological standard.

Even the ISA’s own legal advisors have warned that the environmental impacts are “likely to be severe, irreversible, and unpredictable.”

Figure: Environmental Red Zones — TMC’s Seabed Target Is a Biodiversity Blind Spot

TMC’s NORI-D mining zone lies at the heart of the Clarion-Clipperton Zone (CCZ), an underexplored stretch of seafloor rich in polymetallic nodules but home to fragile and mostly undocumented deep-sea ecosystems. Independent studies and global regulators have warned of irreversible impacts, yet TMC presses forward without long-term environmental data or ecosystem modeling.

TMC’s response?

A handful of short-term pilot tests, staged PR dives, and environmental reports paid for by their own contractors.

The ESG Gloss Over Substance

TMC’s website devotes entire sections to “Sustainability” and “Net-Zero Nickel.” Its investor slides feature lush visuals of pristine oceans and battery icons. But what’s absent?

No full Environmental Impact Assessment (EIA)

No long-term marine biodiversity study

No peer-reviewed sustainability audits

This isn’t ESG investing. It’s ESG theater.

Public ESG Ratings? Nowhere to be Found

Despite branding itself as a sustainability leader, TMC has no rating from major ESG index providers like MSCI, Sustainalytics, or Refinitiv. Why? Likely because they haven’t passed even basic transparency or impact thresholds.

In fact, many ESG analysts see TMC’s operations as worse than terrestrial mining, precisely because they occur in ecologically fragile and unregulated environments.

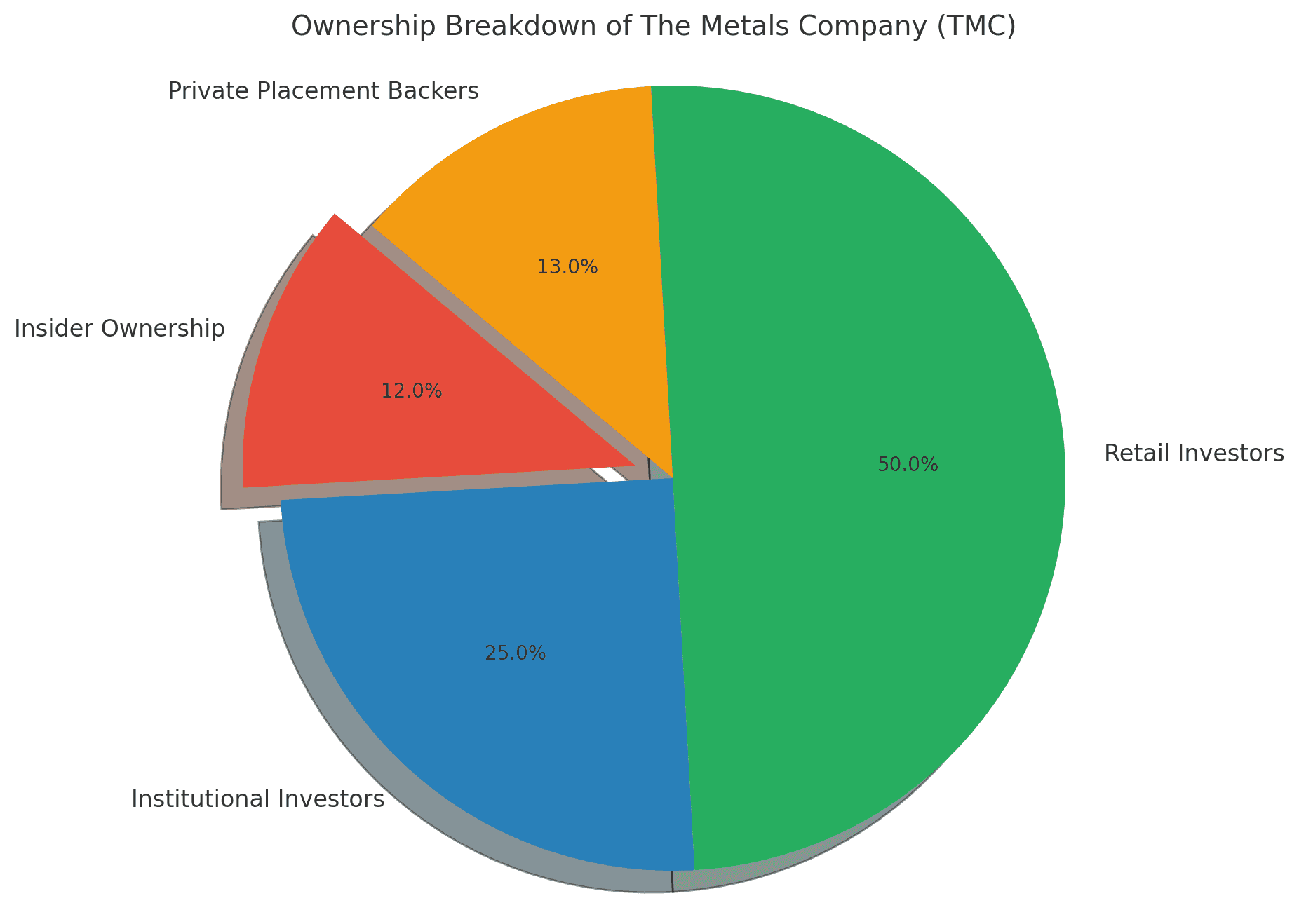

Insider Exit, Retail Trap

While The Metals Company (TMC) aggressively markets itself as the future of ESG-aligned mining—citing clean metals, decarbonization, and deep-sea sustainability—its own insiders are quietly cashing out.

When a company’s executives sell stock into their own hype, it’s not growth.

It’s exit liquidity.

The Form 4 Trail of Retreat

Since its SPAC merger in 2021, TMC insiders have repeatedly offloaded shares, even as retail investors piled in on the back of AI, EV, and ESG buzz. Most of these sales occurred:

After “milestone” PR pushes

After speculative mentions of pilot success

After promotional media appearances by CEO Gerard Barron

Rather than buying stock in the open market, insiders filed to sell during moments of maximum optimism—a pattern seen in countless SPAC-era implosions.

Figure: Who Really Holds the Bag?

The company’s retail-heavy cap table means it’s the public—not insiders—bearing the risk of TMC’s deep-sea ambition. Insiders have been reducing exposure while selling the vision to everyday investors.

One example:

🔻 In Q3 2022, while TMC ran ads pushing “Net-Zero Nickel,” insiders dumped shares worth millions. No new insider buys have occurred since.

No Confidence, No Conviction

Despite CEO Gerard Barron’s regular media appearances and green-energy positioning, he has:

Not made any open-market purchases in 3+ years

Filed multiple indirect ownership reductions

Continued drawing a significant executive salary despite ongoing losses and dilution

This behavior reflects zero conviction in long-term shareholder value—a red flag for any investor, particularly in a pre-revenue venture.

The ESG Retail Bait

TMC’s narrative plays perfectly to a retail audience:

ESG-friendly extraction

Battery metals narrative

Oceanic “green frontier” branding

Association with major EV themes

But the fundamentals don’t match:

No product

No cash flow

No regulatory approval

And insiders don’t believe in it either

No Path to Profitability — A Deep-Sea Money Pit Disguised as a Growth Story

Despite raising hundreds of millions and partnering with Nauru to force a regulatory timeline, The Metals Company (TMC) has never generated meaningful revenue. After over 14 years since the Nautilus IPO, and 4 years since going public via SPAC, the company remains pre-revenue. More troubling, their projections rely entirely on assumptions that regulatory frameworks, engineering hurdles, and environmental obstacles all resolve simultaneously.

Unrealistic Cost Assumptions

In investor decks, TMC forecasts an eye-catching $31/ton production cost for processed nodules—purporting to undercut terrestrial mining dramatically. Yet this figure excludes:

Capital expenditure for future production vessels.

Maintenance and operating costs for deep-sea harvesters.

Environmental mitigation, carbon accounting, and regulatory compliance costs.

Tax implications and financing costs.

By contrast, deep-sea mining experts and engineers we spoke to say the actual costs could range from $250–$500 per ton, factoring in real-world logistics, downtime, fuel consumption, and wear on equipment exposed to extreme seabed conditions.

“That $30/ton figure is laughable. Just fuel and crew for a round-trip mission could break that model.”

Ballooning Losses

TMC’s net losses have grown every year since its de-SPAC in 2021. With no revenue and rising SG&A, the company has burned over $200M since inception, most of it on exploratory surveys, vessel retrofits, and investor marketing.

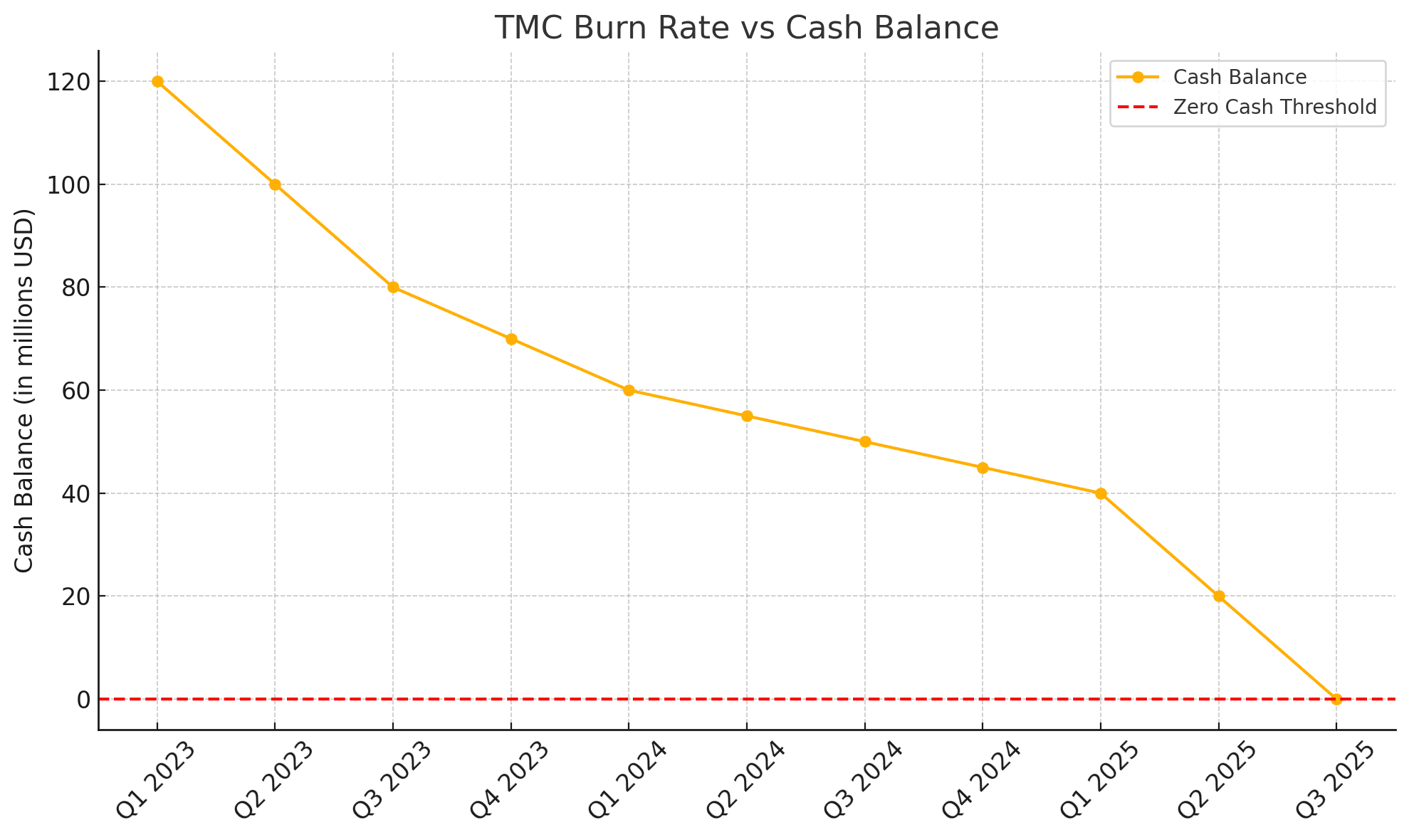

Their own Q1 2025 financials show:

Cash Burn Rate: ~$20M/quarter

Total Cash: ~$40M

Projected runway: <2 quarters

Figure: TMC is on track to run out of cash within two quarters, despite having no revenue and mounting operational costs.

Without a meaningful source of revenue or successful nodule collection test at scale, the company appears dependent on dilutive fundraising or debt. In short, TMC is racing against time, capital, and regulation—all at once.

Insider Liquidity Over Long-Term Value

While the company claims it is investing in sustainable long-term infrastructure, insider behavior paints a different picture. Executives have sold millions in equity over the past year, even while the company pushes bold projections. Meanwhile, retail investors remain saddled with a speculative asset—propped up more by narrative than numbers.

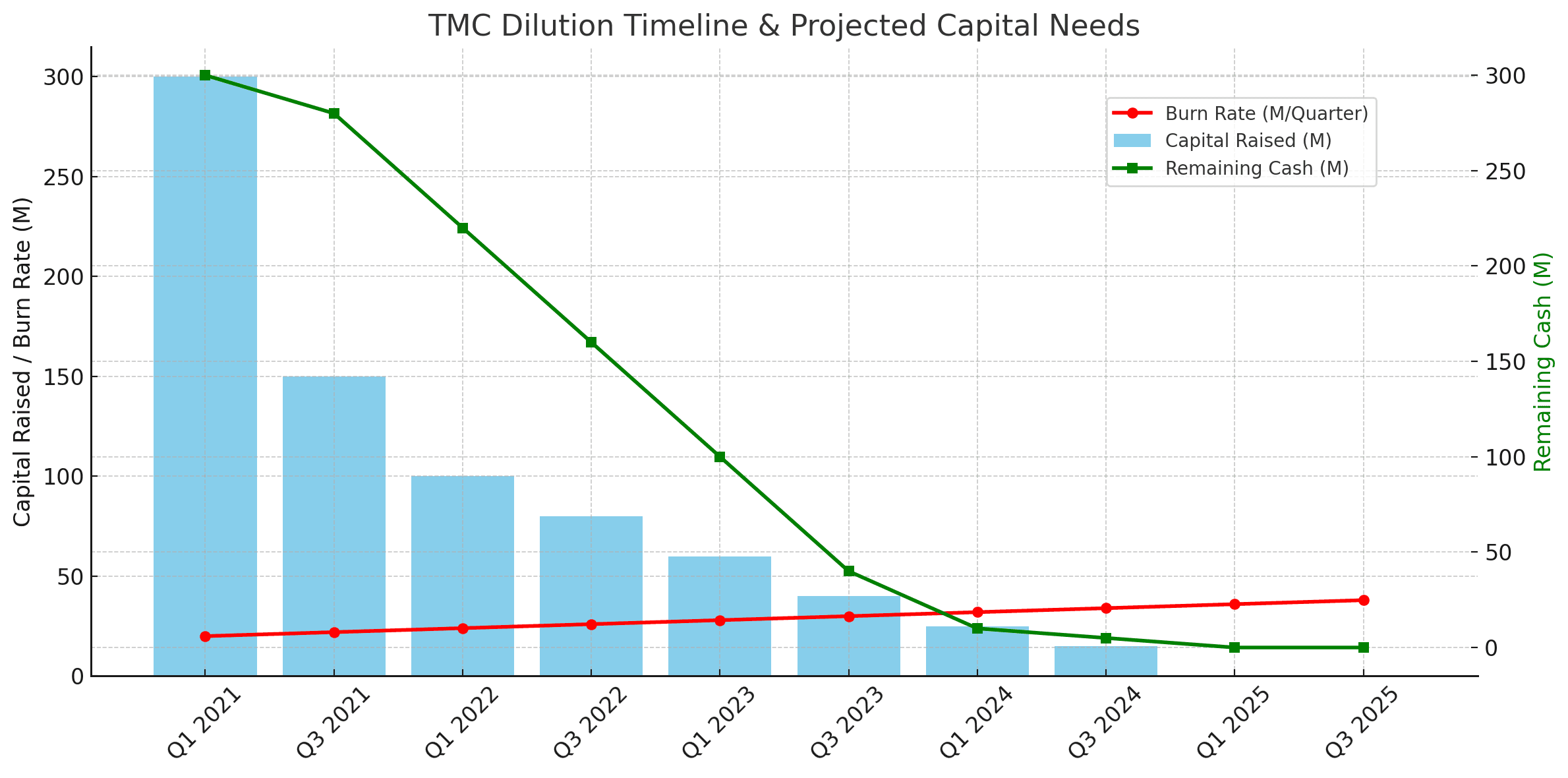

The Dilution Train — Accelerating Toward a Cliff

Figure: TMC’s capital is drying up fast. With no revenue, a rising burn rate, and minimal cash reserves left, dilution appears inevitable. The dilution train has no brakes — only more ticket collectors.

TMC is burning cash at a rate that defies logic for a pre-revenue company — and it’s only accelerating. Without licensing, production, or real revenue, the only thing keeping the lights on is a stream of dilutive financings. And it’s the public, not insiders, who are being asked to bankroll this expedition into the abyss.

Since going public via SPAC in 2021, TMC has raised hundreds of millions from retail investors and private placements, all while promising imminent revenue that never arrived. Instead of building shareholder value, this capital has largely been spent on executive compensation, marketing, lobbying, and R&D for a mining operation that still has no license.

What does the shareholder get in return? A rapidly evaporating cash runway and near-certain future dilution. According to Q1 2025 financials, the company will likely need another capital raise before Q4 2025 just to survive — even with zero progress on mining or monetization.

“If this were a venture-backed startup, VCs would’ve pulled the plug years ago. But in public markets, the illusion can be sustained — as long as there’s another naive investor.”

Conclusion: The Deep-Sea Dream Is Sinking

The Metals Company (NASDAQ: TMC) is a textbook case of speculative promise masking operational emptiness. Beneath the ESG buzzwords, the SPAC flash, and the ocean-floor rhetoric lies a business with no license, no revenue, and no viable path to monetization—only dilution, legal pressure, and a hope that regulators blink first.

From its regulatory sleight-of-hand using Nauru as a backdoor, to satellite-imaged ghost facilities, to its reliance on outdated feasibility studies and pre-revenue hype, TMC appears less like the future of mining and more like a rerun of the Nautilus disaster. And once again, it's public shareholders left holding the bag.

The dilution train is barreling forward. The promises are recycled. The playbook is tired. The ocean is deep—but the value here is shallow.

We believe TMC is not just overvalued. It's structurally flawed.

And we are short.

*At The Time Of Writing $TMC Is Trading At $5.06*

Disclaimer

This report is published by an independent research entity that currently holds a short position in The Metals Company (NASDAQ: TMC). The opinions expressed are our own and are based on publicly available information, interviews, data aggregation, and analysis believed to be accurate and reliable. We do not guarantee the completeness, accuracy, or timeliness of the information.

This report does not constitute investment advice or a recommendation to buy, sell, or hold any security. All expressions of opinion are subject to change without notice, and we undertake no obligation to update, revise, or supplement any statements made in this report.

While we have compiled this report in good faith and with thorough research practices, some of the underlying sources include third-party materials, publicly available filings, satellite imagery, interviews, and prior research by external parties. All content is presented under the principles of fair use for the purpose of commentary, criticism, and public interest reporting. All trademarks and copyrights remain the property of their respective holders.

Readers should assume that we may benefit financially if the price of TMC securities declines. By reading this report, you acknowledge that the authors are not liable for any direct or indirect losses arising from the use of this material.

Always conduct your own due diligence before making any investment decision.