Connexa Sports Technologies ($YYAI) is no turnaround story—it’s a penny-stock dilution scam dressed up in AI buzzwords. From tennis toys to pickleball pivots to a matchmaking algorithm shell, the company is broke, auditor-tainted, governance-free, and one financing away from collapse.

Connexa Sports Technologies ($YYAI) isn’t a turnaround—it’s a textbook penny-stock hustle masquerading as a Nasdaq tech play. The company has morphed from one failed gimmick to the next, cycling through buzzwords like a serial grifter: first it was tennis ball launchers, then pickleball accessories, then “connected sports hardware,” and now it’s supposedly an AI matchmaking platform.

Strip away the press releases and what you’re left with is ugly:

Cash at FY2025 year-end? $54,000. That’s what a Manhattan divorce lawyer bills in two weeks.

Liquidity? Management openly admits cash + receivables “will not” cover the next 12 months. Translation: insolvency risk is staring them down.

Governance? A one-man fiefdom. Majority shareholder Hongyu Zhou owns ~56%, stuffed the board with his people, and within months lost Nasdaq compliance when one director quit.

Auditors? Until late 2024, Connexa’s books were signed by Olayinka Oyebola & Co.—the same outfit the SEC is trying to permanently ban for enabling a multi-hundred-million-dollar fraud at Tingo.

Legacy business? Their once-touted Slinger Bag “connected sports” gadget was sold for one dollar. That’s the liquidation value management put on its old dream.

Behind the shiny new “AI licensing” story is a company bleeding cash, reliant on dilution and controlled by a single shareholder. One more Nasdaq notice, one failed financing, and this thing implodes.

From Pickleball to “AI Love Tech” – The Scam Evolution

Connexa’s history reads like a roadmap of desperation.

Stage 1: The Tennis Toy Hustle. They entered the market as Slinger Bag, flogging a portable tennis ball launcher. It was pitched as “connected sports hardware” but was basically a glorified ball machine. Investors bought into the sports-tech hype, but sales never scaled.

Stage 2: Pickleball Pivot. When tennis buzz fizzled, management latched onto pickleball—the fastest-growing sport in America—as their next gimmick. They rebranded as Connexa Sports and positioned themselves as a “pickleball play.” It didn’t work.

Stage 3: The Fire Sale. By 2024, the company was out of cash. The Slinger Bag business—the core of its identity—was sold for one dollar. You read that right. The entire pickleball/tennis dream was worth less than a Chipotle burrito.

Stage 4: The AI Fantasy. Enter Hongyu Zhou, who “rescued” Connexa by injecting a Chinese matchmaking and dating algorithm company (YYEM). Suddenly Connexa pivoted from sports gear to AI licensing and dating platforms. The same Nasdaq ticker that once sold pickleball accessories is now pitching itself as a “leader in AI matchmaking.”

FIGURE: Slinger Bag product image. Once touted as Connexa’s flagship “connected sports hardware” innovation, the Slinger portable tennis ball launcher was sold in 2024 for just one dollar, exposing the collapse of its original business model.

It’s the corporate equivalent of a Tinder bio that says “entrepreneur” after three failed MLMs. A pivot this absurd is not strategy—it’s survival. And the market knows it.

Financial Forensics – The Numbers Don’t Lie

Connexa’s press releases spin a story of “explosive growth.” The filings tell a very different story: a company living paycheck to paycheck, masking insolvency with paper profits and dilutive financing.

The Headline Numbers (FY2024 → FY2025)

Revenue: $5.2M → $12.8M.

Sounds impressive—until you realize it’s almost entirely “licensing revenue” from a newly folded-in Chinese matchmaking asset with 90-day payment terms. On paper, it’s growth. In reality, it’s IOUs.Gross Profit: $4.0M → $9.8M.

Nice margins—if only they could collect.Operating Income: $3.9M → $6.6M.

But wait: operating cash flow was negative $379,000. Profits that can’t be turned into cash are just accounting smoke.Net Income (controlling interest): $2.6M → $3.5M.

Again, only real if the receivables show up.Cash on hand: $39k → $54k.

Yes, they “doubled” cash. No, $54k isn’t a war chest—it’s a joke. This is what a Midtown partner at Skadden bills before lunch.

Receivables Balloon – A $10M House of Cards

FIGURE: Connexa Sports Technologies – Cash Flow Statement (FY2025). Despite reporting $4.6M in net income, operating cash flow was negative ($379,384), driven by a ballooning $12.1M increase in receivables. This stark mismatch highlights that Connexa’s “profits” are built on IOUs, not cash in the bank.

The “growth” story hinges on $10M of receivables booked in FY2025. Connexa gave licensees 90 days to pay—but by year-end, the cash hadn’t arrived. The result? Revenue recognition without revenue reality. Management itself admits that available cash + expected inflows will not cover the next 12 months. That is corporate code for: we’re broke.

Dilution as a Lifeline

Like every penny-stock scam, Connexa’s solution isn’t execution—it’s dilution.

In June 2025, Connexa announced a $4.6M private placement (20M units at $0.23, warrants at $0.89). The deal hasn’t closed—it depends on Nasdaq compliance and shareholder approval.

They also filed for an ATM offering (~$2.2M) to dump stock into the open market.

Reverse splits (June 2024, again in August 2025) are the duct tape keeping the Nasdaq ticker alive.

The pattern is obvious: cash comes not from customers but from shareholders. Investors are the product, not the market.

Slinger Bag Fire Sale – Proof of Value

Let’s not forget: the original “connected sports” business was pawned off for $1. That’s management’s own verdict on the company’s past decade of hype. If history is any guide, Connexa’s AI dating fantasy will end the same way.

Governance & Auditors – No Adults in the Room

If you wanted to design a corporate structure to destroy investor trust, you’d build Connexa Sports Technologies. Let’s break it down.

A One-Man Fiefdom

Connexa is a “controlled company” under Nasdaq rules. Translation: majority shareholder Hongyu Zhou owns ~56% of the stock and calls every shot. He installed his own board in November 2024, and within six months they already lost compliance when a single director walked out.

This isn’t a board—it’s a rubber stamp. Minority investors don’t have governance rights; they’re along for the dilution ride.

Auditor Shopping Amid Scandal

Until October 2024, Connexa’s financials were signed off by Olayinka Oyebola & Co.—a no-name firm the SEC later charged with aiding and abetting one of the biggest accounting frauds of the decade (Tingo). The SEC is seeking to permanently bar Oyebola and his firm from auditing public companies.

When that bombshell dropped, Connexa quietly fired Olayinka and hired Bush & Associates. Three months later, they dumped Bush too and brought in Enrome LLP to finish the FY2025 audit. That’s two auditor swaps in six months.

Auditor roulette is the hallmark of penny stock frauds. No credible mid-tier firm will touch them.

Going Concern Warnings – Again and Again

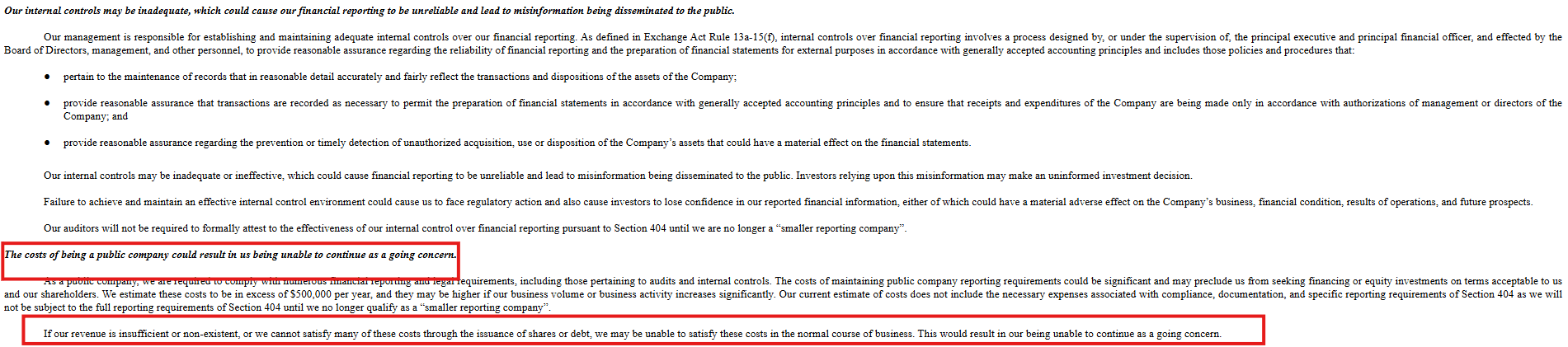

FIGURE: Excerpt from the company’s risk disclosures highlighting severe financial instability and inadequate internal controls. The section warns that the company’s financial reporting may be unreliable and subject to misinformation, creating potential legal and regulatory risks. Additionally, it underscores that the high costs of maintaining public company status—estimated at over $500,000 annually—pose a material threat to operations. The disclosure explicitly states that insufficient or non-existent revenue could prevent the company from covering these expenses, resulting in its inability to continue as a going concern.

Even before the “AI pivot,” Connexa’s audits came with going concern warnings. That language didn’t disappear just because they stapled a matchmaking algorithm onto the cap table. It’s still there, buried in the filings, screaming that the company might not survive 12 months without new capital.

The Optics Problem

It’s hard to overstate how bad this looks:

A board with no independence.

A CEO whose salary doubles as a convertible loan.

A chairman funding company bills out of his own pocket.

An auditor caught red-handed enabling fraud in other clients.

This isn’t corporate governance—it’s corporate cosplay.

Insolvency & Delisting Risk – They’re Fucking Broke

Let’s stop sugarcoating it: Connexa is broke. Not “tight on cash,” not “managing liquidity”—flat-out broke.

Cash balance at FY2025 year-end: $54,000. That’s the total. A Nasdaq-listed “AI company” with global ambitions has less cash than the average wedding budget in Scottsdale.

Operating cash flow in FY2025: negative. They lost money on operations even while reporting “profits.” That means the income statement is a fairy tale; the cash flow statement is reality.

Payables and obligations: They still owe their new chairman (Hongyu Zhou) hundreds of thousands he fronted to keep the lights on. The CEO literally converted his unpaid salary into a loan. This isn’t growth capital—it’s survival handouts.

FIGURE: Connexa Sports Technologies – Balance Sheet (FY2025). Year-end cash stood at a paltry $54,744, up only slightly from $39,351 in FY2024. For a Nasdaq-listed “AI company,” this balance represents near-insolvency and validates management’s own admission that liquidity “will not” cover 12 months of operations.

And here’s the brutal truth: it’s very fucking hard to run a business with no fucking money. You can’t pay engineers with receivables, you can’t fund marketing with “licensing revenue due in 90 days,” and you sure as hell can’t keep Nasdaq happy with $54k in the bank.

Dilution or Death

Connexa’s only path forward is selling stock. They lined up:

A $4.6M private placement (20M units at $0.23).

A $2.2M ATM program to dribble shares into the market.

Both are contingent. Both are dilutive. Neither solves the structural problem: there is no cash engine here. Without constant infusions, the company is one payroll cycle away from default.

Nasdaq’s Patience Is Wearing Thin

Connexa has already burned two lifelines:

A reverse split in June 2024 to get back above $1.

Another reverse split in August 2025.

It still got slapped with compliance notices—first for board independence, then for late filings. One more tripwire, and Nasdaq will boot them to the pink sheets. At that point, equity financing dries up, and bankruptcy becomes the only option.

Governance & Auditors – The African Auditors with Blood on Their Hands

Shady Auditors with a Massive Fraud Stain

Connexa’s financials from FY2023 and FY2024 were signed off by Olayinka Oyebola & Co., a Lagos-based chartered accounting firm. Stay with me—this is not a reassuring audit background.

In September 2024, the U.S. SEC charged Olayinka Oyebola and his firm with aiding and abetting a massive, multiyear securities fraud carried out by Dozy Mmobuosi and the Tingo group. The allegations are brutal: Oyebola’s firm knowingly signed off on fake audit reports and helped conceal falsified financials.

FIGURE: Screenshot showing the engagement of a little-known audit firm based in Africa. The auditor lacks a verifiable track record with U.S.-listed companies, raising serious concerns about independence, competence, and regulatory oversight. The reliance on obscure offshore auditors is a recurring red flag seen in fraudulent overseas listings.

By August 2025, a U.S. federal court finalized judgments:

A combined $200,000 fine ($100K each individual and firm),

Permanent ban from auditing U.S. public companies,

A six-year suspension from appearing before the SEC as accountants.

Connexa quietly fired Oyebola in October 2024, only to hop auditors again three months later. That’s two swaps in six months—classic audit roulette territory.

Why This Matters — Connect the Dots

Gatekeeper failure: Auditors are meant to safeguard financial truth. These guys failed so badly, they were complicit in a fraud worth hundreds of millions.

Credibility crisis: If Oyebola’s work is now tainted, Connexa may be forced to restate prior audits—or risk delisting if filings remain suspect.

Reputation and risk: Swapping to new auditors doesn’t erase the trust gap. Investors should assume the entire FY2023–24 reporting suite is suspect.

The Scam in Plain English

Connexa isn’t building a business—it’s buying time.

Time through receivables that may or may not get collected.

Time through insider bailouts and unpaid salaries.

Time through dumping shares on retail.

But time runs out. And when it does, the stock follows the legacy Slinger Bag business into the dustbin—sold for a dollar, if it’s lucky.

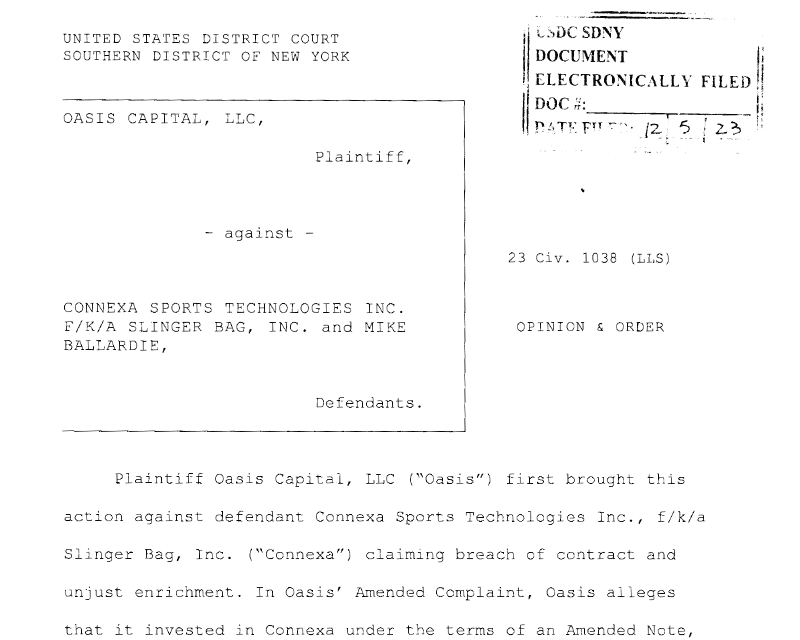

Legal Luggage – The Oasis Capital Lawsuit

If Connexa’s governance and financials weren’t enough, its legal history seals the deal: this company has already been accused of defrauding its own financiers.

In 2023, Oasis Capital LLC sued Connexa (then still trading on the Slinger Bag story) and its CEO Mike Ballardie. The lawsuit alleged:

Oasis put up $600,000 in a convertible note.

When Connexa uplisted to Nasdaq, Oasis claimed the company illegally converted the note to equity and stiffed them on the cash repayment.

Worse, Oasis alleged CEO Ballardie fed them material non-public information (MNPI) that prevented Oasis from selling shares—classic Rule 10b-5 securities fraud territory.

The case went to federal court in New York. Connexa tried to get it thrown out. The judge disagreed—allowing the securities fraud claims to proceed into late 2023. That’s important: the court believed the allegations had merit.

FIGURE: Oasis Capital LLC v. Connexa Sports Technologies Inc. – A federal lawsuit filed in the Southern District of New York alleging breach of contract and unjust enrichment. This case underscores Connexa’s long track record of financial disputes with its own financiers, raising red flags on governance and trustworthiness.

By March 2024, the case quietly disappeared—likely settled or dismissed on undisclosed terms. Connexa never came clean with investors about how it ended. But the signal is clear:

When your own lender sues you for securities fraud, you’ve already crossed the line from “mismanaged” into “untrustworthy.”

This wasn’t a frivolous lawsuit. It was a major financing partner accusing management of deception. That stain doesn’t vanish just because they pivoted from pickleball to AI dating apps.

Why This Matters Today

The Oasis saga shows a pattern: Connexa raises capital, misleads counterparties, then pivots and leaves the wreckage behind. Investors should assume that today’s “AI licensing” narrative will end the same way—with shareholders holding the bag.

Phantom Growth via Receivables – The Mirage Behind the Numbers

Connexa’s supposed revenue surge in FY2025 is accounting fiction dressed up as growth. On paper, revenue rocketed from $5.2M to $12.8M. In reality, $10M of that is receivables sitting on the books—not cash in the bank.

Why This Is Dangerous

Receivables ≠ Revenue

Connexa recognizes revenue the moment it signs licensing agreements, not when the cash clears. This inflates the income statement, but the balance sheet tells the truth: they haven’t collected.90-Day Terms, Zero Cushion

Management gave licensees 90-day payment windows. That’s standard for big-cap companies with billions in float. For Connexa—sitting on $54,000 in cash—it’s suicide. They cannot survive 90 days without those payments landing.One Bad Actor = Collapse

If a single licensee delays payment → liquidity crisis.

If one defaults → their entire FY2025 “profit” evaporates.

This is the fragility of a business built on paper revenue.

Cash Flow Already Shows the Crack

Despite “profitability,” operating cash flow in FY2025 was negative $379,000. The books say they’re making money. The bank account says otherwise. This mismatch is where fraud allegations are born.

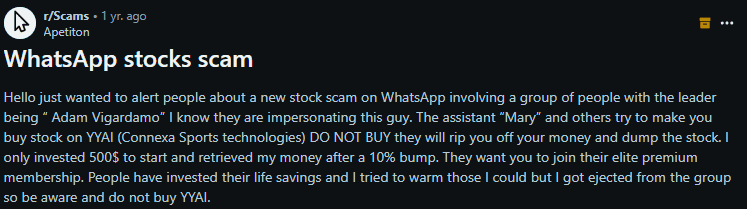

Overseas Manipulation via WhatsApp Pump Groups

In addition to insider malfeasance, Connexa Sports Technologies ($YYAI) has been the subject of coordinated overseas stock manipulation schemes. Evidence from Reddit’s r/Scams documents a WhatsApp stock-pumping group led by impersonators pushing unsuspecting retail investors into buying YYAI under the guise of a “premium membership.” Victims report being urged to invest their life savings, only to be dumped on once the stock was artificially spiked by 10% or more.

This activity fits a broader pattern of overseas boiler-room style operations that target thinly traded microcap securities. Such manipulation artificially inflates liquidity and volume in $YYAI, masking its weak fundamentals and creating exit liquidity for insiders and overseas promoters. The fact that YYAI has become a target for these coordinated scams should raise immediate red flags for regulators and investors alike.

FIGURE: A Reddit post on r/Scams warning of a WhatsApp pump-and-dump group tied to YYAI stock, where organizers encouraged participants to buy shares and join a “premium membership” before dumping the stock on them.

The Short-Seller Tell

Every short fund worth its salt watches the “subsequent events” section in filings. If Connexa discloses that those receivables haven’t been collected—or had to be renegotiated, extended, or written down—it confirms what we already suspect:

The $12.8M headline revenue is a mirage.

Bigger Picture

This isn’t just bad accounting—it’s structural. Connexa doesn’t have a product or recurring revenue. Its only way to show “growth” is to book big contracts, recognize all the revenue upfront, and pray counterparties pay later. That’s not growth. That’s desperation.

Bottom line: Connexa’s FY2025 “profitability” isn’t a turnaround—it’s an illusion built on IOUs. When the checks bounce, so will the stock.

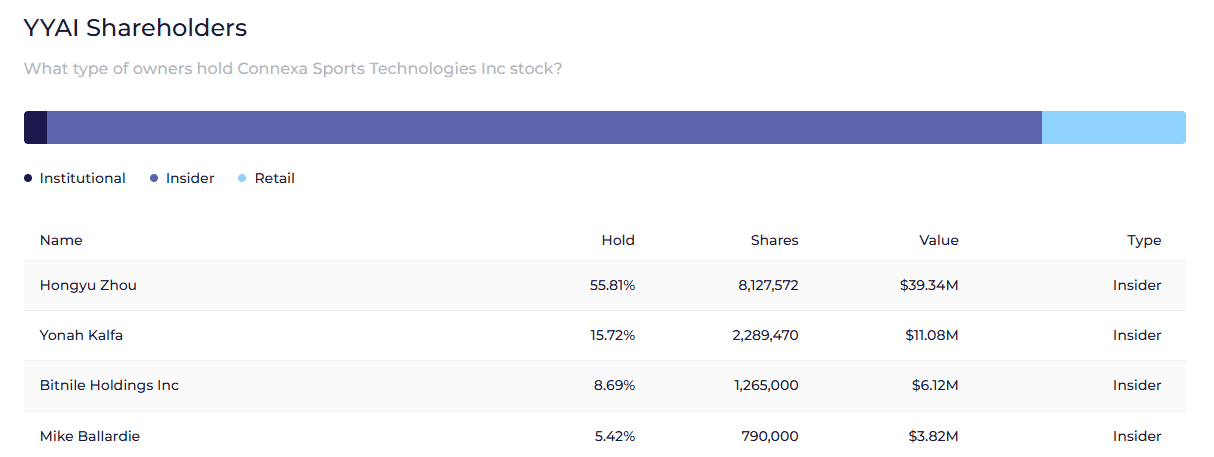

Controlled Company Loophole – Legalized Looting

Connexa isn’t run for shareholders—it’s run for one man: Hongyu Zhou. After the November 2024 “AI pivot,” Zhou walked away with ~56% ownership, instantly classifying Connexa as a “controlled company” under Nasdaq rules.

Here’s why that’s toxic:

No Real Oversight

Being a controlled company means Connexa can legally skip the basics:

No majority independent board.

No independent compensation committee.

No checks on insider transactions.

FIGURE: Connexa Sports Technologies (ticker: YYAI) shareholder breakdown. The chart and table show that ownership is overwhelmingly controlled by insiders, leaving minimal float for retail and institutions. The largest holder is Hongyu Zhou with 55.81% (8.1M shares, $39.34M value), followed by Yonah Kalfa at 15.72% (2.3M shares, $11.08M value). Other major insiders include Bitnile Holdings Inc. (8.69%, 1.27M shares) and Mike Ballardie (5.42%, 790K shares). Together, insiders control over 85% of the company, suggesting extremely limited liquidity and potential susceptibility to manipulation.

That’s not governance—it’s abdication. Zhou doesn’t need to answer to minority shareholders, period.

Total Control of the Dilution Machine

Zhou can—and already has—rammed through dilutive financings and insider-friendly arrangements:

The CEO (his appointee) literally converts his unpaid salary into stock or warrants.

Zhou himself has fronted $700k+ in expenses for Connexa, which he can choose to claw back whenever he likes.

The upcoming $4.6M PIPE at $0.23/share? Zhou holds the majority vote to approve it—and dilute everyone else into irrelevance.

The Rubber-Stamp Board

After Zhou’s takeover, Connexa stacked its board with his own nominees. Within months, one quit—instantly triggering a Nasdaq non-compliance notice for lack of independence. That’s how fragile the façade of governance really is.

The Playbook

This is the classic penny-stock hustle:

Seize majority control.

Opt out of governance.

Bleed minority holders through dilution and insider deals.

Connexa is no exception—it’s the rule. Investors aren’t partners here; they’re exit liquidity.

No Real Product – Just Paper and Hype

Connexa has reinvented itself so many times it’s hard to keep track—tennis gadgets, pickleball pivots, “connected sports,” now AI dating. But through all the noise, one fact remains: they have never built a sustainable product.

The Graveyard of Failed Pivots

Tennis/“Slinger Bag”: Once hyped as a revolutionary portable launcher, sold off for $1. That’s what years of marketing and shareholder money amounted to—pennies on the dollar.

Pickleball Accessories: The “fastest-growing sport” pivot that fizzled out as fast as it arrived. Zero lasting traction.

Connected Sports Platform: Supposed to unify smart sports devices. Never materialized into anything.

The New Shell Game: AI Licensing

Now they’re pitching “AI matchmaking” as the future. Let’s be clear: this is not a product. It’s an algorithm they claim to license.

No app.

No ecosystem.

No proof of adoption.

Instead, they’ve booked “royalty revenue” that hasn’t been collected, and called it growth. Licensing without real deployment is smoke and mirrors.

Why It Matters

Businesses with no product, no moat, and no paying customers have one destiny: dilution and eventual collapse. Connexa isn’t an AI company—it’s a story stock that keeps swapping costumes.

From sports toys to dating algorithms, the through line is the same: hype the buzzword of the day, raise money, dilute shareholders, and walk away when the narrative dies.

Final Short Thesis – The Scam in Plain Sight

Connexa Sports Technologies ($YYAI) is the definition of a penny-stock dilution scam hiding in plain sight. This company has no money, no governance, no product, and no credibility. It’s a corporate chameleon that pivots from tennis toys, to pickleball hype, to AI dating algorithms—not because of vision, but because of desperation.

The numbers tell the real story: $54,000 in cash, negative operating cash flow, and “profits” built entirely on phantom receivables that may never materialize. They’ve sold their legacy business for a dollar, fired auditors caught up in SEC fraud charges, and now rely on reverse splits and PIPE financings to keep the lights on. Governance? Nonexistent. A one-man fiefdom with legal permission to loot shareholders at will.

This isn’t a turnaround. This isn’t innovation. This is a dilution treadmill dressed up as a Nasdaq ticker. When the receivables don’t show, when Nasdaq patience runs out, or when the financing falls apart, it all collapses. And history tells us exactly how this ends: bagholders left broke, insiders walking away, and another penny stock carcass on the pink sheets.

Our view is simple: YYAI is a controlled dilution machine headed for zero.

Legal Disclaimer (BMF Style)

We are short sellers. We are biased. We stand to profit if the price of $YYAI declines. Nothing here is investment advice, and everyone reading should assume we are talking our book—because we are.

All of the information in this report is sourced from public filings, news reports, and third-party sources believed to be reliable, but we make no representation as to accuracy or completeness. If you believe in Connexa’s fairy tale, buy the stock. We’ll be on the other side of that trade.

At BMF Reports, we don’t sell hope—we sell reality. And the reality here is simple: Connexa is fucking broke, auditor-tainted, governance-free, and structurally doomed. Invest at your own risk. We’re short.