BMF Capital Investigates Jet.AI ($JTAI): Forensic Short Report Exposing Dilution, Governance Red Flags, and the Risk Behind the AI Pivot

Jet.AI, Jet Token, pitched “AI-powered” aviation and now touts “AI data centers.” Beneath the branding shifts: gross-up accounting, serial dilution, a cash-hungry capital structure, insider conflicts (including a sponsor-side SPAC), and a business model that keeps changing faster than the balance sheet can keep up. This is a forensic, no-BS look at how this sausage is made.

Why We’re Short

Low-quality revenue: Charter brokerage recorded on a gross basis (not net commissions), inflating the top line while margins hover near zero/negative. Revenue looks big; the economics don’t.

Serial dilution machine: SPAC trust arrived thin → repeated equity/preferred deals → 1-for-225 reverse split → more issuance. Latest S-3 for 1,956,000 shares vs ~3.26M o/s = ~37.5% ownership dilution if placed; share count up ~60%.

Going-concern dependence: Cash burn funded by GEM/Ionic/convertible paper. Every “solution” sells tomorrow’s equity cheaper than yesterday’s.

Conflicted capital allocation: Company cash into management’s SPAC sponsor (AI infrastructure). When runway is short, insider promotes shouldn’t be the priority.

Pivot risk (aviation → AI data centers): Zero track record in a cap-intensive, winner-take-scale market. Hype outpaces capacity (land/power/permits/customers/CapEx).

Financial telltales: Negative equity, outsized “prepaid offering costs,” whipsaw share counts—signals of a structure built to finance narrative, not operations.

Asymmetric path: Near-term catalysts (resale overhangs, deal slippage, cap-raise friction) skew downside for common holders.

In Short:

We are short $JTAI. The numbers don’t lie, the narrative does.

HOW JET.AI MAKES A DOLLAR: GROSSED-UP REVENUE ON THIN MARGINS

FIGURE: CHARTERGPT MARKETING IMAGE

Jet.AI promotes its CharterGPT app as an AI-powered booking tool. The ad shows luxury jet interiors and flight options (e.g., Citation CJ2+ at $13,500). In practice, Jet.AI books third-party flights, records the full ticket price as revenue, and passes most of it to the operator—creating inflated revenue figures but negative gross margins.

The setup:

Jet.AI loves to talk about its “CharterGPT” app, Cirrus Aviation partnership, and “AI-enhanced booking platform.” Sounds sleek. But peel back the filings, and the economics are brutal. The company doesn’t make money on the flights—it makes money booking them, then calls the whole transaction “revenue.”

THE ACCOUNTING TRICK — GROSS VS. NET

Jet.AI books charter sales on a gross basis. That means if a customer pays $30,000 for a flight, Jet.AI recognizes all $30,000 as “revenue.”

In reality, $28,000 goes straight to the operator, fuel, handling, and third-party costs. Jet.AI keeps maybe $2,000.

A more conservative company would only book the net commission as revenue. Jet.AI instead inflates the top line with money that doesn’t belong to it.

THE CONSEQUENCE — REVENUE WITHOUT PROFIT

Q2 2025 filings: Jet.AI posted $2.2M in revenue but a gross loss of –$110K.

That’s not a typo. The company managed to lose money at the gross margin line.

Over the last twelve months ending Q2 2024, Jet.AI’s gross profit margin averaged –3%. For every dollar it booked, it effectively spent more than a dollar to deliver the flight.

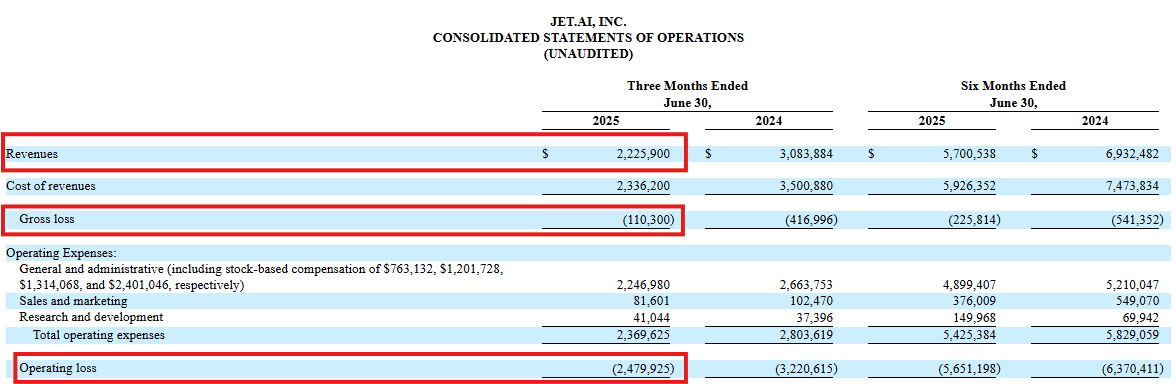

FIGURE: Q2 2025 CONSOLIDATED STATEMENTS OF OPERATIONS (Excerpt)

The company’s own 10-Q shows the problem in black and white:

Revenues: $2.23M

Cost of revenues: $2.34M

Gross loss: –$110K (losing money at the gross margin line)

Operating loss: –$2.48M

For the six months ending June 30, 2025, Jet.AI posted $5.7M revenue but still managed a gross loss of –$226K and an operating loss of –$5.65M.

Jet.AI’s Q2 2025 filing confirms the structural flaw: the company books full charter revenue, but costs exceed sales, producing a gross loss. Scaling revenue only scales losses.

DEFERRED REVENUE TELLS THE STORY

Year-end 2023: Deferred revenue (unflown prepaid jet cards/fractionals) sat around $1.78M.

By mid-2024: Down to $1.10M.

Translation: They were recognizing past sales as revenue but not replenishing with new sales. This is pull-forward accounting—eating tomorrow’s revenue to survive today.

Management admitted clients pulled back, “anticipating the sale” of the aviation business. In other words, customers stopped booking because Jet.AI told them it was getting out of aviation.

FIGURE: DEFERRED REVENUE DECLINE (2023 → 2024)

The company’s 10-Q shows Deferred Revenue falling from $1.78M at year-end 2023 to just $1.10M by June 30, 2024.

These balances represent prepaid jet cards and fractional ownership sales that haven’t yet been flown.

The decline means Jet.AI was recognizing prior sales as revenue but not replacing them with new bookings.

Management admitted clients held back purchases “anticipating the sale” of the aviation segment, further weakening future revenue streams.

Deferred revenue dropped 38% in six months—evidence of pull-forward accounting and collapsing demand as customers stopped booking once Jet.AI signaled its exit from aviation.

THE RED FLAG PATTERN

Big “revenue” numbers from gross reporting.

Negative gross margins that show the business model is upside-down.

Deferred revenue falling, proving demand is drying up.

Public spin about “AI software” to distract from the fact that the core unit economics don’t work.

“Revenue is what you brag about. Margin is what you eat. Jet.AI isn’t eating.”

OUR VIEW:

This isn’t growth—it’s a mirage of scale created by gross-up accounting. In reality, Jet.AI is a low-margin broker pretending to be a tech company. Investors are buying the optics of revenue, not the economics of profit.

THE LIFELINE LOOP: GEM, IONIC, SERIES B PREF, AND THE REVERSE SPLIT

When Jet.AI merged with Oxbridge Acquisition Corp. in August 2023, the victory lap was hollow. Investors expected fresh capital to fuel expansion. Instead, the SPAC trust had been stripped bare by redemptions, leaving Jet.AI with barely $530,000 to its name. From the opening bell, this was a company public in ticker only, not in balance sheet strength. Survival would hinge not on execution, but on serial lifelines.

The first stop was GEM Global Yield. Jet.AI trumpeted access to a $40M share purchase agreement. But the reality behind the headline was far less impressive:

Cash actually received: just $1.11M.

Price tag: an $800K commitment fee paid up front.

Result: The fee nearly equaled the capital drawn, leaving “Prepaid offering costs” as one of the biggest assets on the balance sheet.

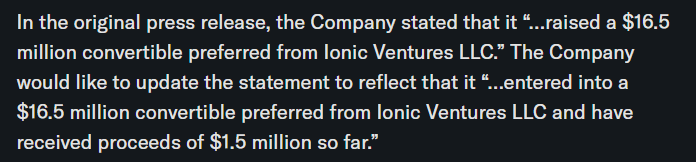

FIGURE : IONIC VENTURES FINANCING — CORRECTION NOTICE

In May 2024, Jet.AI was forced to correct its own press release.

Original claim: “Raised a $16.5 million convertible preferred from Ionic Ventures LLC.”

Correction: “Entered into a $16.5 million convertible preferred … and have received proceeds of $1.5 million so far.”

Caption:

Jet.AI initially implied a full $16.5M funding. The correction confirms only $1.5M was received, with the balance dependent on warrant exercises that never occurred—an admission that the original statement misled investors. READ HERE

From there, the baton passed to Ionic Ventures. In early 2024, Jet.AI blasted out a press release claiming it had closed a $16.5M financing. Investors thought salvation had arrived. In truth, only $1.5M ever hit the account. The rest was contingent on warrant exercises that never happened. The company eventually had to issue a correction—admitting its own announcement was misleading. The structure itself raised eyebrows: Series B convertible preferred stock capped at 9.99% beneficial ownership, a toxic setup that allowed financiers to drip-feed stock into the market without ever crossing disclosure thresholds.

As cash burn accelerated, the equity spigot opened wider. In 2024 alone, Jet.AI sold:

15.6M shares for just $1.5M (~$0.10 each).

26.6M shares for $2.4M.

Figure: Jet.AI’s share structure whiplashed within months—a drastic 1-for-225 reverse split in November 2024 temporarily shrunk the float, but by mid-2025, shares outstanding skyrocketed to 3.26M. That’s a 3,000%+ increase year-over-year—a brutal dilution cycle.

By year-end, the share count had exploded to 66M+. Nasdaq compliance was slipping, and Jet.AI pulled the standard trick: a 1-for-225 reverse split in November 2024. Overnight, the float shrank to ~300,000 shares. It looked cleaner—but nothing fundamental had changed.

Sure enough, the treadmill kept running. By mid-2025, shares outstanding had already crept back to 3.26M. And then came the latest blow: a new Form S-3 registering 1,956,000 shares for resale. The math is brutal:

Pre-issuance: 3,261,256 shares.

Post-issuance: 5,217,256 shares.

Impact: ~60% increase in share count.

Dilution: ~37.5% hit to existing holders.

The pattern is unmistakable. Big-dollar financing headlines, small-dollar reality. Fees that eat nearly as much as the cash raised. Shareholders shredded in the gears of issuance after issuance, reverse splits papering over the wreckage.

“When the story needs cash to survive, the stock becomes the product.”

Our view:

Jet.AI is not a business—it’s a dilution machine. Each “financing” is another turn of the screw, selling tomorrow’s equity cheaper than yesterday’s just to buy a little more time.

CONFLICTED CAPITAL: COMPANY CASH → INSIDERS’ SPAC SPONSOR

Jet.AI is starved for cash. Yet in August 2025, the company quietly revealed it had invested corporate funds into AIIA Sponsor Ltd., the sponsor of a brand-new SPAC called AI Infrastructure Acquisition Corp. On the surface, this looks like another step toward the “AI pivot.” But beneath it, the transaction reeks of conflicted incentives and insider enrichment.

Even more troubling, the timing coincides with Jet.AI’s own going concern warnings. In the Q2 2025 10-Q, management acknowledged that survival depends on external financing. Yet weeks later, they chose to fund a sponsor instead of plugging the company’s own liquidity gap.

Cash balance (June 30, 2025): ~$8.3M.

Quarterly burn: ~$2.5M.

Runway: Barely 3–4 quarters without new capital.

Insider focus: Seeding a SPAC sponsor instead of extending survival.

The conflicts don’t end at money. Murnane now wears two hats: still a Jet.AI board member, but also CFO and director of AI Infrastructure Acquisition Corp. Winston and other insiders hold parallel roles. That means the same executives responsible for salvaging Jet.AI’s crumbling balance sheet are simultaneously incentivized to make their SPAC deal succeed—even if it comes at Jet.AI’s expense.

“When every dollar counts, why is Jet.AI spending them on someone else’s promote?”

Our view:

This is governance malpractice. Jet.AI shareholders are watching their equity diluted, their cash burned, and their executives moonlight on a side project that enriches themselves. The SPAC sponsor investment isn’t strategic—it’s conflicted self-dealing dressed up as an “AI pivot.”

THE GREAT PIVOT: FROM JET CARDS TO “AI DATA CENTERS”

Jet.AI began life as Jet Token, a small player in fractional jet ownership and charter booking. It sold jet cards, marketed fractional HondaJet shares, and built a flashy app to connect customers with operators. The business was crowded, commoditized, and structurally low margin. Losses piled up. By 2025, management threw in the towel—announcing the sale of its aviation segment to FlyExclusive.

What came next was more startling: Jet.AI would abandon aviation altogether and “pivot” into AI data centers. The company that couldn’t turn a profit selling jet cards suddenly promised to build hyperscale GPU infrastructure to compete in the hottest arms race in tech.

WHAT THE PIVOT LOOKS LIKE

Spin-off: Jet.AI agreed to merge its aviation business into FlyExclusive through a Reverse Morris Trust. Shareholders will receive FlyExclusive shares, while Jet.AI keeps only software and IP.

AI repositioning: Jet.AI rebranded as a “pure-play AI data center company.” Management highlights partnerships and letters of intent with Consensus Core, a Canadian developer.

Project scope: Two proposed hyperscale campuses in Canada, with ambitions for 100+ MW GPU-powered data centers.

THE REALITY CHECK

Cash on hand (Q2 2025): ~$8.3M.

Quarterly burn: ~$2.5M.

Estimated cost to build one hyperscale data center: hundreds of millions of dollars.

Track record: Zero history building or running data centers. Prior experience? Selling jet cards.

Milestones disclosed: Talk of land negotiations, power purchase agreements, and early permitting steps—but no secured assets, no signed anchor customers, and no binding financing.

WHY THIS IS A RED FLAG

Buzzword arbitrage: Jet.AI is using the hottest theme in markets—AI infrastructure—to distract from deteriorating aviation metrics.

Mismatch in scale: The capital required dwarfs the company’s means. Even if partnerships contribute, Jet.AI is at risk of being diluted out or sidelined.

Execution risk: Competing against hyperscalers (Amazon, Google, Microsoft) and specialized players with real war chests is a losing battle.

Narrative vs. numbers: While press releases tout “AI progress,” the SEC filings still show negative margins, cash burn, and going-concern warnings.

“Jet.AI isn’t pivoting. It’s abandoning one failed business for another it can’t afford.”

OUR VIEW:

This pivot isn’t strategy—it’s survival theater. Jet.AI knows the aviation model is broken, so it slapped “AI data centers” on the masthead and promised investors a future it has no resources to deliver. Without secured financing, assets, or customers, the pivot reads less like transformation and more like narrative arbitrage.

FINANCIAL ODDITIES: NEGATIVE EQUITY, PREPAID OFFERING COSTS, AND WHIPSAW SHARES

Jet.AI’s financial statements read like a cautionary tale in corporate survival. Beyond the aggressive revenue reporting and endless dilution, the balance sheet itself tells a story of structural weakness and creative accounting.

NEGATIVE EQUITY — A COMPANY UPSIDE DOWN

By mid-2024, Jet.AI reported stockholders’ equity of –$3.94M. In plain English, the company owed more than it owned. Even after multiple capital raises, this deficit persisted—because new cash was consumed just as fast as it came in. Negative equity isn’t just a number; it’s a signal that liabilities, preferred claims, and accumulated losses have boxed out common shareholders.

PREPAID OFFERING COSTS — PAYING TO RAISE CASH

One of the strangest line items on the June 30, 2024 balance sheet: $800,000 in “Prepaid offering costs.” That’s not R&D. It’s not an asset that builds the business. It’s the commitment fee Jet.AI paid GEM just for the right to maybe raise money in the future. For a company with less than $2M in total assets at the time, that means nearly half its balance sheet was tied up in a fee for hypothetical financing. Few companies treat raising money itself as an “asset.” Jet.AI did—because it had nothing else to show.

WHIPSAW SHARE COUNTS — A MOVING TARGET

Tracking Jet.AI’s share count is like watching a shell game. In two years:

Pre-SPAC: A few million shares outstanding.

Late 2024 (pre-split): Over 66M shares after cheap equity sales.

November 2024: A 1-for-225 reverse split collapsed the float to ~0.3M shares.

Mid-2025: Shares outstanding crept back to 3.26M.

Post S-3 (if issued): ~5.22M shares.

That’s a swing of more than 20,000% in the denominator used for EPS in less than two years. In Q2 2024 alone, weighted average shares rose 170% YoY. For shareholders, that means every “per-share” metric is meaningless—the denominator is a moving target, constantly inflated away.

OTHER RED FLAGS

Redeemable preferred stock: $1.7M liability tied to early Series A preferreds with an 8% dividend, sitting senior to common.

Related-party notes: At 2023 year-end, Jet.AI still carried insider payables (~$266K), highlighting dependence on insider loans to survive.

Settlement in stock: The $2.4M Sunpeak Holdings settlement paid in equity, another dilution hit disguised as legal housekeeping.

“When prepaid fees are your biggest asset and equity swings by 20,000%, the financials stop looking like a business and start looking like a shell.”

OUR VIEW:

Jet.AI’s financial statements aren’t just weak—they’re structurally abnormal. Negative equity, prepaid offering costs, and whipsaw shares point to a company whose “assets” exist mostly to facilitate dilution. For common shareholders, this isn’t a balance sheet; it’s a liquidation funnel.

PEOPLE & PAST: LEADERSHIP BAGGAGE AND DIVIDED ATTENTION

If you want to know where a company is headed, start with the people driving it. Jet.AI’s leadership history is littered with red flags—from past legal scandals to present-day conflicts of interest.

GEORGE MURNANE — A HISTORY THAT STILL CASTS A SHADOW

Before Jet.AI, George Murnane was CFO of Mesa Air Group. His tenure ended in scandal. In 2007, a federal court sanctioned Mesa for destroying and withholding evidence in litigation with Hawaiian Airlines. The fallout was severe: the court found Mesa acted improperly, and within days the company “jettisoned” its CFO—George Murnane. The story was widely reported in financial media, including CFO.com, under headlines about Mesa’s evidence tampering.

That’s the same George Murnane now steering Jet.AI. While his biography highlights later stints at VistaJet and ImperialJet, it conveniently omits the fact that his last high-profile CFO role ended in termination under the cloud of misconduct. For investors, this isn’t ancient history—it’s a governance scar that speaks to credibility.

Mesa Air litigation: Hawaiian Airlines vs. Mesa Air, 2007.

Court finding: Evidence destroyed, discovery obstructed.

Outcome: Mesa sanctioned, Murnane terminated as CFO.

Connection today: Same executive, now CEO and director of Jet.AI.

DIVIDED ATTENTION — TWO JOBS, ONE CEO

Murnane’s governance issues don’t stop in the past. Today, he splits his time between Jet.AI and a brand-new SPAC—AI Infrastructure Acquisition Corp. He sits on Jet.AI’s board while simultaneously serving as CFO and director of the SPAC. Executive Chairman Mike Winston is also deeply involved in both.

This raises the obvious question: who exactly is running Jet.AI? The company is on life support, burning cash and facing going-concern warnings, yet its leadership team is devoting energy to a separate SPAC vehicle that personally enriches them through founder shares.

BOARD STRUCTURE — POWER CONCENTRATED, OVERSIGHT THIN

In August 2024, Jet.AI shuffled its C-suite: Winston became interim CEO, while Murnane shifted to interim CFO. That left Winston effectively in full control as both Chairman and CEO.

The board itself is small and insider-heavy—SPAC-era appointees, a sponsor rep, and a retired Israeli Air Force officer. Independent oversight is minimal.

Meanwhile, the company’s strategic focus has swung wildly—from fractional jets, to software, to AI data centers, to sponsoring a SPAC. Shareholders are left to wonder whether anyone on the board is pushing back.

THE RED FLAG PATTERN

Leadership with a track record of termination after evidence tampering.

Concentration of power in one executive (Winston) wearing multiple hats.

Conflicts of interest as executives moonlight on a SPAC sponsor while Jet.AI bleeds cash.

A board that looks more like a sponsor’s inner circle than an independent check.

“If leadership has two day jobs and one checkered past, shareholders are left holding the bag.”

OUR VIEW:

Governance risk is central to the Jet.AI story. A CEO terminated in his last major role for evidence tampering. Executives chasing personal upside in a sidecar SPAC. A board asleep at the wheel as dilution and pivots pile up. These aren’t just management quirks—they are fundamental risks to any investor betting on this team to deliver.

WHAT BREAKS THIS: SCENARIOS, CATALYSTS, PRICE PATH

Jet.AI’s story doesn’t unravel all at once—it bleeds out in steps. Each financing, each press release, each registration filing sets up the next crack in the narrative. For investors, the downside risk isn’t abstract; it’s sitting in plain view.

EQUITY OVERHANGS — SUPPLY SHOCKS WAITING TO HIT

The S-3 for 1,956,000 shares is the first shoe. Once those shares are registered, they’ll drip into the market, adding ~60% more supply and cutting existing ownership by ~37.5%. With Jet.AI trading on thin volume, even modest selling can crush the bid.

Catalyst: Effectiveness of the S-3, followed by selling pressure.

Impact: Immediate technical weakness as the market digests dilution.

THE FLYEXCLUSIVE DEAL — A CLOCK TICKING DOWN

The Reverse Morris Trust spin-off into FlyExclusive is pitched as transformational. But it’s already been delayed, extended to October 31, 2025. The deal hinges on Jet.AI delivering $12M net cash into SpinCo.

Cash as of June 30, 2025: ~$8.3M.

Burn per quarter: ~$2.5M.

Gap to requirement: At least $3–4M, likely more by closing.

If Jet.AI can’t meet that condition, the deal breaks—or worse, gets re-cut on worse terms. Either outcome is bearish.

Catalyst: Closing deadline for FlyExclusive deal.

Impact: Broken or renegotiated deal torpedoes the “orderly pivot” narrative.

AI DATA CENTER “MILESTONES” — PROMISES VERSUS PERMITS

Press releases promise big: 100+ MW data centers, GPU cloud, AI infrastructure. The filings tell a different story: no secured land, no signed power agreements, no customers. If milestones slip or counterparties walk, the AI narrative crumbles.

Catalyst: Missed or delayed project updates.

Impact: Market begins to price Jet.AI as hype, not hardware.

FINANCING STRAIN — THE NEXT DILUTIVE DEAL

Cash runway is measured in quarters. With $8.3M in the bank and $2.5M burning each quarter, Jet.AI needs fresh capital before mid-2026. History suggests the next raise will come in the form of toxic convertibles, more preferred stock, or another reverse split.

Catalyst: Next financing announcement.

Impact: Accelerated dilution; equity death spiral dynamic.

GOVERNANCE AND LITIGATION RISK

The history of evidence tampering at Mesa still hangs over George Murnane. Add in Winston’s dual role as Executive Chairman/Interim CEO and SPAC sponsor insider, and shareholder lawsuits or regulatory inquiries become more likely. Class-action law firms are already circling the FlyExclusive deal.

Catalyst: Shareholder lawsuits, SEC scrutiny, or proxy fights.

Impact: Governance credibility shredded further, investor confidence collapses.

PRICE PATH — HOW THIS UNRAVELS

Base case (dilution drift): Shares grind lower as S-3 stock hits the tape, FlyExclusive drags, and cash burn forces more raises.

Bear case (deal failure): FlyExclusive breaks, AI pivot loses steam, financing options tighten → accelerated death spiral.

Bull case (low probability): Jet.AI secures real financing and lands credible data center partners. Even then, shareholders face ongoing dilution.

“Jet.AI doesn’t need a short attack to collapse. The next catalyst is already in the filings.”

OUR VIEW:

The bear thesis doesn’t depend on finding fraud. It depends on arithmetic. Too much dilution, too little cash, too many promises. Every upcoming catalyst—S-3 resales, FlyExclusive conditions, AI project updates, next financing—skews risk to the downside.

DOCUMENT TRAIL & OPEN FILES: WHAT WE STILL WANT

Jet.AI’s filings, press releases, and deal announcements sketch the outline of a troubled company. But like any good investigation, the devil is in the details—and those details often live in footnotes, attachments, or contracts the company hopes no one reads. Here’s the paper trail we’ve traced, and the open files we’re still watching.

SEC FILINGS WE PULLED APART

10-Q (Q2 2025): Going concern warning, $8.3M cash, ~$2.5M quarterly burn, –$110K gross margin.

S-3 (Aug 2025): Registration of 1,956,000 shares for resale → ~60% increase in share count, ~37.5% dilution.

10-K (2024): Negative equity (–$3.94M), prepaid offering costs ($800K GEM fee), redeemable preferreds ($1.7M).

8-K (FlyExclusive merger): Reveals deal conditions, including Jet.AI’s requirement to contribute $12M net cash at closing.

Equity agreements: GEM share purchase agreement, Ionic Ventures convertible preferred financing. Both carry toxic terms.

PRESS RELEASES VS. REALITY

Ionic Ventures “$16.5M financing” (Jan 2024): Only $1.5M funded. Jet.AI issued a correction after misrepresenting the deal.

AI pivot announcements (2025): Claims of data center milestones, but filings admit projects are still at LOI/permitting stage.

SPAC sponsor investment (Aug 2025): Jet.AI put cash into insiders’ SPAC (AIIA Sponsor Ltd.), enriching management while starving its own runway.

RELATED-PARTY TRANSACTIONS

Bridge loan (2023): From Executive Chairman Mike Winston, later waived. Raises arm’s-length questions.

SPAC sponsor (2025): Jet.AI insiders (Winston, Murnane) double-dipping as both Jet.AI executives and SPAC managers.

Historical preferred stock (Series A): Early financings with opaque counterparties (e.g., Sunpeak Holdings settlement in equity).

OPEN FILES WE WANT TO SEE

FlyExclusive deal docs: Exact cash contribution terms, how net cash will be measured at closing, whether Jet.AI can actually deliver.

Consensus Core JV agreements: How much capital Jet.AI is obligated to provide for Canadian data center projects, and what happens if it can’t.

SPAC sponsor terms: Founder share allocations for Winston, Murnane, and Jet.AI itself—who really benefits.

Warrant conversion schedules: For Ionic Ventures and Hexstone Capital, showing how much more stock can hit the tape.

Board minutes: Deliberations around using scarce cash to fund the SPAC sponsor instead of core operations.

“The story lives in the filings. The next shoe is already in the footnotes.”

OUR VIEW:

Jet.AI’s filings reveal more than its press releases admit. But gaps remain. The FlyExclusive merger conditions, the SPAC sponsor terms, and the true obligations under Consensus Core could decide whether Jet.AI survives another year—or whether shareholders are simply diluted into oblivion. We’ll keep pulling the thread.

APPENDIX: DATA TABLES, ISSUANCE MATH, CHANGE-OF-SHARES MAP

SHARE COUNT EVOLUTION (2023–2025)

Jet.AI’s equity story is best told through its share count. The math doesn’t lie:

Date / Event | Shares Outstanding | Notes |

|---|---|---|

Aug 2023 (SPAC merger close) | ~3–4M | SPAC trust redemptions left just ~$0.53M cash. |

Late 2024 (pre-split) | 66M+ | Massive cheap equity sales: 15.6M shares for $1.5M; 26.6M shares for $2.4M. |

Nov 2024 (1-for-225 reverse split) | ~0.3M | Cosmetic reset to avoid Nasdaq delisting. |

Mid-2025 (10-Q) | 3.26M | Share creep from ongoing issuances, convertibles, and preferred conversions. |

Post-S-3 (filed Aug 2025) | 5.22M | 1,956,000 new shares registered for resale (~60% increase, ~37.5% dilution). |

DILUTION MATH FROM LATEST S-3

Pre-issuance shares: 3,261,256

New shares registered: 1,956,000

Post-issuance total: 5,217,256

Share count increase: ~60%

Dilution to existing holders: ~37.5%

BALANCE SHEET ODDITIES (2024–2025)

Equity: –$3.94M (negative stockholders’ equity, mid-2024).

Cash: $8.3M (Q2 2025).

Quarterly burn: ~$2.5M (Q2 2025).

Prepaid offering costs: $800K (commitment fee to GEM).

Redeemable preferred stock: $1.7M (Series A, 8% dividend).

“In two years, Jet.AI’s share count went from millions, to tens of millions, back to thousands, and up again—proof that common equity here is a moving target, not a store of value.”

OUR VIEW:

The appendix confirms the thesis in numbers: Jet.AI’s share structure is a dilution treadmill. No matter what the press releases say about AI, the filings tell the real story—every financing step crushes common equity further.

DISCLAIMER

This report is an independent, investigative opinion prepared by BMF Reports. Everything herein is based on publicly available information, SEC filings, press releases, news coverage, and sources believed to be reliable—but we make no guarantees of accuracy or completeness. Numbers can change. Filings can be amended. Management can (and often does) spin.

We are short $JTAI at the time of publication. That means we stand to profit if the stock declines. We may add, reduce, or exit our position at any time without notice. This report is not investment advice, not a recommendation, and not a solicitation to buy or sell securities. Do your own homework. Consult your own financial advisor.

If you’re reading this and you own the stock, understand what you own: a dilution treadmill with governance baggage. If you’re mad at us for pointing it out, that’s your problem, not ours.

BMF Reports exists to expose corporate bullshit. We call it like we see it. No apologies.